India’s ambitious goals of achieving 500 GW of renewable energy capacity by 2030 and becoming a net-zero economy by 2070 underscore the critical need for advancements in grid management. The deployment of smart meters is essential for this transition.

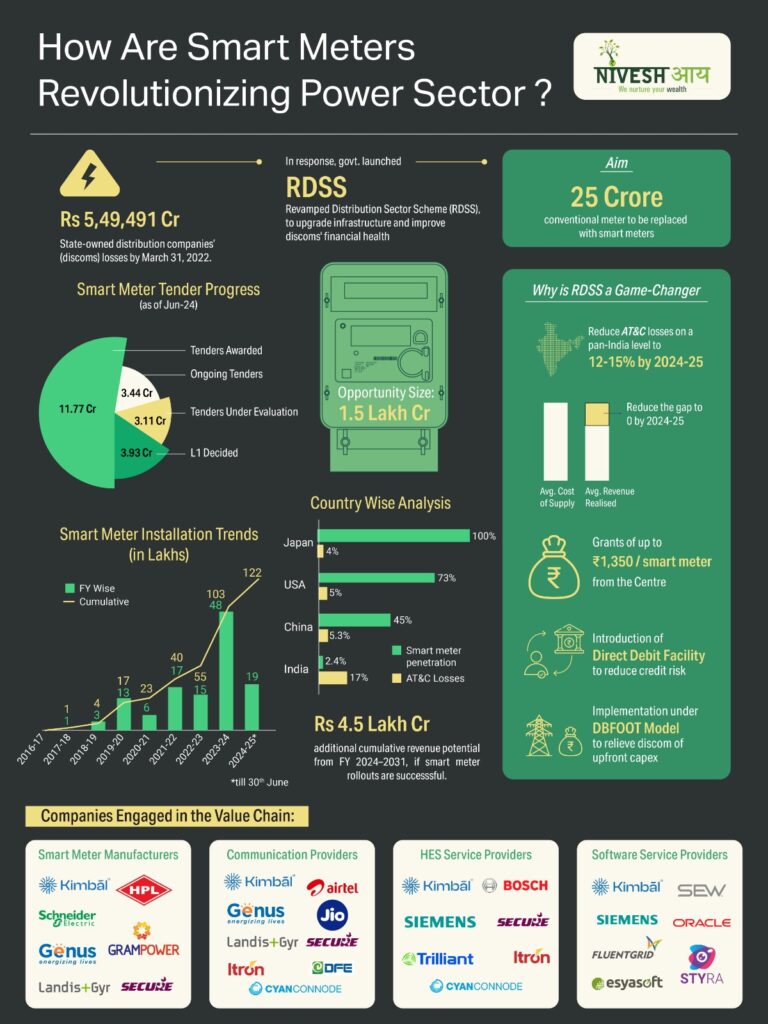

The Indian smart meter market is experiencing unprecedented growth, driven by a strong governmental push for grid modernization and energy efficiency. The target of installing 250 million smart meters highlights the scale of this transformation.

To gain key insights, we attended the Smart Metering Summit 4th edition, where we engaged with various industry players across the smart meter value chain. Here are key insights from the event:

Opportunity and Execution Status

Investments : The smart meter program is set to draw €17 billion (₹1.54 lakh crores) in investments over the next five years for smart meter installations.

Current Progress and Global Penetration: As of July 2024, only 12.6 million out of 222 million sanctioned smart meters have been installed in India. While smart meter penetration in developed countries like the USA is around 80%, the installation is growing at a faster rate in emerging markets like India.

Successful Implementation Factors:

For India’s smart meter program, efficient network coverage is vital, with RF, Cellular, and NB-IoT technologies playing key roles. India uses RF and Cellular based on regional needs. Cloud solutions must be well-sized and balanced between IaaS, PaaS, and SaaS for effective data management. Cybersecurity is critical to protect data and system integrity. Additionally, maintaining system reliability while managing costs is essential for a durable and cost-effective smart meter rollout.

Challenges that the industry is facing:

Infrastructure Integration and Scalability: Integrating smart meters with existing, often outdated, infrastructure and ensuring they are scalable and compatible with various technologies.

Cost Management and Grid Stability: Balancing the costs of deployment, maintenance, and upgrades while maintaining grid reliability, especially in areas with frequent power fluctuations.

Data Protection: Safeguarding consumer data from unauthorized access and cyber threats.

Consumer Education: Educating consumers about the benefits and addressing concerns related to smart meter installations.

Thebenefits of smart meters extend beyond just reducing Aggregate Technical & Commercial (AT&C) losses. These include:

Theft Deterrence and Accurate Billing: Smart meters help reduce electricity theft, a significant issue in the Indian power sector, while providing precise consumption data that minimizes billing disputes and enhances customer trust.

Operational Efficiency and Usage Insights: Smart meters offer accurate billing, efficient energy usage tracking, and peak load management. They also facilitate quick response and resolution of power outages, while providing valuable insights into usage patterns for better demand forecasting and grid management.

In a nutshell, industry stakeholders including utilities, Advanced Metering Infrastructure Service Providers (AMISPs), Original Equipment Manufacturers (OEMs), communication solution providers, and software and cybersecurity experts—expressed a unified optimism at the substantial rollout of smart meters in India. Their collective enthusiasm reflects confidence in overcoming challenges and achieving significant advancements in grid management, operational efficiency, and consumer engagement through this massive deployment

The Union Budget 2024 is themed around the roadmap for the pursuit of ‘Viksit Bharat,’ aiming to generate employment, enhance financial stability, improve credit access, and foster overall economic growth, making it a unique model of self-propelling growth strategy. While tax adjustments are part of the new policies, the focus remains on supporting sustainable corporate growth and economic stability. The government’s continued emphasis on enhancing the company’s earning potential reflects a commitment to ensure long-term success and resilience.

Moreover, the budget’s initiatives to stimulate consumption through generating employment in the economy signal a proactive approach to economic health and welfare. To reduce the gap between receipts and expenditure, the government needs to do a balancing act. India’s fiscal deficit for FY24 was ~5.63% of the GDP which the government aims to bring down to 4.9% of the GDP for FY25 and below 4.5% of the GDP by FY26.

The budget announcement has introduced several policies and measures aimed at different segments of society and the economy. While the comprehensive budget addresses various sectors and stakeholders, our focus will be on examining the specific policies and initiatives that directly impact our investment strategies and allocations. Our analysis will assess the budgetary decisions, offering insights into how such changes will guide our approach.

PART A

1.Push for Energy Transition to continue

The government has continuously prioritized sustainable energy over the last two tenures and the current budget also maintains its focus on initiatives for energy storage, solar rooftops, nuclear energy, and aiding small industries in cleaner energy transitions.

Energy storage: This year’s budget emphasizes energy solutions, including pumped storage, to tackle the variability and intermittent issues of renewable energy. Multiple tenders are anticipated, boosting opportunities for pumped storage manufacturers, project financiers, and EPC contractors involved in these projects.

Solar: Solar energy is thriving with strong government support, targeting 280 GW by 2030. Currently, ~85 GW has been installed, and we anticipate continued momentum as execution remains a focus. The ‘PM Surya Ghar Muft Bijli Yojna’ aims to install rooftop solar in 1 crore households, providing 300 free units of electricity monthly, already attracting 1.28 crore registrations and 14 lakh applications. This is expected to boost domestic solar component manufacturers and EPC players, aided by budget measures like a 10% Customs Duty on solar glass (w.e.f October 2024).

Nuclear reactors: The future energy mix will prominently feature cleaner sources like nuclear energy. The government, in collaboration with the private sector, will focus on establishing and advancing nuclear projects, including the R&D of Bharat Small Reactors. Funding for R&D, as announced in the interim budget, will support these initiatives.

Advanced Ultra Super Critical Thermal Power Plants: The development of Advanced Ultra Super Critical (AUSC) thermal power plant technology, which offers higher efficiency, has been completed. A joint venture between NTPC and BHEL will build an 800 MW commercial plant using AUSC technology, with government fiscal support. This is expected to foster indigenous production of high-grade steel and advanced materials, benefiting the economy.

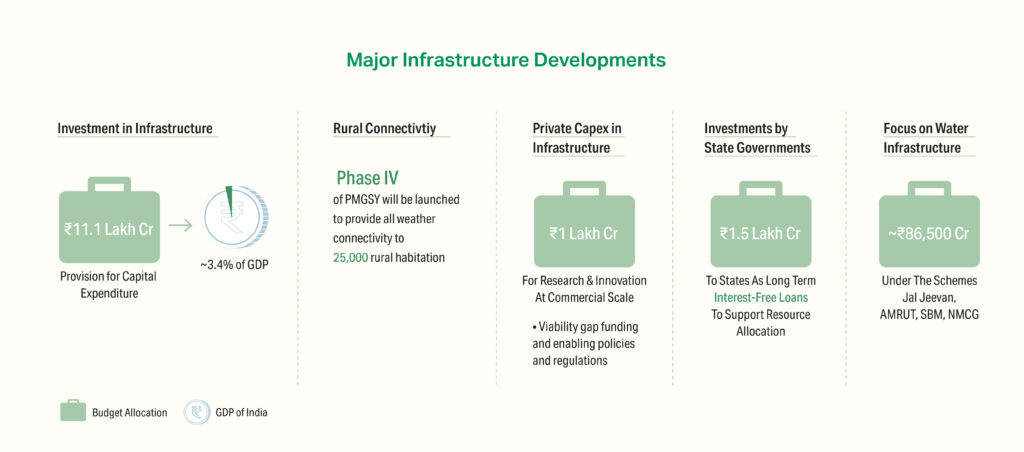

2.Major Infrastructure Developments on the Horizon

The budget emphasized a comprehensive development initiative called ‘Purvodaya’, targeting the overall growth of Bihar, Jharkhand, West Bengal, Odisha, and Andhra Pradesh.

