The Niveshaay team got lucky to get an opportunity to meet and interact with Mr. Vijay Kedia who is know for his spectacular success in investments like Atul Auto Ltd. (100x), Cera Sanitaryware (100x) and Aegis Logistics (40x) to name a few. It was a completely different experience to know about his journey from the person himself. He has written some incredible quotes and known for his prowess of striking the right note on the essence of stock markets through his singing compositions.

Few things that we learnt from him that we think are worth their weight in gold:

His Investing Mantra: ‘SMILE’

Small in Size Medium In experience Large in Aspirations Extra-large in market potential

A company which is smaller in size is always a better opportunity to look for because a smaller company like a fish has huge potential to penetrate or gain more market share and become the crocodile whereas, for a sizeable company to grow or penetrate further in a pond is comparably more difficult. He very famously quotes ‘fish in an ocean is far better than a crocodile in a pond’.

Medium in experience means he looks out for management that have an experience of 15-20 years and should have seen 2-3 down cycles with good times in their business graph. Such downcycles are great source of learning’s for the management to judiciously allocate the capital and earn prosperous returns. This gives them the ability to drive growth in the right direction.

Oh! We could completely relate to this mantra as our primary focus is on small-mid cap companies.

“Knowledge, courage and patience are key to successful investing. Courage will be tested in bear market”

Out of these three, Courage is the most important. Idea can be borrowed but not conviction. Without courage, it is not possible to have higher allocation in a stock and stick to a company without any fear if the price isn’t moving. Sometimes, it takes time for the market to give value to a company. He shared how he pitched his investment rationale of Atul Auto Ltd and Cera Sanitaryware Ltd. to institutions but no one believed it. Rome was not built in a day. Similarly, it takes time to build a strong portfolio. Build your own conviction, invest, keep patience and move on. Atul Auto Ltd. is a classic example on how on the basis of his strong conviction, he took 20% stake in the company. He even went to China with the promoters for business development.

His ability to think long term—how does he manage to hold an investment for 8-10 years ?

He explains when you use a torch, it gives a vision of upto 25 meters. You can’t see things which are 100 meters distant from you, right? Investing also works the similar way. On the first day, it’s difficult to predict the growth trajectory in next 8-10 years. Invest in a sunrise sector, observe progress at regular intervals and stay invested if it’s going according to your investment thesis.

The ‘Management Factor’ in investing

The company might have excellent product offerings, ultimately the management is responsible to thrive the company. The management of the company must have hunger to grow, shrewd business acumen, honest intentions, undying passion towards work and much more. Observe body language and tone of management- speaks volume about their characteristics.

“Alone you can go fast, together you can go far”. He applies this in his investing strategy aptly. He believes, a good team is a must to grow the business multi-fold rather than having a one man show.

Some money management and life lessons from him:

Avoid getting emotionally attached to any company, as he quotes “don’t marry your stocks.” Track them on regular basis and hold them till the thesis holds true.

“Only two people can buy at the bottom and sell at the top- One is God and the other is a liar.”

A company focused on its core business should be watched for rather than a company shifting its focus on different businesses.

He very aptly pointed out that he invested in a company that was originally into the business of tea plantations, forayed into sugar manufacturing but when they announced its plans for opening a dairy business as well, at that point, it was clearly evident to him that the company lacks focus and feared “ab chai ki dukan hi khol lenge”

Always have a fixed income, apart from the market gains for your day-to-day expenses, and invest that portion of your income that you will not need for at least the next 3 years.

Invest in such a way that you have a peaceful sleep at night. Mental capacity is of utmost importance in investing.

Whenever, we meet such experienced investors, we think how lucky our we to get their wisdom at such young age. Of course, your own experience is important but meeting and learning from them can help us to avoid some mistakes and become a more informed investor. Reading about a person and meeting in person is altogether a different experience. Happy to have this opportunity.

Ending with his two very good quotes:-

“Invest like a bull, sit like a bear and watch like an eagle”. (mantra for long term investing)

Whenever there is a correction in the market, the first question that comes to our mind is, “Is it a good time to stay invested or is it better to pull out of the market?”

We tend to make analogies from past market corrections and study the macro factors causing corrections. Isn’t it? Let us put things in perspective. The tightening of monetary policy by FED and now by RBI, inflationary environment due to the Russia-Ukraine conflict and COVID-19 led supply chain disruptions have created the current market environment volatile. We don’t know whether there would be more downfall or not, but what we at Niveshaay think is that, few factors have become quite favourable for the country to find a pivotal place in the global value chain. The current environment doesn’t augur well for businesses that require a consistent supply of capital to grow. Is it a good time to invest?

In the Indian context, corporates now have healthy balance sheets. It seems like, the focus of a lot of companies is to have a balance sheet characterised by low leverage. Labour demographics, cost of manufacturing is steadily becoming competitive and we’re a huge market. The most often used phrase after COVID-19 ‘China plus one’ looks structural and persistent providing tailwinds to the manufacturing sector. The export of engineered goods, steel, textiles and building materials to name a few have increased tremendously after the pandemic and from the pre-covid levels too. Acceptance of any product increases when one gets an opportunity to try and experience new products. India just got that and few companies totally grabbed these favourable opportunities to provide to international as well as domestic clients. With government focus on manufacturing and exports, reviving the capex cycle and taking measures to attract private capex are just some of the needed pre-requisites for growth.

Japan became the second largest economy globally in 1970-1980s, led by a strong central government, rapidly growing manufacturing sector and protective and supportive trade policies. In early 2000’s China was the net importer of metals and of many other products. Slowly, with supportive government policies and manufacturing cost advantages, China built out a massive network of factories dominating the global trade surpassing Japan to become the second largest economy. With COVID-19 led supply chain disruptions, emerging countries like India are getting opportunities in the export markets. India has twin benefits- we’re a huge market plus the ability to export competitively in few sectors.

Our approach in the current market mood is to focus on cash flow generating companies, reasonable valuations and healthy balance sheet.

Secondly, investment decisions shouldn’t be made in stocks that look cheap on the basis of hope that things will turnaround in 1-2 years. Hope is never a strategy and such companies generally are de-rated in markets which is brutal as we’re seeing in the current ones. We truly believe that current times are such where one should invest where there is a visibility and predictability of earnings.

Lastly, not to over-allocate to correlating sectors, follow the basket approach wherever required and keep a high margin of safety.

Themes, which we believe are expected to perform well include:

Capital Goods / Metal Ancillaries:Revival in capex cycle, Import Substitution at play –

Indian engineering components exports grew by 37% when compared to 2019 and grew to $ 111 billion in 2022, a rise of 50% from 2021 levels. The major thrust of government during the last two years has been to revive the capital expenditure cycle. The rise in capital expenditure helps to crowd in private investments. The virtuous cycle of investments begins in the economy. With higher steel and energy prices globally and supply chain disruptions, India can reap benefits from the government support through PLI schemes and import substitution policies additionally with export markets. Insights from visiting various exhibitions, interaction with varied entrepreneurs and management conference call discussions also highlight how imports of raw materials have reduced and domestic sourcing has increased wherever possible. Also, capital goods companies are showing healthy order-book at a time when government policy of export duty on steel translating to reduction in steel prices in home market would help these steel consuming companies in a significant way. Overall, till date, the earning season has been fantastic where few companies have shown good sales growth, maintained or improved margins. Some companies did show margin pressure too. The focus should be on companies that exhibit pricing power. This is also the time when global companies in the developed economies are incurring margin pressure. We truly believe that Indian manufacturing will be the best quality asset to own across the globe as an asset class.

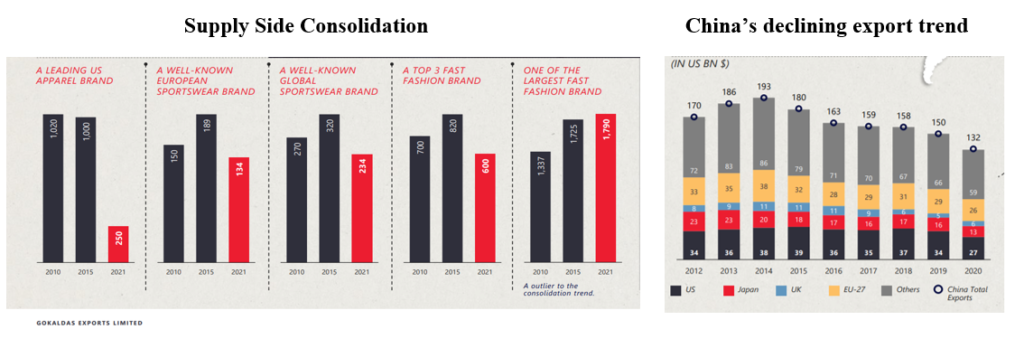

Textiles:Government focus, supply side consolidation and China+1 at play –

Currently, play on apparel segment in the textile value chain looks good. India’s annual textile exports can rise to $100 bn in the next five years from the current USD 40 bn as per Ministry of Textiles. Garmenting requires low investments when compared to setting up spinning, fabrics and processing units.

