Niveshaay’s Approach in the Valuation Reset Market Mood

June 07, 2022 | Industry Insights

Follow

Follow

Whenever there is a correction in the market, the first question that comes to our mind is, “Is it a good time to stay invested or is it better to pull out of the market?”

We tend to make analogies from past market corrections and study the macro factors causing corrections. Isn't it? Let us put things in perspective. The tightening of monetary policy by FED and now by RBI, inflationary environment due to the Russia-Ukraine conflict and COVID-19 led supply chain disruptions have created the current market environment volatile. We don't know whether there would be more downfall or not, but what we at Niveshaay think is that, few factors have become quite favourable for the country to find a pivotal place in the global value chain. The current environment doesn’t augur well for businesses that require a consistent supply of capital to grow. Is it a good time to invest?

In the Indian context, corporates now have healthy balance sheets. It seems like, the focus of a lot of companies is to have a balance sheet characterised by low leverage. Labour demographics, cost of manufacturing is steadily becoming competitive and we’re a huge market. The most often used phrase after COVID-19 ‘China plus one’ looks structural and persistent providing tailwinds to the manufacturing sector. The export of engineered goods, steel, textiles and building materials to name a few have increased tremendously after the pandemic and from the pre-covid levels too. Acceptance of any product increases when one gets an opportunity to try and experience new products. India just got that and few companies totally grabbed these favourable opportunities to provide to international as well as domestic clients. With government focus on manufacturing and exports, reviving the capex cycle and taking measures to attract private capex are just some of the needed pre-requisites for growth.

Japan became the second largest economy globally in 1970-1980s, led by a strong central government, rapidly growing manufacturing sector and protective and supportive trade policies. In early 2000’s China was the net importer of metals and of many other products. Slowly, with supportive government policies and manufacturing cost advantages, China built out a massive network of factories dominating the global trade surpassing Japan to become the second largest economy. With COVID-19 led supply chain disruptions, emerging countries like India are getting opportunities in the export markets. India has twin benefits- we’re a huge market plus the ability to export competitively in few sectors.

Our approach in the current market mood is to focus on cash flow generating companies, reasonable valuations and healthy balance sheet.

Secondly, investment decisions shouldn't be made in stocks that look cheap on the basis of hope that things will turnaround in 1-2 years. Hope is never a strategy and such companies generally are de-rated in markets which is brutal as we’re seeing in the current ones. We truly believe that current times are such where one should invest where there is a visibility and predictability of earnings.

Lastly, not to over-allocate to correlating sectors, follow the basket approach wherever required and keep a high margin of safety.

Themes, which we believe are expected to perform well include:

Capital Goods / Metal Ancillaries: Revival in capex cycle, Import Substitution at play -Indian engineering components exports grew by 37% when compared to 2019 and grew to $ 111 billion in 2022, a rise of 50% from 2021 levels. The major thrust of government during the last two years has been to revive the capital expenditure cycle. The rise in capital expenditure helps to crowd in private investments. The virtuous cycle of investments begins in the economy. With higher steel and energy prices globally and supply chain disruptions, India can reap benefits from the government support through PLI schemes and import substitution policies additionally with export markets. Insights from visiting various exhibitions, interaction with varied entrepreneurs and management conference call discussions also highlight how imports of raw materials have reduced and domestic sourcing has increased wherever possible. Also, capital goods companies are showing healthy order-book at a time when government policy of export duty on steel translating to reduction in steel prices in home market would help these steel consuming companies in a significant way. Overall, till date, the earning season has been fantastic where few companies have shown good sales growth, maintained or improved margins. Some companies did show margin pressure too. The focus should be on companies that exhibit pricing power. This is also the time when global companies in the developed economies are incurring margin pressure. We truly believe that Indian manufacturing will be the best quality asset to own across the globe as an asset class.

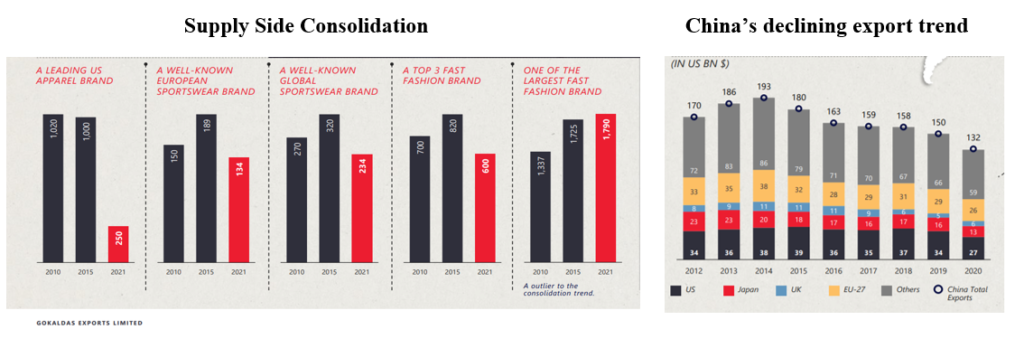

Textiles: Government focus, supply side consolidation and China+1 at play -

Currently, play on apparel segment in the textile value chain looks good. India’s annual textile exports can rise to $100 bn in the next five years from the current USD 40 bn as per Ministry of Textiles. Garmenting requires low investments when compared to setting up spinning, fabrics and processing units.

Renewable Energy: Good for the Planet and a Great Business to Invest in -

This sector has been our focus area since a long time now. Transition to clean energy is certainly the buzzword in the global economy. Why has it suddenly become so important than ever?

Well, COVID-19 accelerated the clean energy adoption trend and also made us realise that the shift to green energy is fuelled by necessity. In addition, the Russia – Ukraine war also highlighted a quick shift to renewables is important. The use of renewables in place of coal will save India Rs. 54,000 cr. ($8.43 bn.) annually by 2040. Renewable energy will account for 55% of the total installed power capacity by 2030. Countries like India and Europe, which are fuel dependent on other nations, did realise the need to fill in the gaps after the energy supply disruptions for greater security after the pandemic and the war period. Hence, definitely, it’s a long-term and integral play for any economy to achieve sustainable growth.

Building Material Industry: Product gaining market share and the industry is expected to grow at a CAGR of 15-20% in next 3-4 years -

Here, the play is on MDF industry where the product is a substitute for plywood and doesn’t have any threat from imports. Being, 80% cheaper compared to plywood, the industry is gaining huge traction due to the increase in housing demand, growth of online home décor platforms and reduction in furniture cycle time.

Staying invested amidst these short-term hiccups will make a huge difference in the long term. Meanwhile, we’ll continue to stick to our process and give our one hundred percent always.

Happy Investing!