RUSHIL DECOR LTD.

April 16, 2022 | Stock Talk

Follow

Follow

| Research Analyst: Ramswaroop Agarwal (rsa0308@gmail.com) & Kartik Mediratta (Kartikmediratta64@gmail.com) |

When promoters buy-back, it is a positive sign. But, when the competitor companies’ promoters take stake in the peer company that significantly boosts investor confidence as they are the most clued people to know about the industry prospects. This keenly watched attribute adds to the assurance factor for the investor. This scenario is being seen in the emerging MDF industry. The leading MDF players like Century Plyboards and Action Tessa have bought stake in Rushil Décor.

The strong conviction of industry leaders towards the growth of the MDF industry and their confidence in Rushil Décor is one of the many reasons why we think that this company can perform well in future. The report aims to discuss the industry and business model in great detail.

SHAREHOLDING OF PROMOTERS OF PEER GROUP (as on 30/09/2021)

Note:

- Promoters of Century Plyboards have acquired 1.37% stake in RDL in Q1 FY22 and subsequently acquired additional 4.02% stake in Q2 FY22.

- Promoters of Action Tessa have increased their shareholding in RDL by 1.71% and 0.15% in Q1 FY22 and Q2 FY22 respectively.

- This trend seems to be continuing in the subsequent quarters as well.

ABOUT COMPANY

Rushil Decor Ltd is the flagship company of the Rushil Group. Rushil Decor Ltd was incorporated on May 24 1993 as a private limited company with the name Rushil Decor Pvt Ltd. The Rushil product portfolio includes Laminates, Medium Density Fiber Boards (MDF), High-Density Fiber Boards Water Resistant (HDFWR), Pre- laminated Decorative MDF Boards and PVC Boards.

Rushil Décor Ltd. is one of the leading company in Laminate and MDF panel boards industry in India with a global foot print in and around 42 countries.

It has 6 manufacturing facilities across West and South India focusing on different product segments. The units are strategically located which assist in the smooth procurement of raw materials which is proved to be the significant factor in cost effectiveness.

INVESTMENT RATIONALE

1. Rapid Pace of Urbanization: As a nation of 1.39 Billion people, India has demonstrated quicker recovery trends in demand as far as consumption of staple commodities, high-end necessities such as electronics, home furnishing as well as luxurious goods such as automobiles are concerned. Especially, the demand for home décor and electronics has been steadily climbing up, as people have been forced to remain within the confines of their homes due to the lockdowns and their swift adoption of the work-from-home trend. Rapid urbanization has also contributed to exponential growth in the real estate sector. It is estimated that there is a shortage of around 10 Million housing units in urban India. According to industry research, supply of additional 25 Million units by 2030 is required to meet the growing urban demand. This growth potential is expected to percolate to allied industries such as consumer goods and home décor industries.

2. Robust Demand and Entry Barriers: The MDF and PVC segments are fast growing owing to their inherent strengths and advantages. There is a huge opportunity in terms of market growth as well as import substitution. The MDF segment has high entry barriers especially in terms of required capex. Hence, there are a few unorganized players in the MDF segment and the industry is more than 90 percent organized.

3. Housing For All’ and Development of Smart Cities: Such programs will drive construction of large number of houses across India, leading to additional demand for furniture. It is estimated that India will receive investment of approx. $1.3 Trillion in housing sector over the period of next 7 years. Notably, the investment would lead to construction of new 60 Million houses.

4. Atmanirbhar Bharat: The Indian government’s commitment to encourage selfreliance is intended to develop Indian industry and reduce imports. In turn, we believe that this platform could deepen India’s industrialisation, strengthen incomes and widen the consumption play.

5. Urban Real Estate Growth: The Indian real estate growth has underperformed its retrospective average in recent years. However, the Work From Home phenomenon has increased the priority of buying into bigger and better homes, kickstarting sectorial growth from the second quarter of the last financial year, which is expected to increase the offtake of interior infrastructure products.