Renewable Energy: Good for the Planet and a Great Business to Invest in –

This sector has been our focus area since a long time now. Transition to clean energy is certainly the buzzword in the global economy. Why has it suddenly become so important than ever?

Well, COVID-19 accelerated the clean energy adoption trend and also made us realise that the shift to green energy is fuelled by necessity. In addition, the Russia – Ukraine war also highlighted a quick shift to renewables is important. The use of renewables in place of coal will save India Rs. 54,000 cr. ($8.43 bn.) annually by 2040. Renewable energy will account for 55% of the total installed power capacity by 2030. Countries like India and Europe, which are fuel dependent on other nations, did realise the need to fill in the gaps after the energy supply disruptions for greater security after the pandemic and the war period. Hence, definitely, it’s a long-term and integral play for any economy to achieve sustainable growth.

Building Material Industry:Product gaining market share and the industry is expected to grow at a CAGR of 15-20% in next 3-4 years –

Here, the play is on MDF industry where the product is a substitute for plywood and doesn’t have any threat from imports. Being, 80% cheaper compared to plywood, the industry is gaining huge traction due to the increase in housing demand, growth of online home décor platforms and reduction in furniture cycle time.

Staying invested amidst these short-term hiccups will make a huge difference in the long term. Meanwhile, we’ll continue to stick to our process and give our one hundred percent always.

Geography Wise Sales- US (61%), Europe (13%), Asia (24%) & Others (2%)

2. Q4 FY22 Results and Conference Call Highlights:

A. Why margins improved in the current quarter?

Operating efficiencies improved

Able to pass on the prices

Fabrics prices haven’t increased in tandem to cotton prices

Also, partly Q3 and Q4 are good quarters as there is increased sale of outerwear (High Realization Products). Essentially, cost remains the same and EBITDA Margins improves.

Going forward,

The company has been able to pass on the increase in raw material prices in last few quarters. 90% of the time, the company has been able to pass on the margins, guided by the management.

Employee Cost increase linked to inflation is expected to happen from Q1 FY23. This happens every year in April (Throughout the year, it remains static). The increase would be around 4-5%. The management plans to offset this increase by high productivity yield which the company has been able to do in last few years.

Automation/ Upgradation of machineries are few measures helping them

B. Demand Scenario

Full Capacity Utilization order book visibility for H1 2023

Can do a better run rate than the current Rs.500 crores as guided by the management.

Production issues in Sri Lanka and Pakistan not helping them much in more order enquires as they aren’t directly competing with these countries in the product mix.

The global economy is quite volatile, need to closely watch the US / UK/ Europe inflationary environment. But, till now, the company isn’t facing any such issue.

Also, apparel players have been able to pass on the increased price to final customers.

C. PLI scheme approval

The company received an approval in the government PLI Scheme. The Madhya Pradesh expansion is under PLI Scheme. The incentive would start reaping in from FY25. The company plans to invest Rs. 149 crores under the PLI Scheme.

D. Product Mix on RM Basis

Cotton- 60%

Linen, Viscose- 10-12%

MMF- 28-30%

E. Capacity Expansion Plans:

Capex in Bangladesh: The company is deciding whether to lease or build its own capacity. Mostly, they plan to opt for leasing method.

F. Other Insights: The company has generated 15% revenue from new customers. 40-45% of the client base has long term relationship.

3. Financials

4. Conclusion

Overall, the management sounded positive in the conference call. Overall, production cost in China is going up and also labor demographics there is aging and cost is increasing in Vietnam too. There might be issues like hike in raw materials and demand issues in the US due to inflation in short term but we think the apparel segment in India can do really well in long term. With government focus on exports of apparels/textiles, small base of apparel exports, India, being cost competitive in the cotton value chain globally and low investments require to expand in apparel segment can aid well for apparel exports in India in next 3-5 years.

The COVID accelerated China plus one and supply-side consolidation trend, the company has been able to gain market share and increase exports. This company is expected to do well as it is quite agile in handling product varieties, timely delivery (important metric) and maintaining margins and at the same time, we need to closely watch the geo-political issues and inflationary environment in the US.

We continue to maintain positive outlook on the company.

To view our initial coverage on Gokaldas Exports Ltd.

Positive – Expected Return of 12%+ on annualized basis in the long term Neutral – Expected return in the range of +/- 12%

Negative – Expected return in negative

Disclaimer:

Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained here is accurate, reliable and has been obtained from public sources which we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Research Analyst: Ramswaroop Agarwal (rsa0308@gmail.com) & Kartik Mediratta (Kartikmediratta64@gmail.com)

When promoters buy-back, it is a positive sign. But, when the competitor companies’ promoters take stake in the peer company that significantly boosts investor confidence as they are the most clued people to know about the industry prospects. This keenly watched attribute adds to the assurance factor for the investor. This scenario is being seen in the emerging MDF industry. The leading MDF players like Century Plyboards and Action Tessa have bought stake in Rushil Décor.

The strong conviction of industry leaders towards the growth of the MDF industry and their confidence in Rushil Décor is one of the many reasons why we think that this company can perform well in future. The report aims to discuss the industry and business model in great detail.

SHAREHOLDING OF PROMOTERS OF PEER GROUP (as on 30/09/2021)

Note:

Promoters of Century Plyboards have acquired 1.37% stake in RDL in Q1 FY22 and subsequently acquired additional 4.02% stake in Q2 FY22.

Promoters of Action Tessa have increased their shareholding in RDL by 1.71% and 0.15% in Q1 FY22 and Q2 FY22 respectively.

This trend seems to be continuing in the subsequent quarters as well.

Trend of Change in Shareholding

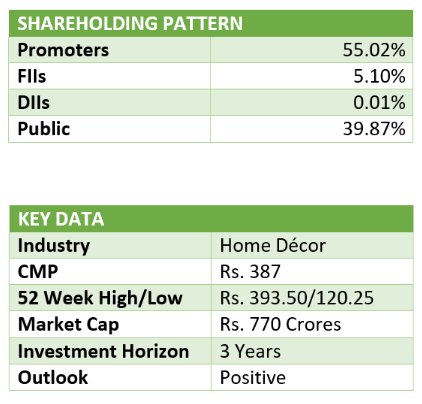

ABOUT COMPANY

Rushil Decor Ltd is the flagship company of the Rushil Group. Rushil Decor Ltd was incorporated on May 24 1993 as a private limited company with the name Rushil Decor Pvt Ltd. The Rushil product portfolio includes Laminates, Medium Density Fiber Boards (MDF), High-Density Fiber Boards Water Resistant (HDFWR), Pre- laminated Decorative MDF Boards and PVC Boards.

Rushil Décor Ltd. is one of the leading company in Laminate and MDF panel boards industry in India with a global foot print in and around 42 countries.

It has 6 manufacturing facilities across West and South India focusing on different product segments. The units are strategically located which assist in the smooth procurement of raw materials which is proved to be the significant factor in cost effectiveness.

INVESTMENT RATIONALE

1. Rapid Pace of Urbanization: As a nation of 1.39 Billion people, India has demonstrated quicker recovery trends in demand as far as consumption of staple commodities, high-end necessities such as electronics, home furnishing as well as luxurious goods such as automobiles are concerned. Especially, the demand for home décor and electronics has been steadily climbing up, as people have been forced to remain within the confines of their homes due to the lockdowns and their swift adoption of the work-from-home trend. Rapid urbanization has also contributed to exponential growth in the real estate sector. It is estimated that there is a shortage of around 10 Million housing units in urban India. According to industry research, supply of additional 25 Million units by 2030 is required to meet the growing urban demand. This growth potential is expected to percolate to allied industries such as consumer goods and home décor industries.

2. Robust Demand and Entry Barriers: The MDF and PVC segments are fast growing owing to their inherent strengths and advantages. There is a huge opportunity in terms of market growth as well as import substitution. The MDF segment has high entry barriers especially in terms of required capex. Hence, there are a few unorganized players in the MDF segment and the industry is more than 90 percent organized.