Despite previous delays, the government remains steadfast in fulfilling the Andhra Pradesh Reorganization Act’s promises, including developing Amaravati as the state capital and completing the Polavaram Irrigation Project. The government’s focus and significant expenditure in this sector highlight the potential for local and regional companies involved in infrastructure, particularly those in cement manufacturing and EPC services, to be well-positioned to be major beneficiaries of this development.

Additionally, the government is transforming Bihar with new airports, medical colleges, sports facilities, and the ambitious Patna-Purnea Expressway. These projects, costing ₹ 26,000 crore, aim to reshape the state’s transportation landscape.

To further boost infrastructure development in India, the government has decided to partner with State Governments and Multilateral Development Banks to promote water supply, sewage treatment, and solid waste management projects in 100 large cities.

The removal of Basic Customs Duty (BCD) on ferro nickel and blister copper, along with the continuation of a nil BCD on ferrous scrap and nickel cathode for another 2 years, aims to reduce the stainless-steel production cost and is also positive for domestic cell manufacturing.

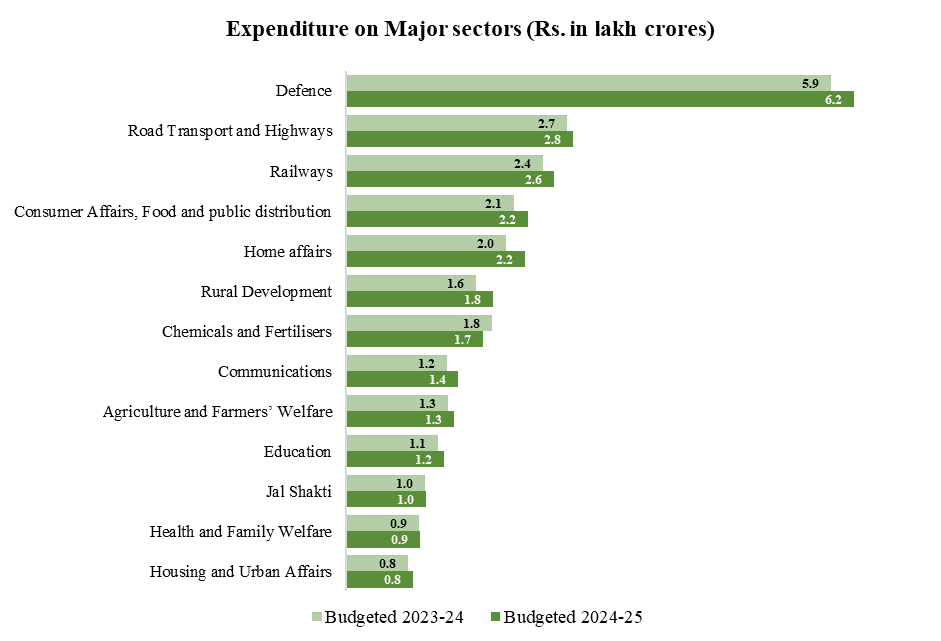

The government has earmarked ₹11.1 lakh crore, a ~10% increase from the previous year’s allocation, to enhance India’s infrastructure, with a significant focus on rural development, including ₹2.66 lakh crore specifically for rural infrastructure.

With the government’s focus on robust fiscal support for infrastructure,we remain optimistic about sectors like capital goods, equipment manufacturers, EPC contractors, cement companies, metal companies, and other infrastructure-related industries.

3.Manufacturing and services

Railways

The recent budget has unveiled a historic capital expenditure allocation of ₹ 2,52,000 crores, marking a 5% increase compared to the previous year. This strategic investment is aimed at modernizing the infrastructure and enhancing service capabilities like the addition of new lines, Broad-gauge (BG) conversion, High-Speed Rail Corridor, etc. The increased allocation reduces reliance on external sources and borrowing, fostering greater self-sufficiency within the sector. This is expected to significantly benefit companies involved in manufacturing railway components, as well as strengthen the overall safety and efficiency of railway operations.

Defense

The Defense budget has received an allocation of ~₹ 6.22 lakh crore, a tad higher than last year. The ministry is targeting to spend on acquiring new weapon systems for the armed forces, including fighter aircraft, ships, submarines, drones, and specialist vehicles. This increased budget is expected to propel the growth of the Defence companies which may also create a positive ripple effect to companies who provide its products to such defence companies.

Electronics

India had exported just ₹ 12,800 crores of mobile phones in FY2019, which increased 19 times to ₹ 2,40,000 crores in FY2024. With a government outlay of ₹ 6,200 crores PLI scheme for electronics manufacturing and reduced custom duty from 20% to 15% on mobile phones, Printed Circuit Board Assembly (PCBA) of mobile phones, and components such as chargers/adaptors, will strengthen India’s competitiveness globally. This is expected to benefit mobile phone assemblers and electric component manufacturers by giving competitive manufacturing prices.

Textiles

The Budget allocates ₹4,417.09 crore to the textiles sector, up from ₹3,443 crore last year. This includes customs duty cuts and other incentives to drive growth. With current exports of technical textiles at $2.5 billion, India aims to reach $10 billion in five years. Additionally, duties on accessories for manufacturing textile and leather products for export will also be removed which are expected to lower production costs and enhance the competitiveness.

Telecom

The Indian government is actively promoting domestic manufacturing in the telecom sector with an outlay of ₹ 1910.80 crore in the PLI. To further support this, import duties on telecom equipment components (PCBAs) have been increased from 15% to 20%. These changes are designed to incentivize domestic manufacturing and support the cable, tower, and telecom equipment industries, and enhance India’s self-reliance in the telecommunications sector.

Pharma

The government’s commitment to strengthen the pharmaceutical sector is evident with the increased PLI scheme outlay to ₹ 2,143 crores from the previous outlay of ₹ 1200 crore. This substantial outlay, coupled with committed investments of ₹ 5,000 crores from the industry, will not only support India’s drug supply chain but also create new job opportunities and foster innovation in the sector.

Medical Equipment and Medicines

The government has fully exempted three cancer medications from duty and reduced the duty on medical equipment, such as X-ray tubes and flat panel detectors from 15% to 5%. Additionally, all types of polyethylene used in the manufacture of orthopaedic implants are now free from customs duty. These measures will benefit the patients and depict the government’s commitment to social reforms.

4.Agriculture and Allied Industries to benefit

The government prioritizes productivity and resilience in agriculture under Vikshit Bharat, planning to enhance productivity and develop climate-resilient crops through revamped research and competitive funding, including private entities.

Key initiatives include releasing 109 high-yielding crop varieties, promoting natural farming for one crore farmers, achieving self-sufficiency in pulses and oilseeds, developing vegetable production clusters, and establishing a digital infrastructure for agriculture. Financial support for shrimp production and a new National Cooperation Policy are also planned.

Additionally, the fertilizer subsidy has been reduced by 13.2% from the FY24 revised estimates, including both Urea and Nutrient Subsidies. This reduction may slightly negatively impact the fertilizer industry.

Overall, the budget allocation of ₹ 1.52 lakh crore allocated for agriculture and allied sectors is expected boost productivity, promote sustainable farming, enhance market access, and stimulate rural economic growth, ultimately leading to increased food security, better farmer incomes, and a more resilient agricultural sector.

5.Employment as a catalyst for holistic growth

The budget’s allocation of ₹ 2 lakh crores over five years aims to empower 4.1 crore youth through employment and skilling initiatives.

These measures are expected to significantly reduce youth unemployment, enhance economic growth, and improve India’s global competitiveness by bridging the skills gap through a comprehensive internship program in top companies.

This is expected to positively impact rural consumption and boost overall economic activity. Such initiatives are also anticipated to strengthen non-discretionary consumption, further supporting economic growth.