6. New Plant: Company has set up a new MDF manufacturing facility at Andhra Pradesh with capacity of 800 CBM per day. For this, company incurred a capex of approximately Rs. 450 crores. This will help Company to cater large set of customers which in turn will strengthen the market share of Company. The new plant is equipped with latest German technology which will consume 8-10% less raw materials thereby reducing the total cost of inputs and will lead to higher margins. According to industry experts, the Replacement Cost of Rushil Decor’s Andhra Pradesh plant is approximately Rs. 650 Crores.

7. IKEAZIZATION of Furniture Industry: IKEA is an internationally known furniture and home furnishings retailer. IKEA entered India in 2018 and is expanding since thereon. IKEA is sourcing 20% of its products which are made in India and the same is expected to reach 30% within 2-3 years. The furniture which they procure is made up of only MDF and particle boards, majorly MDF and the use of plywood is negligible. Due to more demand in MDF sector this would definitely unleash the inherent potential lying in the industry.

For a detailed understanding on Indian Furniture Industry & Indian MDF Industry, visit our blog:

MDF Production in India

Due to sustained momentum in demand as well as prices, manufacturers are getting a clear revenue visibility, despite some price war in the market space. The capacity utilization in the industry has also gone up by 15% to 20% (i.e. 70-75% in 2021, which is expected to improve to 80-85% by 2025).

Industry experts believe that demand for MDF will match the increase in production capacity within the next couple of years. MDF’s market share will further bolster with the rising prices of Poplar Timber, a chief source of economy grade plywood in North India. It is expected to gain market share of Low & Medium grade plywood (which constitute 85% of the Plywood market in India).

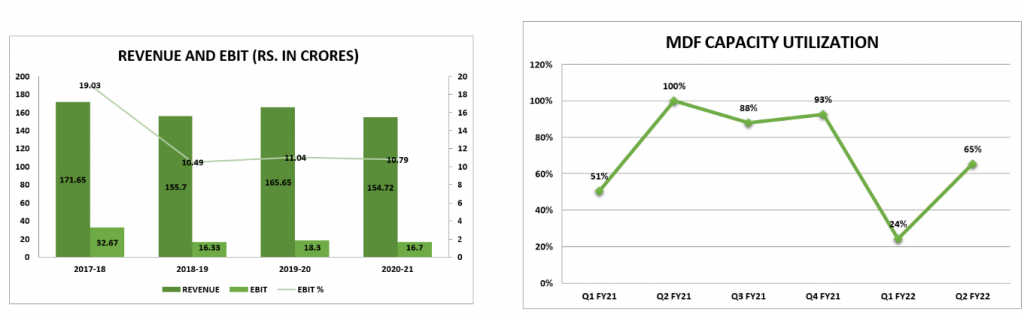

MDF Segment of Rushil Décor Ltd.

Rushil décor is India’s third largest manufacturer of MDF. It has state-of-the-art manufacturing facility, one at Karnataka with total capacity of 300 CBM per day and another one at Andhra Pradesh with total capacity of 800 CBM per day. Thereby taking the total capacity to 1,100 CBM per day or 3,30,000 CBM annually. It incurred capex of Rs.450 crores for setting MDF manufacturing unit at Andhra Pradesh. The regular commercial operations were started from March’21. This plant will help Company increase market share and take care of incremental demand generated in Industry. The new plant is equipped with latest German technology which will consume 8-10% less raw materials and will play a key role in reducing total input costs therefore strengthening overall margins. Also, the company has vast network of 100+ distributors, 50+OEMs and 1000+ dealers.

Note: Capacity Utilization has declined in Q1 FY22 as the new plant at Andhra Pradesh has commenced operations in March 2021 and is yet to achieve optimum capacity utilization. Management has guided an overall capacity utilization of 65% for FY22.