3. Housing For All’ and Development of Smart Cities: Such programs will drive construction of large number of houses across India, leading to additional demand for furniture. It is estimated that India will receive investment of approx. $1.3 Trillion in housing sector over the period of next 7 years. Notably, the investment would lead to construction of new 60 Million houses.

4. Atmanirbhar Bharat: The Indian government’s commitment to encourage selfreliance is intended to develop Indian industry and reduce imports. In turn, we believe that this platform could deepen India’s industrialisation, strengthen incomes and widen the consumption play.

5. Urban Real Estate Growth: The Indian real estate growth has underperformed its retrospective average in recent years. However, the Work From Home phenomenon has increased the priority of buying into bigger and better homes, kickstarting sectorial growth from the second quarter of the last financial year, which is expected to increase the offtake of interior infrastructure products.

6. New Plant: Company has set up a new MDF manufacturing facility at Andhra Pradesh with capacity of 800 CBM per day. For this, company incurred a capex of approximately Rs. 450 crores. This will help Company to cater large set of customers which in turn will strengthen the market share of Company. The new plant is equipped with latest German technology which will consume 8-10% less raw materials thereby reducing the total cost of inputs and will lead to higher margins. According to industry experts, the Replacement Cost of Rushil Decor’s Andhra Pradesh plant is approximately Rs. 650 Crores.

7. IKEAZIZATION of Furniture Industry: IKEA is an internationally known furniture and home furnishings retailer. IKEA entered India in 2018 and is expanding since thereon. IKEA is sourcing 20% of its products which are made in India and the same is expected to reach 30% within 2-3 years. The furniture which they procure is made up of only MDF and particle boards, majorly MDF and the use of plywood is negligible. Due to more demand in MDF sector this would definitely unleash the inherent potential lying in the industry.

For a detailed understanding on Indian Furniture Industry & Indian MDF Industry, visit our blog:

Due to sustained momentum in demand as well as prices, manufacturers are getting a clear revenue visibility, despite some price war in the market space. The capacity utilization in the industry has also gone up by 15% to 20% (i.e. 70-75% in 2021, which is expected to improve to 80-85% by 2025).

Industry experts believe that demand for MDF will match the increase in production capacity within the next couple of years. MDF’s market share will further bolster with the rising prices of Poplar Timber, a chief source of economy grade plywood in North India. It is expected to gain market share of Low & Medium grade plywood (which constitute 85% of the Plywood market in India).

MDF Segment of Rushil Décor Ltd.

Rushil décor is India’s third largest manufacturer of MDF. It has state-of-the-art manufacturing facility, one at Karnataka with total capacity of 300 CBM per day and another one at Andhra Pradesh with total capacity of 800 CBM per day. Thereby taking the total capacity to 1,100 CBM per day or 3,30,000 CBM annually. It incurred capex of Rs.450 crores for setting MDF manufacturing unit at Andhra Pradesh. The regular commercial operations were started from March’21. This plant will help Company increase market share and take care of incremental demand generated in Industry. The new plant is equipped with latest German technology which will consume 8-10% less raw materials and will play a key role in reducing total input costs therefore strengthening overall margins. Also, the company has vast network of 100+ distributors, 50+OEMs and 1000+ dealers.

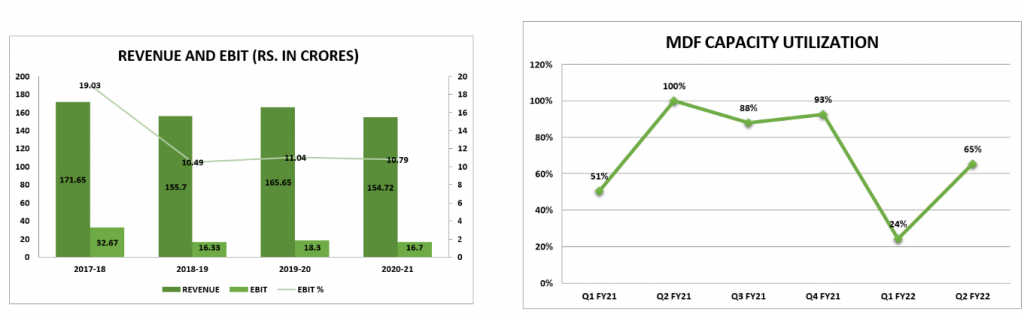

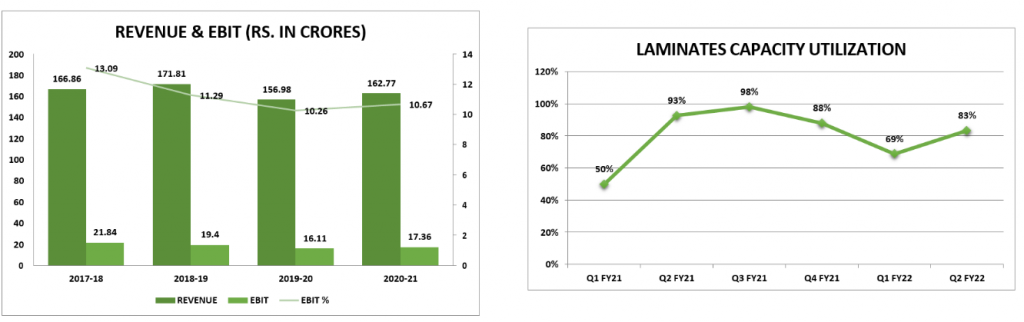

Note:Capacity Utilization has declined in Q1 FY22 as the new plant at Andhra Pradesh has commenced operations in March 2021 and is yet to achieve optimum capacity utilization. Management has guided an overall capacity utilization of 65% for FY22.

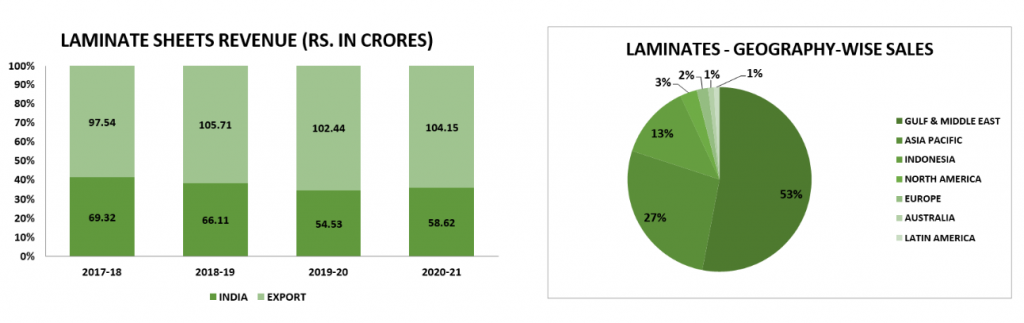

LAMINATES

Laminate sheets are made by bonding together two or more layers of materials. Laminate sheets from plastics are glued to wood to make the surface aesthetic. These sheets are manufactured by laminating different types of papers with formaldehyde. The core sheet consists of Kraft paper with phenol formaldehyde (PF) and below it, a barrier paper is provided. Above the Kraft paper, a tissue paper is impregnated with FF melamine formaldehyde (MF) resin is provided which gives protection and also enhances abrasion resistance. Then, these laminates are bonded to wooden surfaces with suitable glue and pressing for some time finishes the process.

Laminates provide a better surface finish for furniture elements and also provide an attractive look for a very less price. Furniture like tabletops, cupboards, surfaces of chairs mostly uses laminates as the finish material.

Types of Laminate Sheets:

High-Pressure Laminate (HPL): The layer of the laminate adheres to substrate under pressures of 70 to 100 bars at temperatures of 280° to 320° Fahrenheit using adhesives. The laminates are available in thickness 0.8 mm, 1.0 mm and 1.5 mm in standard sizes 1.2 m x 2.5 m. These laminates are most durable, flame retardant, and consists high level of resistance to heat and chemicals.

Low-Pressure Laminate (LPL): The layer of the laminate adheres to substrate under pressures of 20 to 30 bars at temperatures of 335° to 375° Fahrenheit without using adhesives. These laminates are less durable, thinner than HPL, flame retardant, resistant to heat and chemicals and comparatively very cheaper than HPL.