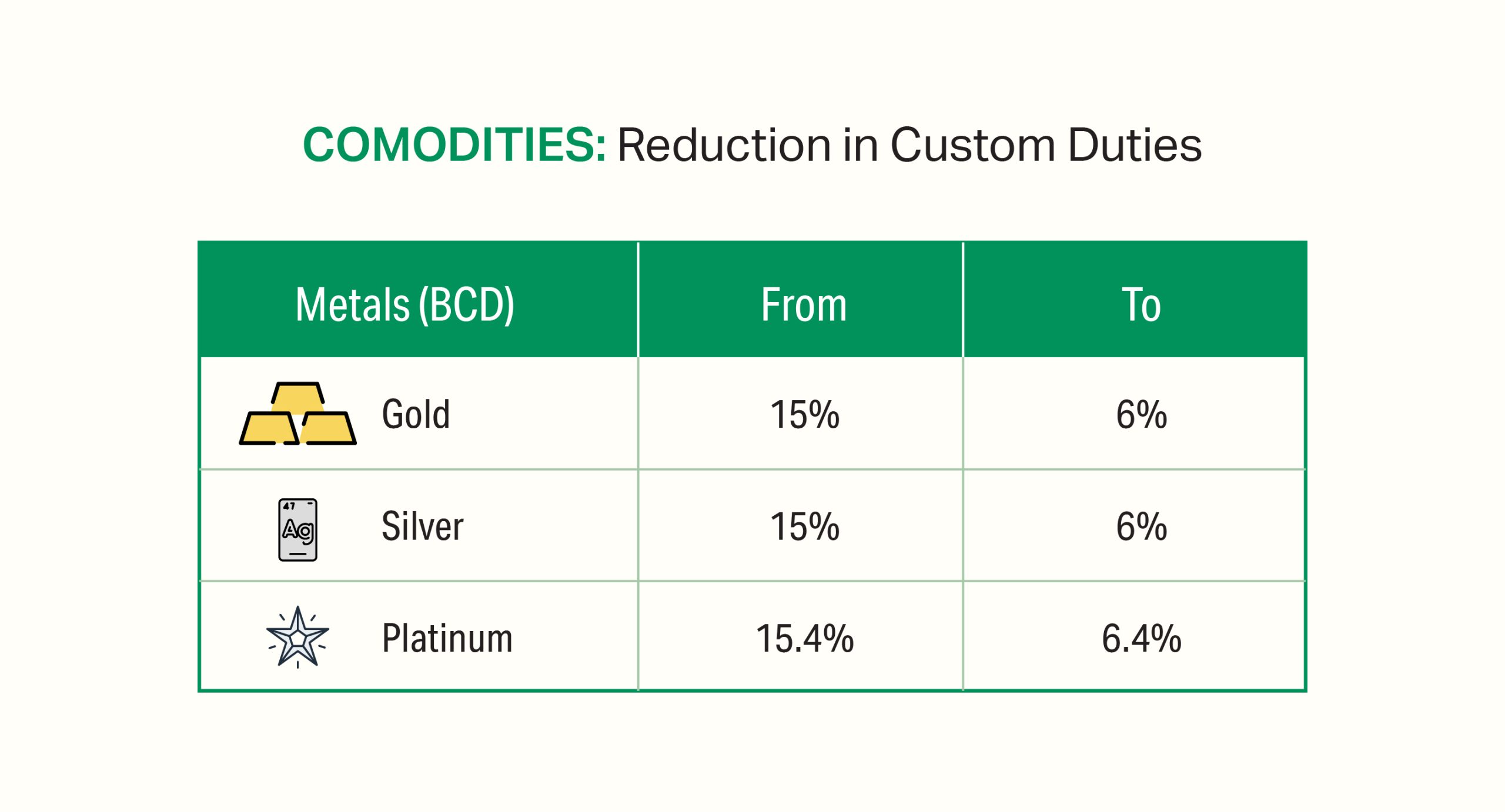

6.Commodities

The recent significant duty cut is anticipated to benefit the domestic jewellery market by boosting demand, lowering prices, and encouraging increased investment in precious metals. By reducing smuggling and fostering a more competitive market, the government aims to create a conducive environment for jewellery businesses to thrive.

PART B

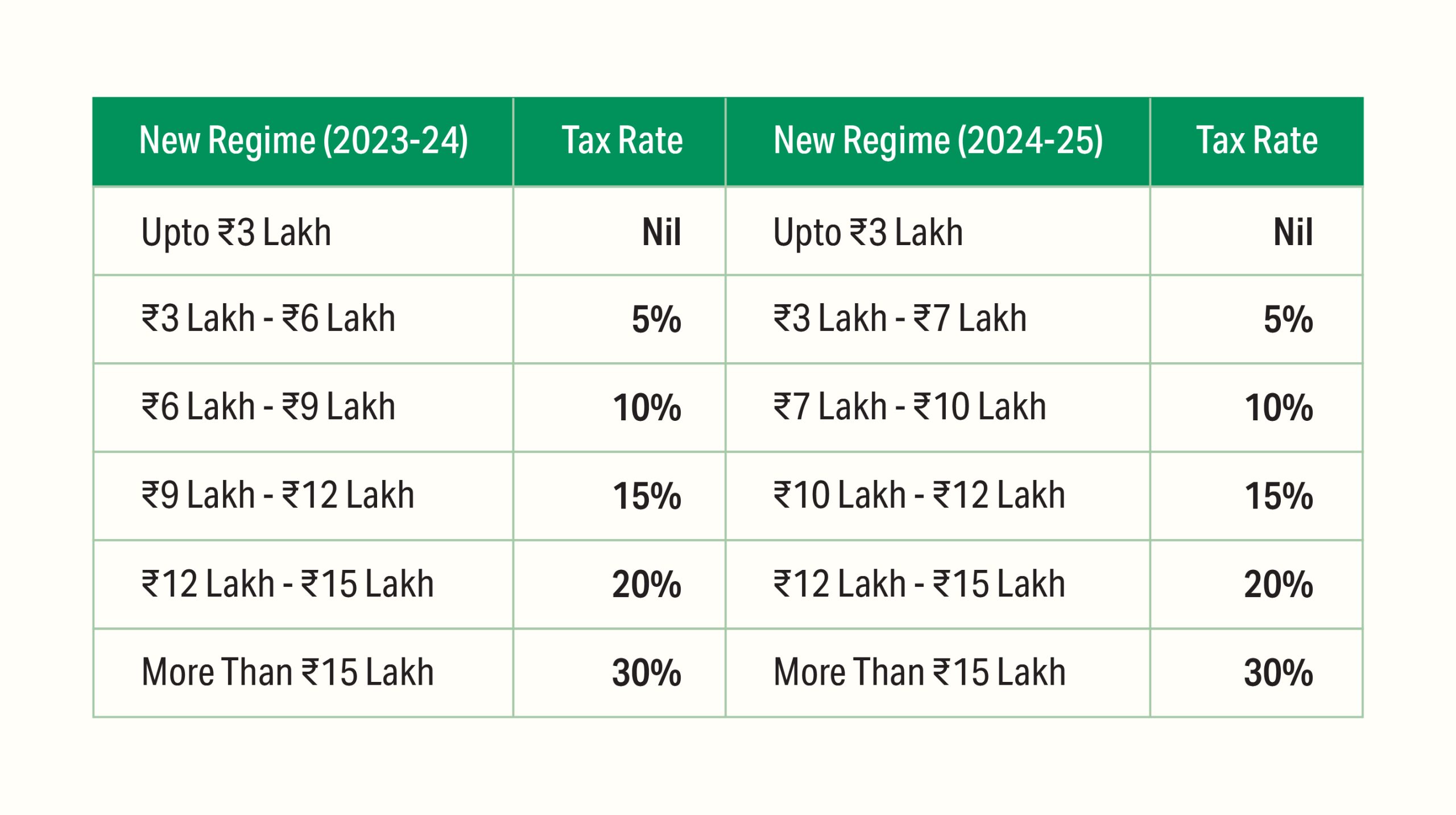

In 2022-23, over 58% of corporate tax revenue came from the simplified tax regime, and more than two-thirds of taxpayers have adopted the new personal income tax regime.

The revised tax slabs are expected to save salaried employees ~₹17,500, taking into account the standard deduction.

The standard deduction for salaried employees is proposed to be increased from ₹50,000/- to ₹75,000/-.

Similarly, the deduction on family pension for pensioners is proposed to be enhanced from ₹ 15,000/- to ₹ 25,000/-

This will provide relief to about four crore salaried individuals and pensioners.