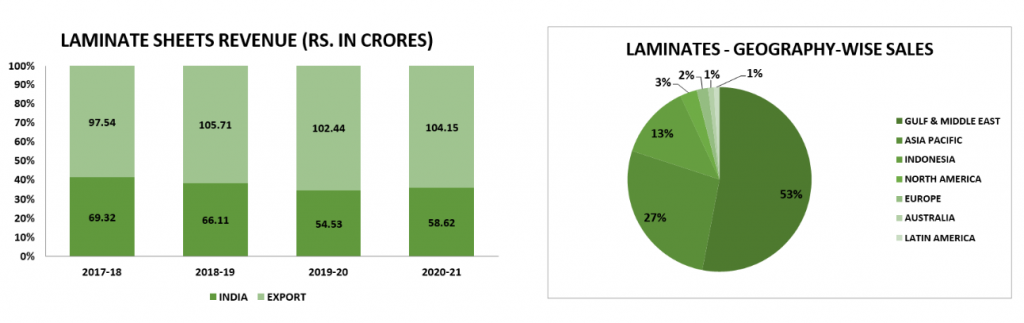

LAMINATES

- Laminate sheets are made by bonding together two or more layers of materials. Laminate sheets from plastics are glued to wood to make the surface aesthetic. These sheets are manufactured by laminating different types of papers with formaldehyde. The core sheet consists of Kraft paper with phenol formaldehyde (PF) and below it, a barrier paper is provided. Above the Kraft paper, a tissue paper is impregnated with FF melamine formaldehyde (MF) resin is provided which gives protection and also enhances abrasion resistance. Then, these laminates are bonded to wooden surfaces with suitable glue and pressing for some time finishes the process.

- Laminates provide a better surface finish for furniture elements and also provide an attractive look for a very less price. Furniture like tabletops, cupboards, surfaces of chairs mostly uses laminates as the finish material.

Types of Laminate Sheets:

- High-Pressure Laminate (HPL): The layer of the laminate adheres to substrate under pressures of 70 to 100 bars at temperatures of 280° to 320° Fahrenheit using adhesives. The laminates are available in thickness 0.8 mm, 1.0 mm and 1.5 mm in standard sizes 1.2 m x 2.5 m. These laminates are most durable, flame retardant, and consists high level of resistance to heat and chemicals.

- Low-Pressure Laminate (LPL): The layer of the laminate adheres to substrate under pressures of 20 to 30 bars at temperatures of 335° to 375° Fahrenheit without using adhesives. These laminates are less durable, thinner than HPL, flame retardant, resistant to heat and chemicals and comparatively very cheaper than HPL.

Applications of Laminate Sheets

Laminates Industry

The global market size for decorative laminates is estimated to be worth USD 91,015.03 Million by 2025, registering a CAGR of 5.3%. On the global demand map for decorative laminates, China and India are leading from the front as their huge demand emanates from their enormous population base, growing urbanization and mass- scale construction activities in residential as well as commercial real estate sector. Consumption of Indian panel products has grown at CAGR of 15-20% for organized sector.

Indian Laminate market size is Rs. 5000 Crores. Major chunk of market is enjoyed by the unorganized sector due to low-capital intensive industry. Apart from voracious consumer demand, implementation of tax reforms such as GST is expected to aid the organized manufacturers capture a larger market share as against their unorganized counterparts.

Production Capacities of Top Organized Players:

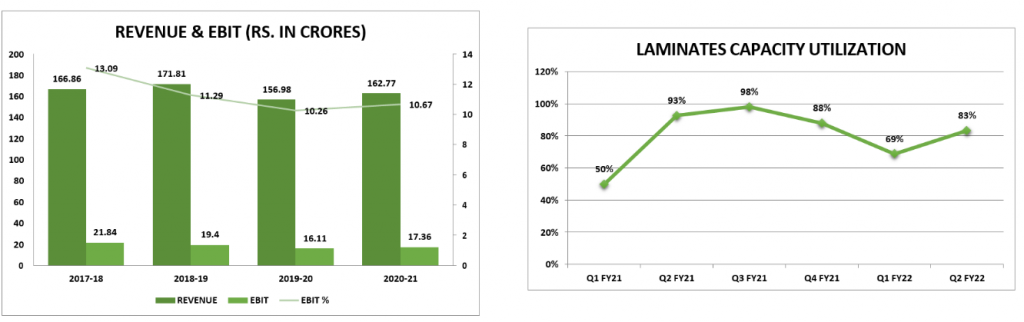

Laminates Segment of Rushil Décor Limited

Note: Capacity Utilization is lower in Q1 FY21 and Q1 FY22 due to 1st and 2nd wave of Covid19 pandemic in Q1 FY21 & Q2 FY22 respectively.