Applications of Laminate Sheets

Laminates Industry

The global market size for decorative laminates is estimated to be worth USD 91,015.03 Million by 2025, registering a CAGR of 5.3%. On the global demand map for decorative laminates, China and India are leading from the front as their huge demand emanates from their enormous population base, growing urbanization and mass- scale construction activities in residential as well as commercial real estate sector. Consumption of Indian panel products has grown at CAGR of 15-20% for organized sector.

Indian Laminate market size is Rs. 5000 Crores. Major chunk of market is enjoyed by the unorganized sector due to low-capital intensive industry. Apart from voracious consumer demand, implementation of tax reforms such as GST is expected to aid the organized manufacturers capture a larger market share as against their unorganized counterparts.

Production Capacities of Top Organized Players:

Laminates Segment of Rushil Décor Limited

Note:Capacity Utilization is lower in Q1 FY21 and Q1 FY22 due to 1st and 2nd wave of Covid19 pandemic in Q1 FY21 & Q2 FY22 respectively.

POLYVINYL CHLORIDE (PVC)

Poly Vinyl Chloride (PVC) is a high-strength synthetic resin made from the polymerization of vinylchloride. It’s a sheet made of plastic composite that’s extremely durable in its purest form. The first thing that comes to mind when PVC is mentioned is pipes and plumbing material. However, PVC is also an extremely versatile material, one that is used for flooring, cabinets, countertops and more.

It is in very high demand in building and construction industry because of its multifaceted use in windows, doors, sidings, roofs, wires, cables, pipes and fittings. Such a wide variety of applications emerges from PVC’s safety, quality, durability and cost effectiveness as a material. PVC is light weight, tough, easy to mould, strong material that resists corrosion,rotting or adverse impacts of weather effectively. For the similar reasons, the PVC boards are also high in demand as they give highly aesthetic look after finishing and are economically priced.

Uses of PVC Foam Sheets/PVC Foam Boards

Used for the ceilings of Cars, Buses or Trains

Widely used for making home and office furniture

Used to build external wall panels

Home interiors can be designed using PVC foam boards

Used in sign boards and outdoor advertising kiosks

Used in Construction, Garage Doors, POP Displays, Exhibit Spaces & Signage

Advantages of PVC Foam Boards

Water Resistance: PVC foam boards have solid resistance to water due to its composition. When it comes in contact with water, it does not swell or lose its composition. This makes is fit for all types of weather.

Corrosion Resistance: When brought in contact with chemicals, PVC doesn’t react. This keeps its state intact and saves it from any kind of deformation.

Fire Resistance: PVC foam boards can be used anywhere as they are fire resistant. There is no effect of acid, heat or light on it.

High Strength & Durability: Due to the structure of its component molecules, PVC foam boards are highly strong which ensures that they don’t undergo any deformation. The boards can survive for as long as 4 decades without any damage.

Easily shaped and painted: PVC can be given any shape to suit your requirements. It can be cut for the furniture of your house or can be made into wall panels for exterior use. Also, it can be painted with any type of paint which lasts for years and gives the look and feel as if it is new!

Pocket-friendly: They are a good substitute for wood or aluminium and they come in a variety of price range. They don’t require any extra maintenance and stay in the same state for quite a long time. No special equipment is required to cut or drill them and this makes them pocket-friendly to use.

PVC Market in India

Though in fledging stage, the market for PVC boards in India is gradually expanding with the size of the market touching nearly Rs. 2000 Crores, before the pandemic of COVID-19 hit..

COMPANY FINANCIALS

Notes:

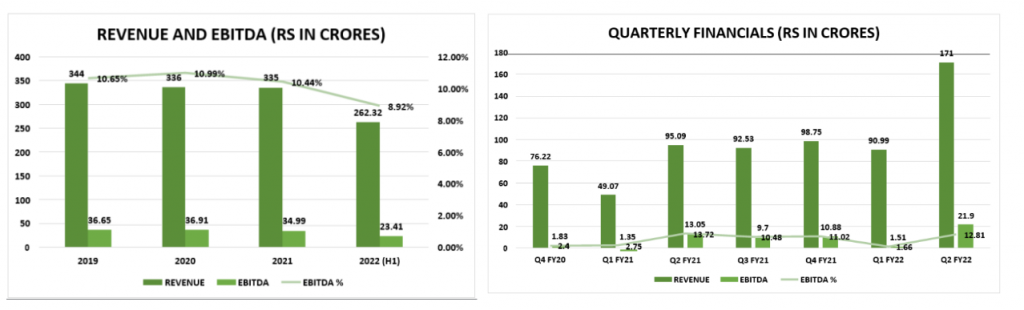

EBITDA margins have declined in Q1 FY22 and H1 FY22 as the company has commenced commercial operations at its new MDF manufacturing plant at Andhra Pradesh leading to higher costs. These costs are expected to taper down gradually with improved capacity utilization.

Finance Costs and Depreciation have increased from Q1 FY22 onwards due to commencement of operations at the new plant at Andhra Pradesh and cessation of capitalization of Interest expenses of the new plant which are now being charged to Statement of Profit & Loss.

Financial Ratios:

Debt Repayment Obligation:

RUSHIL DECOR V/S NIFTY SMALLCAP 250:

VALUATION

Notes:

Total EV of Rushil Décor is Rs. 1,160 Crores. However, approximately 25% of this value is contributed by its Laminates Segment. Hence, EV for MDF segment = Rs. 870 Crores.

Since, Greenpanel is the market leader in MDF industry with strong brand value and extensive dealer networks, it deserves a higher valuation than Rushil Décor. So, our target EV per ‘000 CBM is at 50% discount to Greenpanel.

* This should be the Fair Value based on current capacity of the company’s MDF segment. These values are subject to periodic revision based on improvement in capacity utilization of the new plant and the company’s ability to set up efficient dealer networks for its products thereby driving growth in revenue and EBITDA margins.

SCENARIO ANALYSIS

Notes:

The above tables show the effect of improved capacity utilization across the 3 segments of the company on its revenue and EBITDA margins over next 2-3 Years.

Under the Moderate Scenario, the MDF segment is expected to operate at 75% capacity. In this case, the topline is expected to double and the EBITDA margin will increase to approx. 15% due to improved operational efficiencies.

Under the aggressive scenario, the MDF segment is expected to operate at 85% Capacity. In this case, the topline is expected to multiply 2.5X and EBITDA margin will improve to approx. 20%.

RISKS AND THREATS

High Competition

The industry in which the Company operates has intense competition, especially from the unorganized sector in the plywood and wood panel segment as around 75% of the market players are still unorganized.

Companies like Greenpanel and Action Tessa are the market leaders in MDF. They enjoy strong brand value and vast dealer networks. Significant difficulties could be faced by Rushil Décor to penetrate in the markets of these companies and expand its dealer network.

New Entrants: For the laminate segment, entry barrier in terms of required capex is pretty low. There always remains a pressure of new entrants getting in the organized market, which has been the case, leading to higher competition.

Raw Materials: With increasing urbanization, deforestation is taking a toll on the raw material availability. Further, erratic monsoon has played a role in suppressing the raw material supply. Rising crude price has been another reason leading to an increase in raw material prices.

Man power crunch: Manpower availability in case of Laminates has been one of the most- impacted matrix of operation for this industry and for the Company more so in the wake of the pandemic. Most migrant labourers left for their respective home locations and many of them are yet to return leading to labourer supply shortage. Moreover, skilled manpower is scarce and availability is an issue.

Overcapacity in MDF Industry: MDF being the lustrous business segment, bestowing the higher margins, has always provided the exposure to new entrants. With the entrance of new comers the MDF market is exploited with over-supply and thus the realization per unit crashes thereby leading to trembling of margins.

Import Menace:

Imports has always been a cause of trouble for domestic sellers as the importers provide par quality product, as to what domestic merchants are providing, but at considerably low costs. Prior to the pandemic, India imported 30% of its MDF demand. Post- Covid imports of MDF and Laminates fell sharply to 15% due to the surge in logistics costs particularly the container cost. This momentary surge in prices is expected to taper down in the upcoming period and imports may resurge to the pre-covid levels.

Companies like Greenpanel and Actiontessa mainly operate in North India which provides them a strong location advantage in terms of protection from imports due to higher logistics costs to transport imported MDF from ports to North India. Thus, these companies continue to be a major threat for Rushil Décor to penetrate in different regional markets in India.