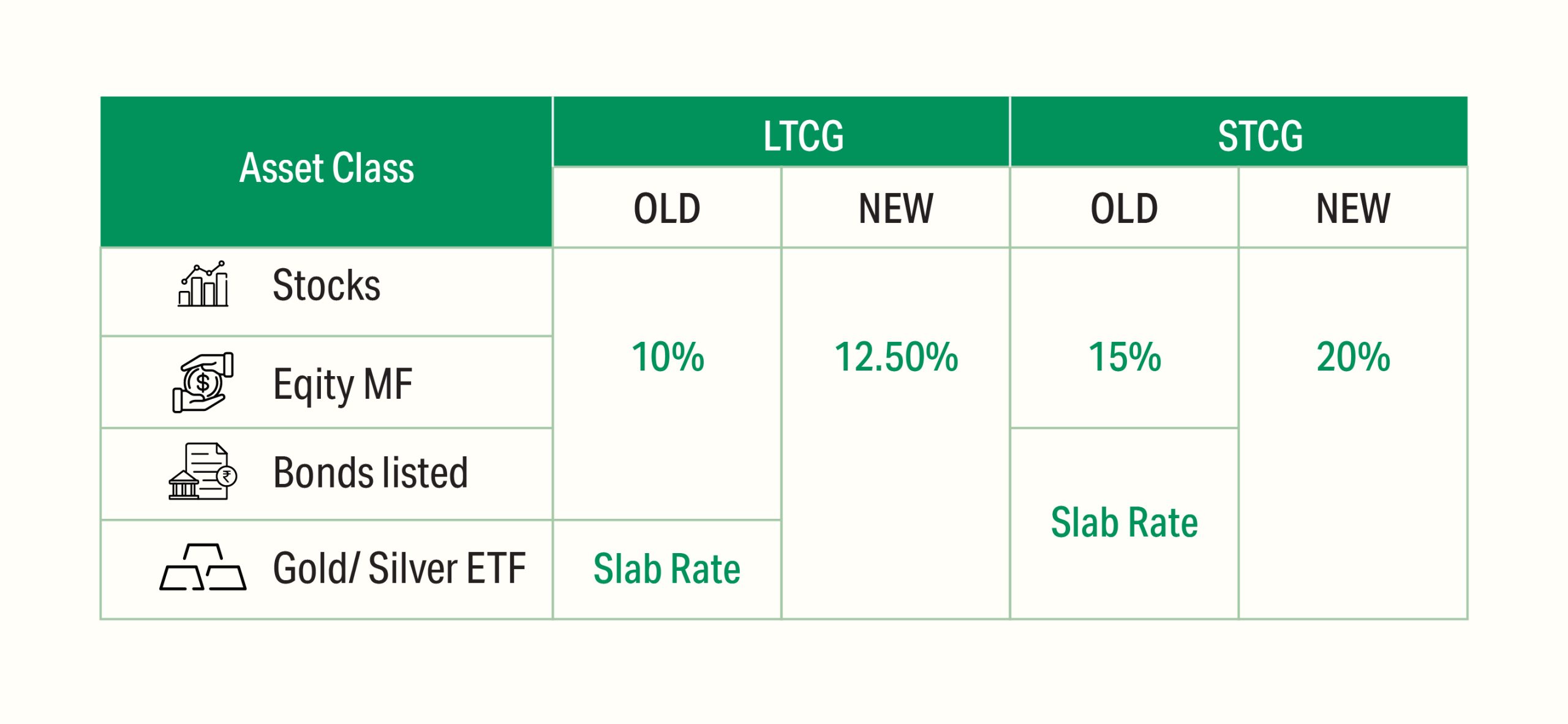

The finance minister has also removed the indexation benefits previously available for property sales and reduced the Long-Term Capital Gains (LTCG) tax on property from 20% to 12.5%. While this may impact short-term investments, it aims to simplify the computation of capital gains for both taxpayers and tax administration.

India’s tax reforms reflect a commitment to creating a conducive environment for economic growth. India is attracting investments and encouraging industrial development by reducing corporate tax rates, particularly for new manufacturing units. The simplified personal income tax regime has reduced compliance burdens and has been well-received by taxpayers, indicating a positive shift towards a more efficient tax system.

In 2018, when the capital gains tax was introduced, adverse economic conditions occurred, and there were high corporate debts. Still, today’s resilient economic environment and strong corporate balance sheets support our confidence that these policies will drive further growth.

In comparison to developed countries, India’s tax rates are competitive, and its ongoing reforms are positioning it as an attractive destination for business and investment, signaling a robust trajectory toward development.

“Water is life’s matter and matrix, mother and medium. There is no life without water.”

India is home to a whopping 18% of the world’s population, but it only has about 4% of the world’s resources. With cities growing and industries booming, the country’s water demand is set to skyrocket from around 1040 BCM (billion cubic meters) now to about 1447 BCM by 2050. This surge in demand is made worse by problems like groundwater depletion, climate change, and poor water reuse and recycling practices. To make sure everyone has access to clean and safe water, it’s vital to invest in water and wastewater infrastructure. This will help us make the most of our water resources and tackle the looming supply challenges.

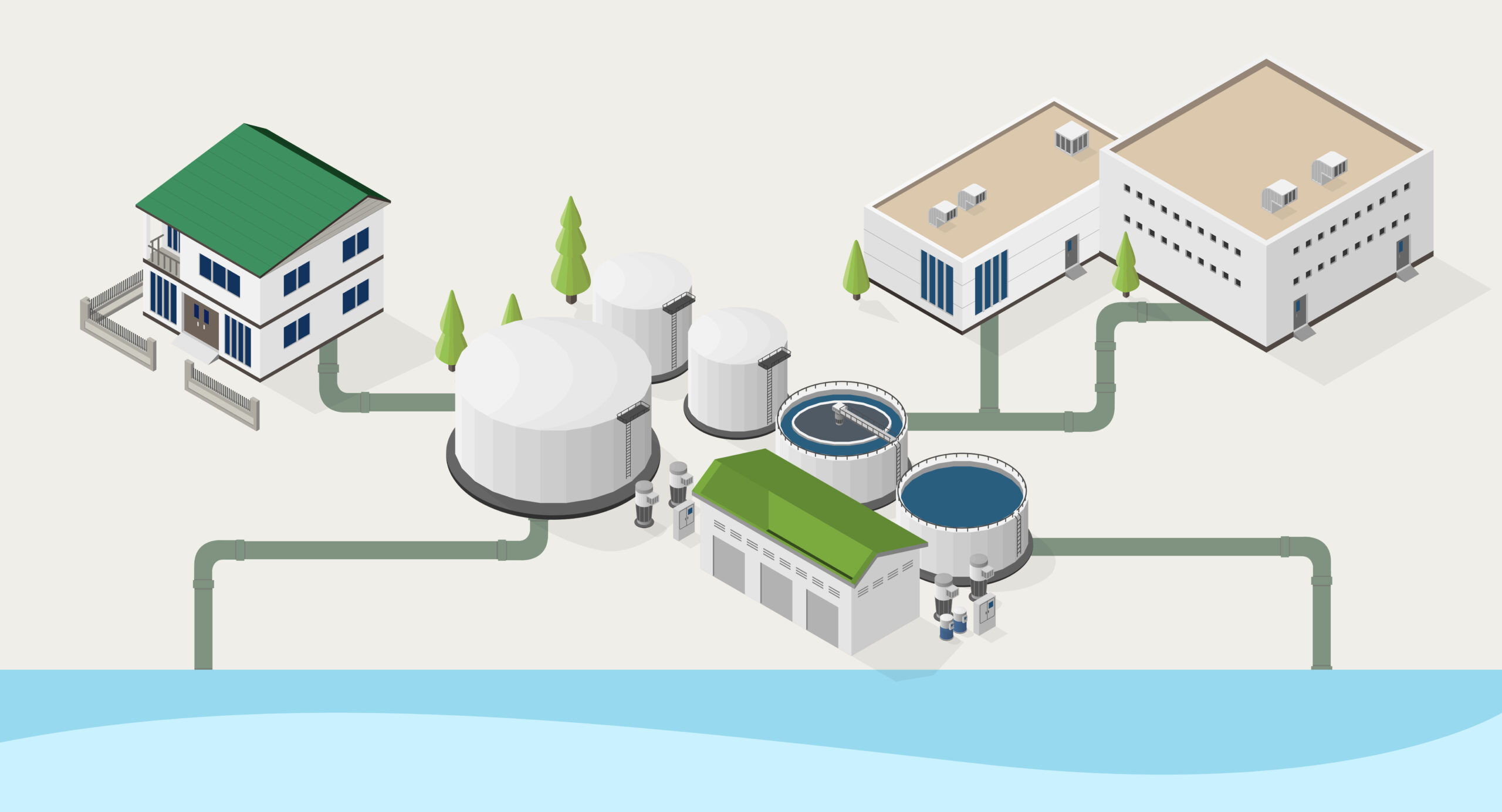

Basic understanding of the value chain

Here’s a quick rundown of how the water/wastewater treatment industry operates:

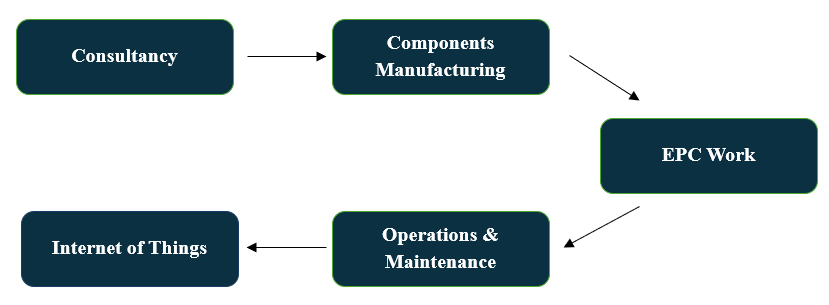

Consultants – The Planners: First up are the consultancy firms. These companies kick things off by analyzing the area where a Sewage Treatment Plant (STP) or Water Treatment Plant (WTP) will be built. They look at the local population, how much sewage is generated, and other key factors to figure out the plant’s required capacity and other necessary things. They then draft up layouts that show the plant’s capacity, location, treatment technology, and a survey of the pipeline network.

EPC Companies – The Builders: Next in line are the Engineering, Procurement, and Construction (EPC) companies. They take the consultants’ plans and start building the WTP or STP, along with the necessary pipelines. They handle everything from getting materials to actual construction. Some EPC companies stick to engineering and procurement and hire others for the construction part. On bigger projects, even those that do handle construction might subcontract parts of the job. These companies usually also manage the operation and maintenance of the plants once they’re up and running.

Component/Equipment Manufacturers – The Suppliers Then there are the component manufacturers. These companies supply crucial parts like membranes, bar screens, sludge digesters, pumps, and various filtration equipment. Some of these manufacturers also dabble in EPC activities, adding another layer to their business.