POLYVINYL CHLORIDE (PVC)

- Poly Vinyl Chloride (PVC) is a high-strength synthetic resin made from the polymerization of vinylchloride. It’s a sheet made of plastic composite that’s extremely durable in its purest form. The first thing that comes to mind when PVC is mentioned is pipes and plumbing material. However, PVC is also an extremely versatile material, one that is used for flooring, cabinets, countertops and more.

- It is in very high demand in building and construction industry because of its multifaceted use in windows, doors, sidings, roofs, wires, cables, pipes and fittings. Such a wide variety of applications emerges from PVC’s safety, quality, durability and cost effectiveness as a material. PVC is light weight, tough, easy to mould, strong material that resists corrosion,rotting or adverse impacts of weather effectively. For the similar reasons, the PVC boards are also high in demand as they give highly aesthetic look after finishing and are economically priced.

Uses of PVC Foam Sheets/PVC Foam Boards

- Used for the ceilings of Cars, Buses or Trains

- Widely used for making home and office furniture

- Used to build external wall panels

- Home interiors can be designed using PVC foam boards

- Used in sign boards and outdoor advertising kiosks

- Used in Construction, Garage Doors, POP Displays, Exhibit Spaces & Signage

Advantages of PVC Foam Boards

- Water Resistance: PVC foam boards have solid resistance to water due to its composition. When it comes in contact with water, it does not swell or lose its composition. This makes is fit for all types of weather.

- Corrosion Resistance: When brought in contact with chemicals, PVC doesn’t react. This keeps its state intact and saves it from any kind of deformation.

- Fire Resistance: PVC foam boards can be used anywhere as they are fire resistant. There is no effect of acid, heat or light on it.

- High Strength & Durability: Due to the structure of its component molecules, PVC foam boards are highly strong which ensures that they don’t undergo any deformation. The boards can survive for as long as 4 decades without any damage.

- Easily shaped and painted: PVC can be given any shape to suit your requirements. It can be cut for the furniture of your house or can be made into wall panels for exterior use. Also, it can be painted with any type of paint which lasts for years and gives the look and feel as if it is new!

- Pocket-friendly: They are a good substitute for wood or aluminium and they come in a variety of price range. They don’t require any extra maintenance and stay in the same state for quite a long time. No special equipment is required to cut or drill them and this makes them pocket-friendly to use.

PVC Market in India

Though in fledging stage, the market for PVC boards in India is gradually expanding with the size of the market touching nearly Rs. 2000 Crores, before the pandemic of COVID-19 hit..

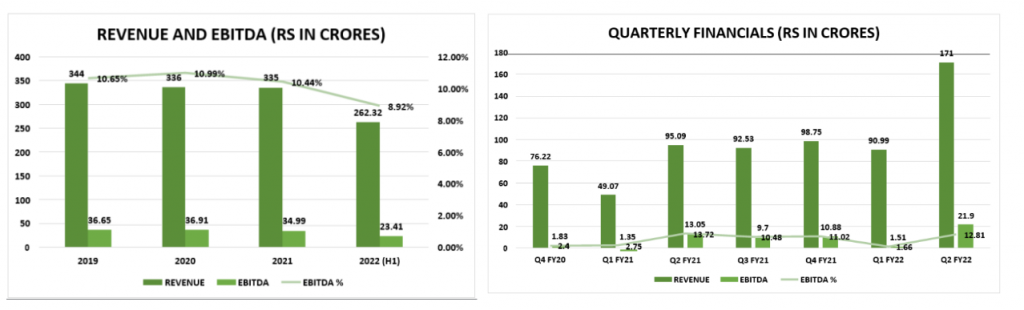

COMPANY FINANCIALS

Notes:

- EBITDA margins have declined in Q1 FY22 and H1 FY22 as the company has commenced commercial operations at its new MDF manufacturing plant at Andhra Pradesh leading to higher costs. These costs are expected to taper down gradually with improved capacity utilization.