Outlook Interpretation

Positive – Expected Return of 12%+ on annualized basis in the long term

Neutral – Expected return in the range of +/- 12%

Negative – Expected return in negative

Disclaimer:

Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Prima Facie, equity as an asset class in last 2 years has given splendid returns to investors given the low base formed in March 2020. Our strategy has turned out to be fruitful in out-performing the market. With immense gratitude, we are happy to say that our portfolio has been amongst the top performers on smallcase.

From here on, should we keep our expectations moderate and realistic? Will the markets fall? These are the most frequently asked questions to any investor. Let’s put things in context.

Amid the market mayhem, sticking to your investment process, research, discipline, patience and not to miss the luck factor did result in superior returns for investors. Let’s keep this in mind and move forward.

FY21 was an eventful year. FY22 continued the streak, began with a fatal second COVID-19 wave and ended with Russia-Ukraine conflict with energy crisis in Europe, Sri-Lanka economic crisis and supply chain disruptions in between resulting in high commodity prices creating inflationary environment. What remained common is that Indian economy emerged resilient and stronger getting benefited due to supply chain disruptions, China +1 and most importantly prudent government support policies in few sectors. Not to miss, the record IPOs that came in FY22. Where are we currently? FY23 also, began on a high note. At Niveshaay, analysing the current scenario characterised by too many moving parts, we are following a stock specific approach where we see structural trend.

How are we picking up stocks?

The best characteristics of equity markets is that we can switch to sectors which are doing well amid the chaos taking benefit of China +1 strategy, inflationary environment etc. For instance, commodity producers (metals, mining, oil and gas etc.) are having a good time while the commodity consumers (Auto, FMCG and consumer durables etc) are having difficulties in passing on the increased prices. Of course, some sectors are unaffected too rather witnessing tailwinds like the IT and Pharma.

We started tracking manufacturing sector in 2016, and little did we know that five years later, the sector would witness upswings from structural and persistent trends like China plus one, consolidation in supplier base and strong government focus. Connecting the dots, looks like India is getting benefitted from these trends owing to certain competitive advantages like cheap labour, low interest rate, favourable government policies, ease of doing business and India is a huge market in itself.

Having said that, the Budget 2022-23 continued the growth momentum through a higher multiplier effect. The major thrust was on reviving the capital expenditure cycle in the country through PLI-Scheme, China plus one and imposing anti-dumping duty boosting domestic production. The rise in capital expenditure helps to crowd in private investment. The virtuous cycle of investments begins in the economy. Capex has a higher multiplier effect on economic output over revenue spending. Investment cycle has bottomed out. Investment contribution to GDP has reduced to 26.7% in FY21 from peak of 36% in FY07. The value of new projects in quarter ended March, 2022 was Rs. 5.1 lakh crores, 53.6 % higher qoq and double when compared to the previous year quarter (Source: CMIE).

Staying true to our investment style, we’ll continue to focus on companies where competition is limited, plays a pivotal role in the manufacturing process and an indirect play on the expected high growth in a broad sector. Here, we are broadly focusing on building materials, textiles, chemicals, metals etc.

Another theme, which we continue to remain bullish on is the renewable energy space. This sector is benefitting from the government impetuous and now the entry of private sector (Reliance Industries) signals a green time in this sector has come. Also, Indian players are becoming competitive globally. When the world is moving towards sustainability, companies doing their bit in achieving the same, then why not tap these opportunities and be a part of their growth story when they are literally getting premium for their products?

Also, focus is on Exports. The pandemic has certainly built a framework for India to find a pivotal place in the global value chain in some sectors like chemicals and textiles. According to commerce and industry ministry, the exports of $418 bn in FY22 surpassed the government target by 5%.

India is a growing country where penetration of many products is very low. So, looking at consumption sector becomes important and also insulating cyclical nature of our portfolio at the same time.

Overall, we look forward to play on such themes, keep evolving with time and continue to analyse trends with fresh perspective.

A BIG THANK YOU to all our subscribers for trusting us in your wealth creation journey. We will continue to stick to our process and give our one hundred percent always.

Part III:How is it different from global industry?

Indian Paper Companies: Classification based on Raw Materials Used

Financials

Research Analyst – Gunjan Kabra (info@gunjankabra.com)

The Paper Industry is classified into four segments:

Printing and Writing (30%)

Coated

Uncoated: Creamwove, Maplitho, Copier

Packaging and Paper Board

Duplex Boards (used in small –packaging: FMCG)

Kraft Paper (used in packaging for transportation)

Specialty Papers (9%)

Tissue Paper

Newsprint (15%)

Characteristics of the Indian Paper Industry

Capital, Energy and Water Intensive

The paper factories in South India are facing issues in sourcing water, so one should be careful while choosing a company as the requirement of water is huge.

Fragmented

Small units account for ~60% of the Industry Size.

Paper can be produced by any of the following Raw Materials:

Wood Pulp (30-35% paper is made from wood pulp): Hardwood and Softwood

Waste Paper (45-50% paper is made from Waste Paper)

Agri Residue (20-22% paper is made from Agri Residue)

Raw Materials used in producing paper will help you in identifying which company to invest in based on the industry dynamics.

High demand and scant supply in Europe driving increase in paper prices

Restricted supply and high energy cost put upward pressure on prices

Against the background of an unprecedented rise in energy prices and other costs, paper producers have almost doubled prices for their products (fine paper grades) compared to January last year. Paper manufacturers explain that in some of their mill’s production costs have risen by several hundred euro per tonne of paper.

Strike at UPM, Finland leading to supply issues

UPM supplies Europe with about 40 percent of the backing sheets for labels.

Russia-Ukraine War Impact

How much paper and board does the EU export to and import from Russia and Ukraine?

Pulp and paper trade between the EU and Ukraine goes mainly one way: about 440,000 t of paper and board are imported by Ukraine from the EU. Ukraine’s exports are very limited.

When it comes to Russia, around 900,000 t of paper and board are imported by Russia from the EU, while Russia exports close to 700,000 t to the EU (accounting for 50% of the Russian exports). Regarding pulp, EU-Russia trade is quite balanced with around 400,000 tonnes traded in total.

2. Rise in prices of Waste Paper/Kraft Paper, availability being an issue

From February 1, the US waste paper rates have been increased to $400 from $300 a tonne.

Ban on exports of waste paper from Europe to India likely to get resolved.

The corrugated box manufacturer, recycled paper manufacturers are having a hard time in sourcing raw materials and maintaining margins. Viability is becoming an issue for small players.

Waste Paper isn’t a high value item to afford such huge freight costs whereas pulp is a high value product. Hence, the high freight costs are still manageable comparatively.

3. Also, when the global wood prices are higher, Indian paper manufacturing companies tend to become competitive and are expected to perform well.

Under normal circumstances, Indian paper companies become globally competitive when the prices are beyond $650-700/tonne. The reason is discussed in detail in the later part of the report.

4. Paper Demand is back to normal with higher demand on the packaging side

Office paper demand is back to normalized levels. Also, with the opening of schools, the demand for paper is expected to resume to normalized levels.

Currently, the industry dynamics guide that wood-pulp-based paper manufacturers are expected to do well. Also, keep in mind that a vertically-integrated business model is a huge added advantage and should be given a preference.

Increased E-commerce penetration, anti-plastic sentiment, a recycled feature of the paper is leading to increased demand for paper.

5. Cost Pressure

The cost of production is increasing on all fronts, from raw material, chemicals to power and logistics.

Also, consider that the paper industry is a cyclical industry. We prefer sticking to a market leader who has been able to maintain its growth, margins and has already done capex.

6. Recent Price Trend

The buoyancy in the prices continues due to issues in raw material availability, rise in chemical prices, logistics prices. Mondi, a leading packaging company in Europe highlighted in its conference call on 3rd March 2022 that the prices are 20-25% higher than the average of 2021. The high-cost base remains amid favorable demand and tight supply scenarios.

With hike in prices by recycled paper manufacturers, Wood Pulp based manufacturers also took a hike even when their raw material prices remained stable.

Vertically-Integrated Business Model is a huge added advantage and should be given a preference. When wood pulp prices are higher globally, Indian companies tend to become competitive.

Hardwood: Domestic secured supply

Softwood: India is import dependent

About the Company

Leading player in Office papers, Coated papers and Packaging boards

It has a ~24% market share in the branded copier segment, 12% in coated paper segment and 13% in packaging board segment in India.

Robust distribution network of over 300 trade partners and 4000 dealers with 15 pan-India depots

15% revenue is derived from export markets

Export Destinations:

Industry Dynamics suggest wood-pulp based companies are expected to perform well.