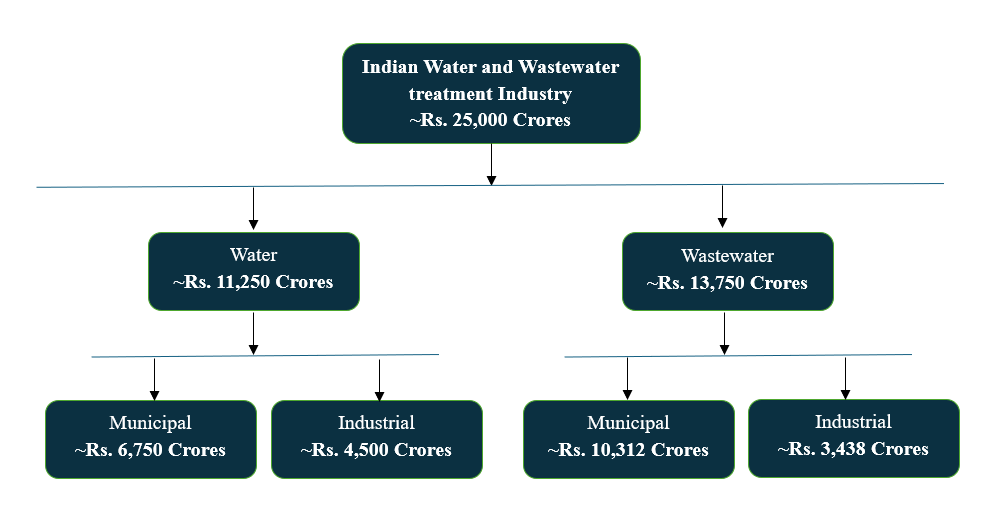

The Indian Water and Wastewater Industry Market size

Source: Frost and Suillvan, Niveshaay Research.

Do note, for the estimation of the market size of the industry we have only considered the EPC of the plants and the equipment. EPC for Pumping system and pipe laying works haven’t been included in this, which itself is a big opportunity under water.

Why water and wastewater Industry India

1. Repercussions of not treating wastewater are high

Ever wondered what would happen if we just let wastewater be? Spoiler alert: it’s disastrous. Here’s a quick look at the major fallout of not treating our wastewater:

Water scarcity – Right now, about 7% of India’s population don’t have access to safe drinking water. On top of that, around 57% lack proper household sanitation. The water we do have is also getting scarcer. In 2021, the average annual water availability per person was 1486 cubic meters. By 2031, it’s expected to drop to 1367 cubic meters. FYI, if this number falls below 1700 cubic meters, we’re officially in “water-stressed” territory, and below 1000 cubic meters, we hit “water scarcity.”

Economic impact – Dirty water isn’t just gross; it’s expensive. Water pollution and related diseases put a huge strain on the economy. With 70% of India’s surface water contaminated and many people lacking safe drinking water, water-borne diseases are common and cost around USD 600 million annually.

Regulatory requirements – As per regulations, industrial units are required to install effluent treatment plants (ETPs) and treat their effluents to comply with stipulated environmental standards before discharging into rivers and other water bodies. However, many industries still do not treat their water before discharging it. In response, the government has begun taking strict action against those who release untreated water.

So, it’s clear: not treating and reusing wastewater has serious consequences. Whether you look at it from an environmental, economic, social, or regulatory angle, treating wastewater is crucial.

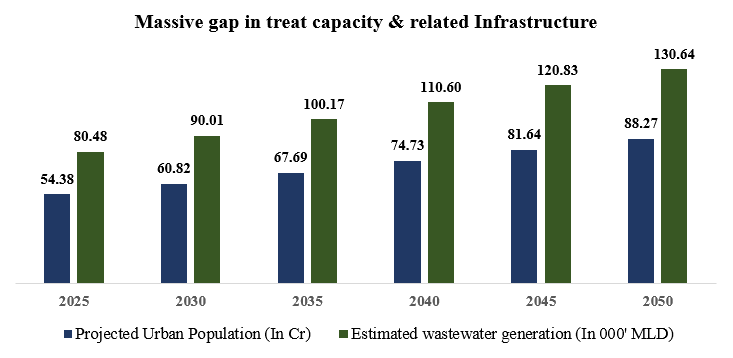

2. Massive gap in treat capacity and related infrastructure.

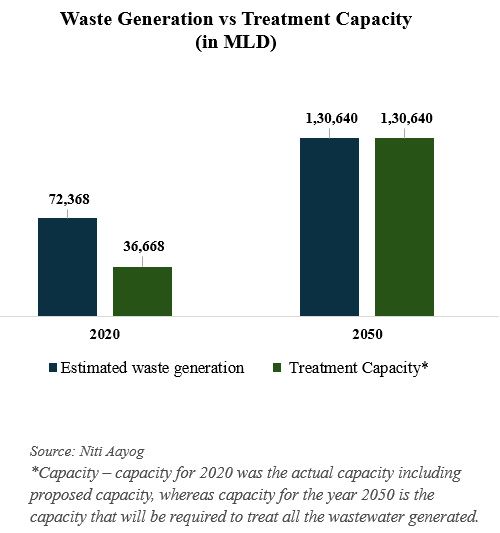

The Central Pollution Control Board (CPCB) reported that in 2020-21, rural areas in India generated about 39,600 MLD (million liters of wastewater per day), while urban areas produced a whopping 72,368 MLD. With the population growing and more people moving to cities, this amount of waste is expected to nearly double by 2050.

In 2020-21, urban areas in India generated 72,368 MLD of wastewater, but the operational treatment capacity was only 26,869 MLD, leaving a massive 63% undercapacity. Shockingly, just 28% of the total wastewater was treated, with the remaining 72% released untreated into water bodies. Even worse, only 12,200 MLD of the treated wastewater met the standards set by the Pollution Control Boards (PCBs/PCCs).

To keep up with the estimated future wastewater generation of 130,639 MLD, India needs to add 3,132 MLD of treatment capacity every year.

Wastewater treatment in India is just getting started but reusing (at a very nascent stage) that water is crucial for optimizing our resources. To give you an idea, in 2020-21, India produced about 72,368 million liters of wastewater daily. If all that water was treated and reused for irrigation, it could have covered around 3.2 million hectares of farmland. That’s about 22 times the size of Delhi! Just imagine the possibilities.

Also, besides sewage treatment plants, only about 30-35% of tier 1 cities have a good sewage network. It’s even worse in tier 2 and tier 3 cities. On top of that, around 13-14% of the households targeted by the Jal Jeevan Mission (JJM) still don’t have a tap water connection.

So, it’s pretty clear that India still has a long way to go when it comes to having proper water infrastructure. This is super important for conserving water and reusing it effectively.

3. Government driving the investments.

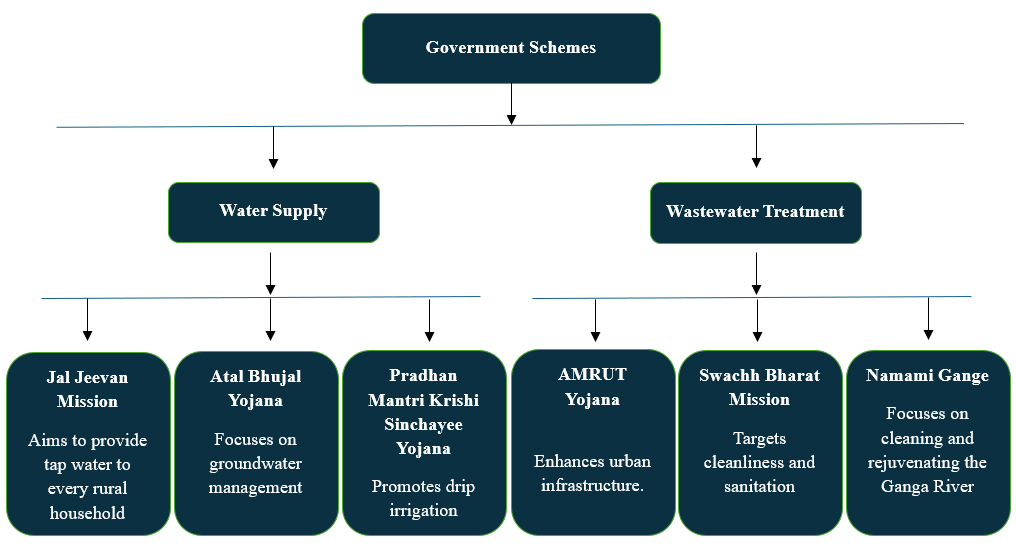

It’s the various government policies that are driving investments in water and wastewater. The Indian government has been emphasizing the importance of water and has rolled out several schemes for water conservation, treatment, and availability.

Here are six major schemes focused on water supply and wastewater treatment, have you heard of any of these schemes?

According to our estimate and understanding, if the government were to complete what they have envisaged under the above 4 schemes (excluding Atal bhujal yogna & Pradhan Mantri Krishi Sinchai Yogjana) we are expecting an investment of almost Rs. 50,000 – Rs. 60,000 Crores in the next 2-3 years. This project includes work related to sewerage network, water supply networks, Sewage treatment plant and water treatment plants.

4. Stricter CPBC Rules Fuel Growth

Industrial growth and tougher regulations from the CPCB and NGT (National Green Tribunal) are ramping up the need for industrial effluent treatment plants. According to the Environment (Protection) Act, 1986, and the Water (Prevention & Control of Pollution) Act, 1974, industries and local bodies must set up ETPs, CETPs, and STPs to treat their waste before releasing it. The CPCB, SPCBs, and PCCs keep an eye on this and dish out penalties for non-compliance.

Since the NGT’s 2018 order, things have improved. Out of 2,859 heavily polluting industries, 2,197 are up and running, with 2,059 meeting the standards, while 138 are still lagging. Those that don’t comply face show-cause notices and even shutdown orders. So, with stricter rules and booming industrialization, the demand for wastewater treatment plants is definitely on the rise.