- Finance Costs and Depreciation have increased from Q1 FY22 onwards due to commencement of operations at the new plant at Andhra Pradesh and cessation of capitalization of Interest expenses of the new plant which are now being charged to Statement of Profit & Loss.

Financial Ratios:

Debt Repayment Obligation:

RUSHIL DECOR V/S NIFTY SMALLCAP 250:

VALUATION

Notes:

- Total EV of Rushil Décor is Rs. 1,160 Crores. However, approximately 25% of this value is contributed by its Laminates Segment. Hence, EV for MDF segment = Rs. 870 Crores.

- Since, Greenpanel is the market leader in MDF industry with strong brand value and extensive dealer networks, it deserves a higher valuation than Rushil Décor. So, our target EV per ‘000 CBM is at 50% discount to Greenpanel.

* This should be the Fair Value based on current capacity of the company’s MDF segment. These values are subject to periodic revision based on improvement in capacity utilization of the new plant and the company’s ability to set up efficient dealer networks for its products thereby driving growth in revenue and EBITDA margins.

SCENARIO ANALYSIS

Notes:

- The above tables show the effect of improved capacity utilization across the 3 segments of the company on its revenue and EBITDA margins over next 2-3 Years.

- Under the Moderate Scenario, the MDF segment is expected to operate at 75% capacity. In this case, the topline is expected to double and the EBITDA margin will increase to approx. 15% due to improved operational efficiencies.

- Under the aggressive scenario, the MDF segment is expected to operate at 85% Capacity. In this case, the topline is expected to multiply 2.5X and EBITDA margin will improve to approx. 20%.

RISKS AND THREATS

- High Competition

- The industry in which the Company operates has intense competition, especially from the unorganized sector in the plywood and wood panel segment as around 75% of the market players are still unorganized.

- Companies like Greenpanel and Action Tessa are the market leaders in MDF. They enjoy strong brand value and vast dealer networks. Significant difficulties could be faced by Rushil Décor to penetrate in the markets of these companies and expand its dealer network.

- New Entrants: For the laminate segment, entry barrier in terms of required capex is pretty low. There always remains a pressure of new entrants getting in the organized market, which has been the case, leading to higher competition.

- Raw Materials: With increasing urbanization, deforestation is taking a toll on the raw material availability. Further, erratic monsoon has played a role in suppressing the raw material supply. Rising crude price has been another reason leading to an increase in raw material prices.

- Man power crunch: Manpower availability in case of Laminates has been one of the most- impacted matrix of operation for this industry and for the Company more so in the wake of the pandemic. Most migrant labourers left for their respective home locations and many of them are yet to return leading to labourer supply shortage. Moreover, skilled manpower is scarce and availability is an issue.

- Overcapacity in MDF Industry: MDF being the lustrous business segment, bestowing the higher margins, has always provided the exposure to new entrants. With the entrance of new comers the MDF market is exploited with over-supply and thus the realization per unit crashes thereby leading to trembling of margins.

- Import Menace:

- Imports has always been a cause of trouble for domestic sellers as the importers provide par quality product, as to what domestic merchants are providing, but at considerably low costs. Prior to the pandemic, India imported 30% of its MDF demand. Post- Covid imports of MDF and Laminates fell sharply to 15% due to the surge in logistics costs particularly the container cost. This momentary surge in prices is expected to taper down in the upcoming period and imports may resurge to the pre-covid levels.

- Companies like Greenpanel and Actiontessa mainly operate in North India which provides them a strong location advantage in terms of protection from imports due to higher logistics costs to transport imported MDF from ports to North India. Thus, these companies continue to be a major threat for Rushil Décor to penetrate in different regional markets in India.

Outlook Interpretation

Positive – Expected Return of 12%+ on annualized basis in the long term

Neutral – Expected return in the range of +/- 12%

Negative – Expected return in negative

Disclaimer:

Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.