It’s a leading wood-pulp based paper manufacturer. As explained above, this is expected to perform well.

2. Capacity Expansion:

Packaging Board Plant Commenced in Jan 2022

The company did an expansion by 170,000 TPA in the packaging board segment at Songadh, Gujarat to take advantage of this growing segment in the paper industry. The company also set up a pulp mill to cater to the new expansion.

The packaging board was commissioned in Jan 2022. The plant is operating at 80% C.U. and is expected to reach 90% in the next 2-3 months. At peak capacity, it is expected around Rs. 1200-1600 crores of revenue ending on the price realization. 10-15% of the revenue from this plant is expected to be derived from exports.

Plans to set up a corrugated packaging paper in Ludhiana

Capex- Rs. 150 crores

Peak Revenue: Rs. 150-170 crores

Commencement: Q2 FY23

Revenue Target Guidance: ~Rs. 3500 crores in FY22

Acquisition of Sirpur Paper Mills

In Aug-2018, JK Paper had announced the acquisition of sick company Sirpur Paper Mills. It has an integrated paper and pulp mill with a capacity of 1,38,000 tonnes per annum. Currently, it is operating at 80% capacity utilization and is expected to reach 90% in Q1 FY23.

3. The company has been able to maintain sales growth and range-bound EBITDA margins

4. Rise in demand for packaging:

Growth in E-Commerce

This segment can lead to a huge demand for paper boards. With fall in the price of waste paper and rise in the finished paper can lead to an increase in turnover and profitability for companies making Duplex Board. For example, Smruti Kappa and Mondi are the leading Packaging companies who got benefitted due to e-commerce growth, improving European Industrial production.

Plastic Ban

Companies like Mc. Donalds have limited the use of plastic and encouraging more use of paper (shift to paper straws)

Hotel Chains are now focussing to eliminate plastic and shifting to glass bottle and paper-based products.

India is a growing country

The growth in the paper industry is linked to the growth of the economy. More Industrial Production translates into more demand for packaging boxes.

Over years, Indian Paper Industry hasn’t been able to compete with the international players on account of the higher cost of production due to a deficit in wood pulp availability, not enough availability of waste paper, etc. According to IPMA, the cost of domestic wood in India was higher by almost $30-40 tonnes as compared to other Asian Countries. Due to this single factor, the cost of paper production in India used to be higher by $100 a tonne.

By FY2010, the paper industry was facing a supply deficit. Hence, the companies started expanding capacities. the industry saw significant capacity additions of 1.6 million MT during FY09 – FY11 (~15% of domestic paper capacity in FY09), particularly in the Printing and Writing Paper segment. This led to an over-supply scenario, build-up of inventories together with pricing pressures. Moreover, there was also an issue in sourcing wood pulp. There wasn’t enough availability of wood pulp domestically for the new capacities added. As a result, companies had to import higher expensive wood pulp. The companies were unable to pass on the higher prices to consumers and at the same time also faced stiff competition from cheap imports. Profits were severely impacted, especially for leveraged companies. After this, the industry along with government measures has taken steps to be self-sufficient in sourcing wood pulp locally.

Indian paper industry is highly fragmented: the top 3 players account for only 9% market share unlike 68% in USA, 72% in Indonesia and 21% in China. The Indian Paper Industry should also consolidate gradually

Wood-Pulp

i.JK Paper (Writing, Printing and Packaging Board)

ii.West Coast Paper Ltd. (Writing, Printing and Packaging Board)

Positive – Expected Return of 12%+ on annualized basis in the long term

Neutral – Expected return in the range of +/- 12%

Negative – Expected return in negative

Disclaimer: Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Explaining, why this industry can do well, going forward

RHI Magnesita India Ltd.

Research Analyst – Gunjan Kabra (info@gunjankabra.com)

What led us to research this industry?

We did a top-down analysis at macro level and analyzed that Indian capex cycle can rebound. India’s capex cycle has been muted since last 10 years as private capex was flat. It was only the government capex that had supported infrastructure spending with 13% CAGR over FY10-20. What has changed now?

Investment cycle has bottomed out. Investment contribution to GDP has reduced to 26.7% in FY21 from peak of 36% in FY07.

Healthy Balance Sheet and Good Cash Flows of corporates

Accommodative Monetary Policy: Low cost of funds & Adequate Liquidity

High Demand from domestic as well as export markets

Cut in corporate tax rate for new capex (15%)

Reforms done in the past like RERA, GST etc.

Government initiatives to boost manufacturing activities like PLI Scheme, import substitution initiatives

National Infrastructure Pipeline of Rs. 1.1 trillion over FY20-25 which is twice of the total spending done in FY13-19.

China plus one strategy helping India to boost manufacturing activities

Indian Renewable/Clean Energy in focus

Government spending is the first to revive in any capex cycle. This gives confidence to private players to make expansion. Hence, we see an upsurge in capital expenditure. Order Flows for capital goods companies are growing.

For instance, Thermax Limited is engaged in the business of manufacture and sale of boilers, heating and cooling equipment, industrial chemicals, and water and waste management equipment. The following table highlights the order book trend.

JSW Steel, for instance, plans to spend around ₹28,000 crore to expand steel-making capacity from 24.5 million tonnes (MT) to 36.5 MT by March 2024,

Tata Motors is investing ₹28,900 crore in subsidiary Jaguar Land Rover and hydrogen fuel cell vehicles in FY2022.

PLI Scheme will be a key driver of Private Sector Investments

With rise in these infrastructure/construction activities, capacity utilisation of steel will increase. The share of building and infrastructure construction in overall steel consumption is 60-65%.

Staying true to our investment style, we have chosen a company whose product is irreplaceable, plays a pivotal role in the capex cycle, indirect play on the steel sector. This sector is less volatile when compared to steel with limited downside. The sector is Refractory Industry.

Understanding the Product: Refractories

What are Refractories?

Refractories are ceramic materials designed to withstand very high temperatures (exceeding 1,200°C) without undergoing physical or chemical changes while remaining in contact with molten slag, metal and gases.

In simple words, Refractories are used for lining furnaces, kilns, reactors, and other vessels which hold and transport hot mediums such as metal and slag.

How it helps?

Serves as a thermal barrier between the hot medium and the wall of containing vessel

Withstanding physical stresses(force) and preventing erosion of vessels

Providing thermal insulation

Protecting against corrosion

Improvement in production and performance

How important are refractories? Refractories are essential protectants for all heat-intensive production processes, including iron and steelmaking, cement production, glass, ceramics, aluminum, and nonferrous metals, paper and pulp, petrochemical processing, power production, and waste incineration. Without refractories, these industries and the products they produce would not exist.

Characterized as Consumable or Investment Goods: depends on the end user industry

Consumable Goods (75% of the total demand- Steel Industry)

Full Line Contracts which includes systems and solutions for complete refractory management

Demand is correlated to output

Mainly caters to Iron and Steel Industry

Investment Goods (25% of the total demand- Other Industries)

Longer Investment Cycles

Customized solutions based on the specific requirements of various industrial production processes

Project driven demand cycles

This point is explained in detail in the next points.

Critical product, yet represents 3% of COGS in steel manufacturing and less than 1 % in other applications. Why critical? Any failure in the refractories results in a great loss of production time and equipment. The type of refractories used also influences energy consumption and product quality. Hence, the issue of getting refractories best suited to each application is of highest importance. Economics greatly influences these issues. The refractory best suited for an application is best is not necessarily the one that lasts the longest, but rather the one which provides the best balance between initial installed cost and service performance.

An essential product in capex driven economic activity: Where is it used? 75% of the refractory demand comes from Iron and Steel industry and the remaining is from cement, glass, non ferrous and energy/environment /Chemicals.

The above table highlights the end user industry, the replacement cycle and the cost in making finished goods.

End-user Industry

Refractory Usage

2. Types of Refractories

Functional/Special Refractories

Competition is comparatively less in this segment

Other segments are quite competitive

This classification of refractories will help you to understand where is it used in the steel industry and also the margins vary of each product profile. This will also enable you to differentiate the product mix of refractory companies.

The focus is on iron and steel industry because the major demand and recurring demand comes from this sector.

3. Where is it used in steel industry?

In order to understand where refractories are used, it is important to understand the manufacturing process of steel. Here, I’ll be discussing the process in a broad sense to understand, how and where refractories are used while making steel.