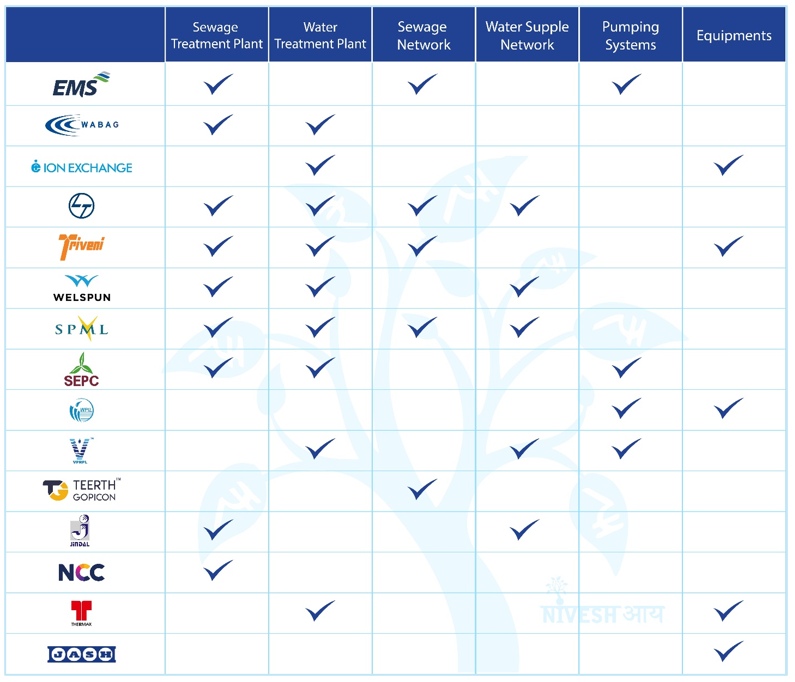

Companies engaged across the value chain are given below: –

Conclusion: –

So, it’s quite evident that India still has a long way to go in terms of developing proper water infrastructure. This is crucial not just for conserving water, but also for reusing it efficiently. Without the right infrastructure in place, we miss out on huge opportunities to optimize our water resources. Investing in better wastewater treatment and reuse systems can make a massive difference, ensuring we use our water wisely and sustainably for the future.

After all, taking care of our water resources is ultimately for our own benefit. By conserving and reusing water effectively, we secure a better future for ourselves and the generations to come. It’s time to step up and prioritize the health of our water systems.

In the coming decades, global energy demand is expected to significantly increase due to rising population, industrial growth, technological advancements, and increased data center usage. This growing demand, coupled with challenges such as climate change, greenhouse gas emissions, and escalating pollution, underscores the need for renewable energy solutions. Among these solutions, Solar energy has been adopted in a meaningful way leveraging its scalability, decreasing costs, and long-term sustainability.

As the power sector undergoes this rapid transition towards cleaner and greener sources of energy, it has presented investors with interesting investment opportunities. We, at Niveshaay, are particularly bullish on this trend. As part of our scuttlebutt investing approach and to gain firsthand insights into the global solar industry, we recently attended the ‘SNEC 17th (2024) International PV Power Expo’ in Shanghai, China.

Current Industry Trend

Our visit to the SNEC Expo provided invaluable insights into the industry’s current landscape and emerging trends. One of the important observations was the industry-wide adoption of TOPCon technology in China. This technology boasts superior efficiency compared to the previously dominant PERC technology, and Chinese manufacturers are leading the charge with a whopping 700 GW TOPCon cell capacity. Due to cost advantages and better pricing of TOPCon cells as compared to PERC cells, most of the companies in China are strategically shifting to TOPCon and phasing out their PERC facilities. Though HJT has better efficiency than TOPCon, it is a costlier technology and the manufacturers are facing some issues in manufacturing HJT cells. China currently has 100 GW HJT cell capacity.

Dominant Position of China

The key factor behind China’s dominant position in the solar industry is the robust government support. This enables them to establish massive production capacities (ranging from 10 to 20 GW) within a remarkably short timeframe of 12-18 months. This rapid scaling is fuelled by a confluence of government incentives, including free land for five years, attractive local subsidies, tax exemptions for initial years, and access to critical utilities like power and water at subsidised rates. Additionally, their fully automated production lines enable them to scale and run efficient operations through adequate human oversight.

India’s Rise: Matching Ambition with Action

Despite dominance of China in the global solar industry, the Indian government has been very proactive in building the necessary infrastructure for a swift energy transition. Initiatives like ALMM (Approved List of Models and Manufacturers) and DCR (Domestic Content Requirement) have significantly benefitted Indian solar manufacturers, empowering them to cater more effectively to domestic demand and restrict competition from Chinese players. The implementation of ALMM has also led to a decline in module imports from China. A growing trend within the Indian solar sector is the intention to push for backward integration, a strategy that allows manufacturers to exert greater control over their supply chains. This move is expected to be further bolstered by the government’s PLI (Production Linked Incentive) scheme.

A Golden Opportunity for Indian Solar Players

MonoPERC technology is expected to stay relevant for Indian markets for implementation under DCR and ALMM requirements. TOPCon is still in its initial phases and may take time to ramp up as only few large players in India are making TOPCon modules in limited quantity. Manufacturers who are able to transition to TOPCon technology in the near future would stand to gain a significant competitive edge. By embracing TOPCon early, they can capitalize on its efficiency benefits and establish themselves as strong contenders.

There are also circumventing and dumping allegations against few Southeast Asian countries in US markets which will create demand-supply gap. Other export markets are also expected to restrict entry of Chinese vendors due to significant overcapacity. Indian manufacturers stand to benefit due to this unique situation in the export markets.

Challenges and the Road Ahead: Building a Resilient Domestic Ecosystem

One of the key challenges on the path to self-sufficiency lies in establishing cell manufacturing facilities in India. Currently, Indian cell manufacturers are facing hurdles in securing essential utilities infrastructure and navigating restrictions on the entry of Chinese engineers to India. Companies that can commence facilities without much delay will have a significant advantage due to demand generated from DCR scheme. However, China’s current overcapacity has created a unique advantage for Indian companies. Chinese equipment manufacturers who are facing constrains in domestic (China) market, are now wooing Indian companies with attractive turnkey solutions at favourable terms.

Summary

The technology in solar is changing fast with limited time available for the manufacturer to recover their investments along with decent profitability while parallelly shifting to latest technology. Due to this complicated and capital-intensive nature of the industry, it may be difficult for a new player with limited history of execution to enter the business and be successful in long run. The energy storage business has also started gaining traction in China due to falling prices of the batteries. Once available at full scale and at a reasonable cost, it will experience significant growth in the Indian market.

The SNEC Expo served as a powerful testament to the dynamism of the global solar industry. The future of solar energy is undeniably bright, and India is well-positioned to be a major player in this transformative journey. By staying informed about the latest technological advancements, government policies, and market trends, investors can make strategic decisions and capitalize on the immense potential of this rapidly evolving sector.

The election outcome has been both remarkable and unexpected. The National Democratic Alliance (NDA) has returned for a third term forming a coalition government. There should not be any crucial impact on the policy frameworks as previous ministers have retained major ministries, ensuring the continuity of previously announced policies.

Historical Context: Government Capex and Economic Impact

Historically, the size and influence of government capex on the economy were substantial, particularly in the 1980s when public spending played a critical role in economic growth. At that time, continuity in government policies was crucial for sustaining economic momentum.

Typically, government capex drives initial growth, which is then followed by private investment. As government policies have already set the foundation, it’s time for private capex to take the lead, indicating a reduced dependency on government spending.

In India, the bull market persisted in 2004 despite a change in government and the formation of a coalition government, fuelled by the continuation of key economic policies and major private capex, resulting in a substantial market rally from 2004 to 2007.

The data mentioned below suggests that irrespective of government actions or changes, portfolio returns will ultimately reflect long-term earnings growth. Therefore, as investors, it’s crucial to concentrate on sectors where corporate earnings growth is expected to be robust.

Government

NIFTY EPS CAGR

NIFTY Return CAGR

UPA 1&2 (2004-2014)

12%

14%

NDA 1&2 (2014-2024)

10%

10%

Sustained Continued Growth Expected for Key Industries

The last two terms of the BJP-led government have seen a huge budgeted capital expenditure for Infrastructure, Railways, Defence, and many more, where we have already made investment allocations to capitalize on the anticipated growth opportunities.

In addition to the global momentum towards energy transition, investments in the whole value chain have paved the way for significant growth. Concurrently, India’s textile industry stands to benefit from the ‘China Plus One’ strategy and supply chain consolidation trends. The growth in this sector not only supports these strategies but also leads to significant employment generation in the country. Moreover, in electronics manufacturing, import substitution has strengthened Indian companies due to cost efficiencies, reduced lead times, and enhanced quality, fostering both domestic preference and increased export opportunities.

Moving forward, we also anticipate some measures towards populist measures aimed at rural development.

According to our observations, the current government’s approach focuses on long-term improvements in rural economies through infrastructure development, such as housing, electrification, and essential facilities, rather than short-term freebies. This strategy aims to provide sustainable economic upliftment.

Moreover, we believe that nurturing a thriving manufacturing sector will result in higher wages, particularly benefiting the bottom of the pyramid. This approach could potentially offer a sustainable solution for rural economic growth over the next decades. Emphasizing investments in manufacturing rather than short-term incentives ensures long-term growth supported by increased earnings and economic stability.

Strategy: Balancing Reactivity and Long-Term Focus

In the face of current market conditions, it is prudent to adopt a reactive rather than predictive investment strategy. Observing the formation of the new government and the distribution of ministries will provide critical insights into the future direction of economic policy. This wait-and-watch approach will allow investors to make informed decisions based on emerging data.

Furthermore, with minimal disruption in the distribution of ministries, we have been actively tracking and investing in the high-growth sectors supported by favorable policies. We anticipate continuity in policy allocation while remaining cautious about any announcements or shifts that could impact our portfolio or present future investment opportunities.

In conclusion, despite current anomalies, we remain focused on the bigger picture, confident that India’s long-term growth trajectory is secure and short term challenges will not have a lasting impact. The manufacturing sector is poised to be a long-term growth driver and energy transition initiatives are expected to remain a focus, aligning with global trends.

Disclaimer:

Niveshaay is a SEBI Registered (SEBI Registration No. INA000017541) Investment Advisory Firm.Our research expresses our opinions which are based on available public information, field research, inferences, and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained here is accurate and reliable and has been obtained from public sources, which we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent investment advice or a recommendation or a solicitation to buy any securities.

In part 1 of our blog, we discussed how the aviation industry appears to be headed towards strong growth. Amongst all, we also discussed how Interglobe Aviation Limited (“Indigo”) appears to be set to enjoy benefits from this industry wide tailwinds.

This part of the blog delves deeper into the operational metrics of Indigo which is India’s largest airline and one of the world’s leading low-cost carriers with a dominant position in the Indian airspace (60%+ domestic market share and 17%+ international market share) with an exemplary management team. It offers passengers a simple brand promise of providing “low fares, on-time flights, and a courteous and hassle-free service”.

The company has a mega fleet of 360+ aircrafts with an average age of 4-4.6 years, almost half the average age of Air India and Spicejet. Further, it is undertaking aggressive capacity expansion by almost doubling its aircraft fleet in the next 5 years.

Some of the key operational excellencies of Indigo include:

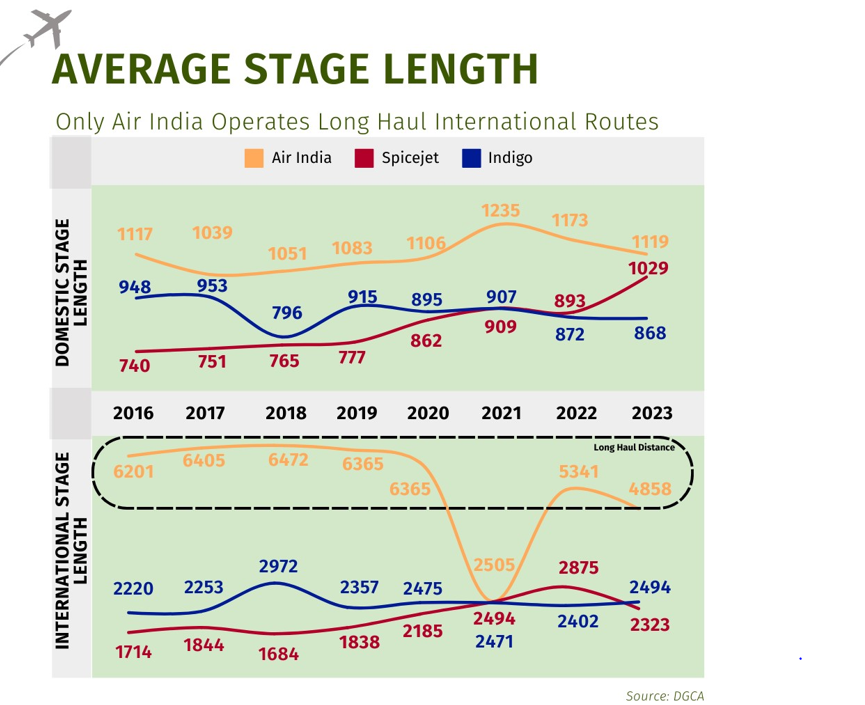

1. Favorable shift in the Average Stage Length:

The lower the average stage length, the more cost-effective the airline is for short-haul flight operations (<4 hours flying distance). A lower average stage length also means a greater number of departures. For long-haul operations (>6 hours flying distance), higher stage length usually leads to cost savings which lead to improved profitability.

Over the last 10 years, Indigo’s domestic average Stage Length (Average Distance flown) has reduced from 947.5 Km in 2016 to 868.4 km in 2023. During the same period, the international average stage length increased from 2,219.8 km to 2,493.5 km. With the introduction of long-haul flights, the international average stage length is expected to increase further in the coming years.

Therefore, since the base minimum fare and functional constant is always received by the airline and the costs are limited, the low-cost carriers are able to earn higher yields per km flown on destinations that fall in the range of short to medium distances as compared to medium and longer distances. Thus, although the number of departures is higher, with extremely efficient operations, Indigo is able to earn good margins with good traffic volumes on these low to medium-faring routes.

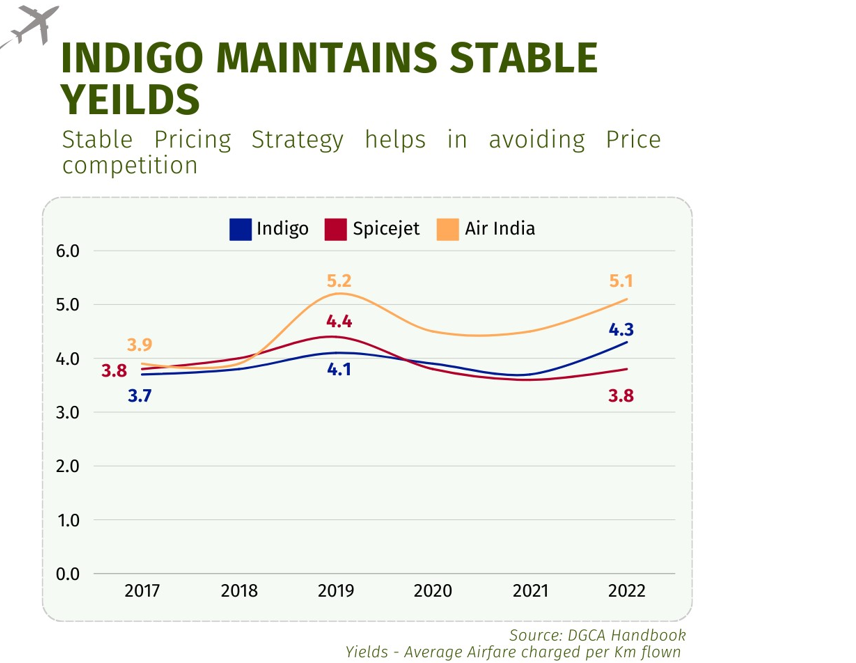

2. Stable Yield Strategy:

While Air India and Spicejet have struggled with volatile Yield Per Passenger km, i.e. fare charged to a customer per km flown, Indigo has maintained a stable yield range over the years. It has kept its pricing strategy very clear – “Affordable”.

Although sounds simple, in light of the aviation industry it is very difficult to maintain stable fares. This industry has always been troubled with pricing wars. However, Indigo’s strategy has been very clear – avoid price wars. Indigo maintains a fair airfare which is slightly higher than its competitors sufficient enough to pose to customers as if they are getting Indigo at almost similar fares (or at a very nominal premium).

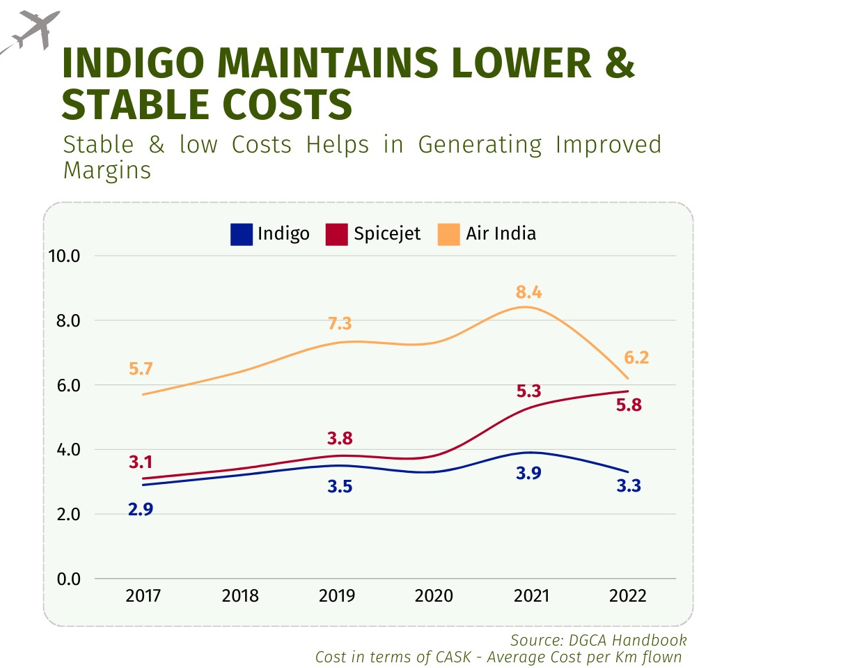

3. Operational Excellence:

Strong management acumen with years of experience in operating airlines, strong business fundamentals and tactics like sale and leaseback model, maintaining lower aircraft weights, maintaining a passenger load factor at 80-85% levels, etc. leads to improved cost efficiency.