Globally, steel products have been mainly manufactured via primary steelmaking process that constitutes two major routes. These are:

Blast Oxygen Furnace (BOF)- Primary Steel Making

Electric Arc Furnace (EAF)- Secondary Steel Making

Blast Oxygen Furnace (BOF)

It is a large integrated steel making facility where primary steel is produced. It is useful in making bulk quantity and good quality. These plants are large in capacity ranging from 1to 5 million tonnes per year are spread in large areas. They can take advantage of economies of scale.

Major Raw Materials: Iron Ore (80-90%), Coking Coal

Other Materials: Limestone, Scrap Steel (10-20%)

How steel is made in this method?

The coke along with iron ore and limestone is heated in Blast Furnace to form pig iron.

The molten iron along with steel scrap is added to the Blast Oxygen Furnace where it is further refined. Oxygen is blown onto the molten iron and converting into molten steel.

Steel ladle is used to transport liquid steel from BOF/EAF and also act as a reactor where refining of steel takes place to reduce impurities, carbon, alloy addition. Here, different alloys like Ferro Manganese and Silico manganese are added.

After completion of secondary refining of steel in steel ladle, the liquid steel is transferred from steel ladle to tundish through the slide gate flow control system. Slide Gate valve is used in tundish also to control the liquid flow from tundish to moulds. The ladle flow control system is consisting of the following items:

Ladle nozzle

Slide gate plates

Collector nozzle

Electric Arc Furnace (EAF)

EAF have a much simpler input process.

Major Raw Materials:

Scrap Steel

Graphite Electrodes (a device to conduct electricity to melt scrap)

Direct Reduced Iron (DRI)

EAF (Electric Arc Furnace) use electric arc with high power to generate the required heat to melt the steel scrap of recycled and transform into the desired composition of steel. The steel-making process on EAF is not dependent on the BF production since the actual input is scrap steel and certain quantity of pig iron and graphite electrodes.

The steel produced from the BOF and EAF is again refined to get the required chemical composition; these are secondary refining processes of steel making. Step iii. & iv. mentioned in the BOF section is same in both.

Refractory Application for Steel Ladle

The numbers in the picture refers to the numbers mentioned in the above types of refractories table.

This table gives a good idea of the types of refractories used in the vessels/components by the methods of steel production.

4. Raw Materials Used

Principle raw materials used in the production of refractories are:

Brown Fused/ White Fused Alumina (manufactured from Bauxite: Not the same alumina used in manufacturing aluminium)

Magnesia

Silicon Carbide

Zirconia

Understanding the Refractory Industry in detail

Industry Characteristics:

Fragmented Industry

In last 6 years, IFGL Refractories have gained market share by 0.8%. While Vesuvius India and Tata Krosaki Refractories have lost market share by 3% and 5.3% The share of RHI Magnesita India remained same. 70% of the refractories consumed in India are locally produced and 30% are import dependent. Out of which 2/3rd is imported from China.

High Entry Barrier Business

Since, it is a critical raw material, relationship with buyer is very important

Customer Stickiness

Product Quality is very important as explained above

Continuous R&D is required to be more efficient , only large players have this capability

Raw Material security is very important

Consumable Product, less volatile over long term Steel Production will happen irrespective of the steel cycle. The fixed cost of shutting down the plant during downcycle is quite high. Hence, the steel plants will continuously run and the demand for refractories would be stable. The profitability of the steel cycle varies depending on the cycle. This explains why refractory industry is less volatile and consistent.

Consistent Growth seen in Refractory Business irrespective of steel cycle

Notes:

The growth rate in RHI Magnesita India in 2020 and 2021 is not comparable as there was a merger

The growth rate was negative in Vesuvius India in 2020 and 2021 as the company lost market share

Overall, we can say that refractory business is an indirect play on steel industry and capex cycle with less volatility.

2. Supply Side Dynamics: Understanding the Raw Material Industry

Raw Material Security is challenging: Around 40% of the raw material is imported from China by refractory players in India. For RHI India it is around 20-25%. Raw material security has been a problem in the industry even before COVID. The pandemic has accelerated the trend of shortage of raw material. Generally, the rise in raw material prices can be passed to the companies as the % to COGS is quite low. This happens with a lag.

Benefit of Vertical Integration: The companies who have integrated mines are the ones who are expected to perform well in the coming years. This can lead to consolidation in the otherwise fragmented industry. The graph below depicts the benefit of vertical integration in the refractory industry

Recent Trends:

Volatile Raw Material Prices: Prices of raw material has increased because of supply chain disruptions from China, high freight costs.

Shift to other countries for procuring raw material: In one of the recent interviews, VP of Tata Krosaki stated that “We still depend on China for alumina and magnesia based refractory raw materials, But, we have slowly moved to other destinations.” Other destination includes Europe, Brazil, South Africa and Turkey, but the cost is 30-40% higher. The company with integrated mines will benefit as they have raw material security and margin expansion. For instance, RHI Magnesita India has mines in Brazil, Turkey and Europe which makes for 40% of the total raw material requirement for the India plant. Around 20-25% is imported from China and rest is sourced locally. For peer companies like IFGL, they don’t have their own mines and is dependent on China for their 40% of the material requirements. Vesuvius India also faced shortage of raw material.

Recycling of raw materials leading to cost savings: Use of recycled refractory materials will lead to savings in raw material costs by almost 30%. Companies like RHI Magnesita India have upto 12% usage of recycled raw materials. The availability of the same is scarce and not all players will be able to scale up the usage. RHIM has acquired magnesia recycling facility in Cuttack. The company who provides complete business solutions will benefit more.

Explaining why this industry can do well, going forward

Shortage of Raw Material can lead to consolidation in the industry: As mentioned, companies who have captive mines can survive and benefit on account of

Raw Material Security: less import dependent and high localisation

Superior Margins

2. The industry is moving towards full line contracts under Total Refractory Management (TRM) services or complete business solution model. Steel companies prefer this model. Here, the company provide a broad range of tailored services at customer sites such as refractory installation, recycling, digital and supply chain services. These drive process efficiencies, reduce costs and generate sustainable benefits, thereby creating value for customers as well as for the companies.

RHI Magnesita, the parent company is now providing this service in India too through RHI Magnesita India. Vesuvius India and TRL are other players who provide this service.

This is a big change and how will this benefit?

Refractories installation is technical. Attention to detail is crucial for a proper refractory installation. For instance, how much water needs to be mixed, temperature control while installation, adequate storage, drying out process. If the installation isn’t correct, the refractory lining will crack and weaken quickly resulting in risks to workers and refractory projects. Steel Companies would need a skilled refractory installation contractor for proper refractory installation.

Every refractory project is unique and needs customisation.

Model II: Dual benefits to Steel and Refractory companies:

Refractory Companies- Scope to gain market share and easy availability of recycled material

Steel Companies- can get customised refractory solutions as working with the refractory manufacturers directly. Right usage of refractory materials can improve production and efficiency.

Globally, refractory companies only provide complete installation to steel companies. RHI Magnesita India is trying to bring the same model to India. It would be easier for companies who has a complete basket of refractories to provide such services.

Why Refractory Maintenance Practice is important?

Refractory maintenance practice is important to maintain availability and extend campaign life. Materials for maintenance are very important as the volume of the maintenance materials consumed over a campaign may be up to two times the volume of original brick. Maintenance helps to balance the wear of refractory lining due to excessive wear in an area of repair whether the damage done mechanically or chemically

A typical cost curve is shown in the figure. The brick cost shows the cost of lining if the maintenance is not considered. Total cost is increasing from brick cost when the vessel is becoming old. There is a possible end of campaign in the absence of maintenance at a life of 4000 heats.

The life is extended to 12,000 heats by maintenance.

3. Steel Production is expected to remain high on account of:

Revival in capex cycle leading to higher economic activities as explained in the beginning of the report.

Strong export demand for steel and less import because of China plus one strategy and supply chain disruptions.

RHI Magnesita India Ltd.

Why RHI Magnesita India ?

Market Leader in Indian Refractory Market with ~15.9% market share

Can be a direct beneficiary of the expected consolidation in the refractory industry (market leader)

Total Refractory Services (TRM) can contribute significantly to revenues and margins as the company is moving towards this service. The benefit of this is highlighted above. This will also help the company to cater to large players.

Superior Margins than peers and comparatively lower on cost curve on account of

Well knit global supply chain network

Vertical integration: Captive Mines leading to better raw material sourcing compared to peers. Hence, superior margins. We have seen this in the above section. Vesuvius India and IFGL are dependent on imports from China for their raw material requirement. RHI Magnesita India can source its raw material from parent company, RHI Magnesita. Further, localisation and recycling is leading to reduced demand from imports.

R&D Facility: Established R&D in Bhiwadi in Nov 21. The aim is to develop 3 new products in the shaped refractory products.

Better capacity utilisation than competitors: Industry Capacity Utilisation is around 50-60%. The company is operating at 85% capacity utilisation.

Better Product Mix is also leading to higher margins: The company is into Tundish Management which is a niche area where it gets higher margin. Almost 15 percent of its business comes from managing the process flow control for the steel companies which again is a very high margin business.

Slide Gate Refractories: Special Refractories Slide Gate Plate Refractories are installed on the ladle’s bottom for regulating the flow of liquid steel from Ladle to Tundish.

Isostatic Refractory: a high margin business, also used in exports Refractory components for the protection of steel from oxidation reactions and other environmental contaminations in the transfer process from laddle to tundish and from tundish to continuous casting machine.

Capacity Expansion Plan: The company has recently announced a capacity expansion plan of Rs.400 crores for the next 3 years. The focus of the parent company is on the Indian market. The company aims to make India as the manufacturing and R&D hub for its Asia and Africa market. According to management interviews, the company plans to increase around 25-30% of the total capacity every year. In one of the articles, it was also mentioned the company can make acquisitions too.

2. Installed Capacity and Planned Expansion

Cuttack Plant: The company acquired a plant at Cuttack manufacturing Magnesia Bricks in 2019. . The company plans to increase capacity by de-bottlenecking in phased manner from 10k tonnes to 18k tonnes. This is part of ORL. Benefit of this plant:

Magnesia Bricks are highly imported. Domestic demand is around 300k tonnes. 75% is imported from China. This will increase localisation helping in import substitution.

Higher heat resistance than Alumina bricks

Cost Savings due to recycling

Bhiwadi Plant (Rajasthan): Manufactures High Margin Products like Slide Gate and ISO This is a part of Orient Refractories Ltd.

It does Contract Manufacturing (Cost +10%) for RHI Entities

Geography Wise Revenue: Exports: 60%, India: 40%

Installed Capacity as on FY21 is 65000 tonnes Expansion: 25000 tonnes(Q3 FY23)

Scope of Margin Expansion is less

Caters to Steel and Cement Industry

RHI India: It’s a trading company sourcing from various RHI entities.

3. About the Company

RHI Magnesita India Ltd. has been incorporated in 2021 with merger of three RHI entities

Orient Refractories Ltd.

RHI Clasil

RHI India Pvt Ltd.

In 2013, ORL was acquired by RHI, Austria. Prior to this Rajgarhia family owned and managed the company. Post the acquisition, ORL was able to improve efficiency and quality and take advantage of the strong network globally. In 2021, the company got merged with other unlisted entities in India.

Geography Wise Revenues: India- 75% Exports- 25% The company plans to increase export share to around 30-35% in 2-3 years.

4. Key Risks

Volatility in Raw Material Prices

Downturn in Steel Industry

5. Management Quality

The company should at least have 50% independent directors in the BOD Committee. RHI Magnesita India has 3 out of 7 as independent directors.

The audit committee is chaired by Independent Director

Remuneration as a % of PAT is optimal

6. Competitive Scenario

Vesuvius India Ltd.

Installed Capacity: 2,75,000 tonnes

Raw Material: Import Dependent The company is operating at low- capacity utilisation The company has lost market share in last 5 years.

Product Mix:

Special Refractories constitutes a small portion in total sales

IFGL Refractories Ltd.:

IFGL Refractories Ltd. is a leading manufacturer of specialised flow control refractories.

Installed Capacity: 27 lakh pieces of shaped refractories and 52k tonnes of Unshaped Refractories.

Products Overview:

Isostatic Refractories

Slide Gate Refractories

Tube Changer System & Refractories

Nozzles

Monolithics & Cast Products

Raw Material: Import Dependent (40-45%)

Market Share: 5.8% in 2015 to 6.6% in 2021

Expansion plans:

Odisha: Rs. 10 crores for normal capex by debottlenecking H1 FY23

Kandla: Rs, 10 crores in HY22

Vishakhapatnam: Project cost of Rs. 30 crores have been completed Q2 FY22 (48000 tonnes) Project cost of Rs. 20 crores is expected to be completed by Q2 FY23

Why RHI Magnesita India over IFGL?

Financials – IFGL Refractories Ltd.

TRL Krosaki Refractories Ltd. (Unlisted Player)

The product mix is good, focus is on domestic market with a large market presence in stainless steel market. But the same is not reflected in EBITDA Margins and the company has been losing market share since 2015.

RHI Magnesita India has a strong presence in Special Refractories.

Financials – TRL Krosaki Refractories Ltd.

Calderys India (Unlisted Player)

Subsidiary of France based Imerys Group.

The company is more into unshaped refractories

Imports raw material from China

40-45% of the total revenue comes from iron and steel industry

Revenue in 2020- Rs. 662 crores

Financials – Calderys India

Dalmia Refractories Ltd. (Unlisted Player)

Product Mix catering to cement and iron & steel industry

Products: Bricks & Castables

Financials – Dalmia Refractories Ltd.

RHI Magnesita India Ltd.– Financials

Income Statement

RHI Clasil Ltd: Financials

RHI India Pvt. Ltd. : Financials

Outlook Interpretation –

Positive – Expected Return of 12%+ on annualized basis in the long term

Neutral – Expected return in the range of +/- 12%

Negative – Expected return in negative

Disclaimer: Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Builds on the growth momentum through a Higher Multiplier Effect (Manufacturing, Digitization and Sustainability)

CAPEX to continue to drive growth

The Indian economy is expected to grow at 9.2 per cent in FY22. The priority in the budget was to sustain the high growth. The major thrust was on reviving the capital expenditure cycle in the country. The rise in capital expenditure helps to crowd in private investment. The virtuous cycle of investments begins in the economy. Capex has a higher multiplier effect on economic output over revenue spending. The capital spending push will also induce demand for services and manufactured inputs from large industries and micro, small and medium enterprises (MSMEs), while helping farmers through better infrastructure. The focus is on building infrastructure, housing and promoting digital economy.

15% lower tax rate for new manufacturing units got extended for one more year till March 2024.

Low Income Housing: Allotted Rs 48,000 crores for FY23 under PM Housing scheme.

Tap Water in Homes: Allocation of Rs 60,000 Cr. has been made to this scheme in 2022-23 to cover 38 million homes.

68% of defense procurement budget kept for domestic private industry.

The launch of 5G auctions in 2022 will help boost telco sector and the classification of data storage as infrastructure spending is expected to benefit telecom companies

Our View

Import Substitution: The focus is to boost domestic manufacturing. Here, the government increases custom duty in certain products, includes some sector in the PLI Scheme like Renewables, Defence, Textiles and Electronics to name a few.

Push on building infrastructure: Increase in demand for capital goods, building materials, cement etc.

Higher capital expenditure would mean higher capacity utilization of steel and other metals.

Focus on Exports: The pandemic has certainly built a framework for India to find a pivotal place in the global value chain in some sectors like Chemicals and Textiles.

Staying true to our investment style, we’ll focus on companies where competition is limited, plays a pivotal role in the manufacturing process and an indirect play on the expected high growth in a broad sector.

2. Transportation and Logistics: link to growth of trade and economic activities

Focus on building roads, building railway network for swifter movement of goods and services

The expansion of the national highways network by 25,000 kms

Railways will offer new products for small farmers and MSMEs, integrate coastal and railway network.

400 new “Vande Bharat” trains in three years

100 PM Gati Shakti cargo terminals will be developed in the next three years.

The budget aims to spend Rs. 20,000 crores under PM GatiShakti Master Plan.

This is expected to benefit key infrastructure and logistics players.

3. A GREEN BUDGET for the greener future

Energy transition, energy efficiency, electric mobility, and supporting renewable energy infrastructure was the key theme of the budget 2022-23. Promoting energy transition and climate action was one of the key focus areas.

280 GW solar capacity target by 2030 – Under PLI Scheme, the government approved the proposal of an additional allocation of Rs. 19,500 crores.Earlier allocation wasRs 4,500 cr. The government will give priority to fully integrated manufacturing units from polysilicon to solar PV modules.

25% and 40% BCD on Solar cells and Solar Modules to promote domestic manufacturing of solar modules. This is a big step. And, we believe it will help India to become a leading player in the solar equipment manufacturing industry.