Whilst other players have struggled with maintaining their Cost per Available kms, Indigo has maintained a clear strategy to keep its operations efficient. The RASK-CASK spread has remained healthy over the years at Rs. 0.30-0.40 per passenger-km.

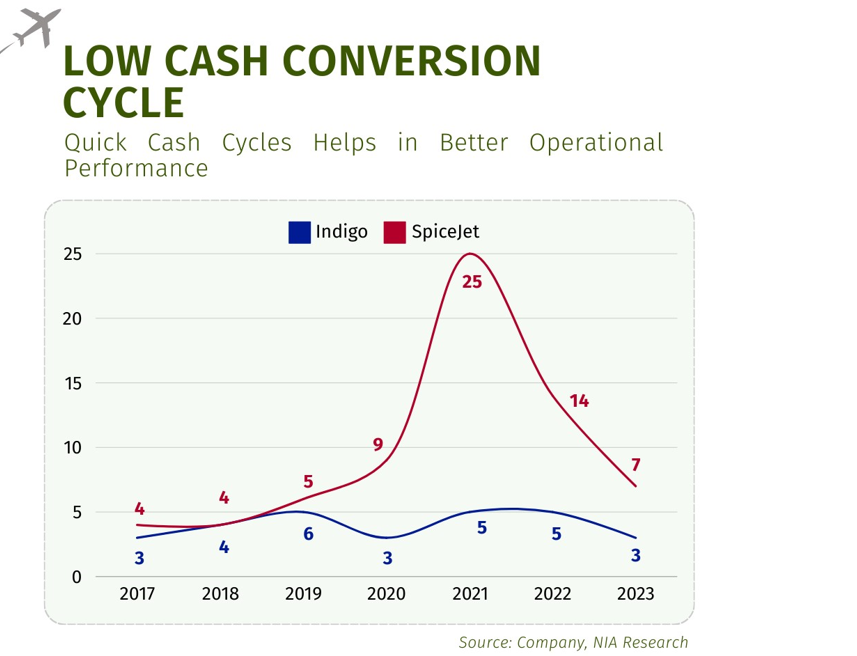

4. Efficient cash management:

Indigo has managed to maintain a stable cash conversion cycle with the lowest in the industry conversion cycle of 3 days. Further, with a cash and cash equivalents balance of over Rs. 13,063 Crores as of 30 September 2023, the company appears well-prepared for capacity additions. This liquidity also aids in better credit ratings and therefore, lower lease finance costs.

All these strong fundamental metrics combined with tailwinds for the industry should lead to multiple benefits for the pioneer of the Indian aviation space, Indigo.

Whilst these factors do indicate a strong road ahead, various factors can impact the operations of the entity, such as weather-based disturbances, flight delays, operational issues, higher costs due to the grounding of aircraft, etc.

All things factored in, despite potential industry challenges, Indigo’s robust operational metrics, strategic international expansion, stable yield strategy, efficient management, and strong cash position, position it well for growth.

Q1. Which Niveshaay smallcase should we invest in?

The choice of smallcase for investment depends on your investment horizon, risk tolerance, and financial goals. Each smallcase is designed with a specific investment objective and strategy in mind. It’s essential to evaluate your own investment horizon and risk appetite before deciding which smallcase aligns best with your financial objectives.

We offer six smallcases and you can learn more about them here. To start with the investing journey, one can consider strategy-based portfolios such as Mid and Small Cap Focused Portfolio Fundamental, Trends Trilogy Fundamental, which are our diversified portfolios and cater to multiple sectors. You may also explore our thematic portfolios, such as Green Energy Theme, Niveshaay Consumer Trends Portfolio Theme, Make in India Theme. Recently we have also launched our Niveshaay IPO Basket Fundamental which provides a unique opportunity to invest early in companies set to become future industry leaders.

Q2. Is there any minimum investment requirement for your portfolio?

The minimum investment amount is calculated based on the underlying stocks and their weights, based on the current market price. Once this amount is invested, the SIP amount will be fixed.

The SIP amount is calculated based on your Minimum Investment Amount (MIA). If the investment amount is less than INR 12,000, then the minimum SIP amount equals the investment amount. If the investment amount is more than INR 12,000, then the minimum SIP amount is twice the value of the highest-valued stock rounded up to the next 1000.

To maintain an optimal expense ratio, we suggest a minimum investment of Rs. 4–5 lakhs in our Smallcase. Click here to learn more about achieving the ideal expense ratio.

Q3. How should one deploy funds?

We recommend investing in a SIP (Systematic Investment Plan), as it enables accumulating cash gradually for lump-sum investments when needed.

Q4. What duration is optimal for investing?

At Niveshaay, our investment strategy is oriented towards the long term, with focus on sectors and industries poised for high growth in terms of revenue, earnings, and cash flow. This could be due to industry-wide healthy tailwinds or the turnaround of a particular company. Given the inherent volatility of markets, we always recommend keeping an investment horizon of 3–5 years to reap the maximum benefits.

Q5. How much return can we expect?

We advise investors to uphold long-term investments to maximize returns, particularly given the market’s volatility. It’s important to note that, in accordance with SEBI regulations, we refrain from making any commitments or assurances of guaranty or risk-free returns to investors.

Q6. How frequently does rebalancing happen?

Our dedicated research team consistently monitors the portfolio, tracking each company and its developments. We swiftly rebalance whenever there are significant shifts in fundamentals or market sentiment or when new company-specific opportunities arise. Furthermore, we typically rebalance after the quarterly results season. We’ll keep you informed via email and WhatsApp whenever a rebalancing occurs.

Q7. How do I execute a rebalance?

Steps to apply rebalance

From your Investments page, click “Rebalance” where available.

Review the update or make changes by clicking on “Customize”

Confirm the update and place orders.

Please note:

Your smallcase will be rebalanced only when you confirm and place the order; it will not be done automatically.

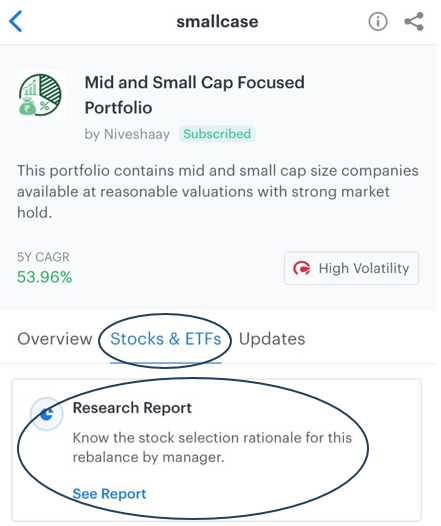

Q8. Where can we find the rationale behind the rebalance?

We offer our research analysis in the rebalance rationale report.

Steps to find the rebalance rationale report:

Login to your smallcase account.

Click on Discover.

Search for the Niveshaay smallcase that you have subscribed to.

Click on Stocks & ETFs.

Scroll down and click on “See Report” to read the rationale behind the rebalance.

Q9. How should one respond when stocks reach the upper or lower circuits?

You might have noticed this error during rebalancing. This situation arises when stocks get stuck in circuits, either upper or lower, preventing buying or selling until they exit circuits. When stocks hit the upper circuit, it indicates a shortage of sellers, while hitting the lower circuit implies a shortage of buyers. This halts trading, potentially causing the rebalance order to not execute. In such cases, we request not to archive the order. Instead, once stock exits the circuit, we kindly request that you go to your Smallcase account and execute a ‘REPAIR ORDER’.

If you mistakenly archived the order, you can reverse it by emailing support@smallcase.com. If you executed the order directly through your broker, please email support@smallcase.com and smallcase@niveshaay.com, providing the stock’s name, price, quantity, and date of transaction from your registered email ID to facilitate order reconciliation.

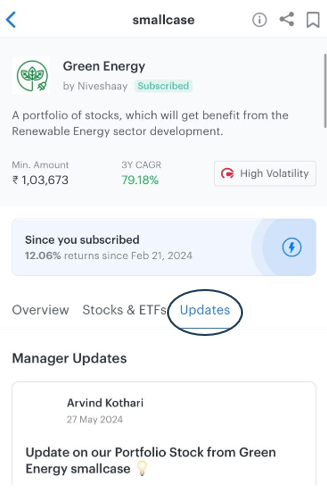

Q10. How do I access the manager updates sent by Niveshaay?

To explore the manager update section, please navigate to the Smallcase application and follow these steps:

Log in to the Smallcase application.

Search for Niveshaay Portfolio

Click on the Updates section.

Q11. What are LiquidBees/Liquidcase ?

LiquidBees, an exchange-traded fund (ETF), functions as a cash equivalent within smallcase, a portfolio where full fund deployment is required. This strategy allows for maintaining liquidity, particularly during times when market valuations are high and holding cash enables quick liquidation as needed, facilitating taking positions in equities.

Q12. The stocks listed in my broker account differ from those in my Smallcase App.

This occurs when transactions are conducted directly through a broker account, resulting in discrepancies in holdings and returns. You can easily reconcile your holdings by simply dropping us a mail at support@smallcase.com and smallcase@niveshaay.com, providing the stock’s name, price, quantity, and date of transaction from your registered email ID.

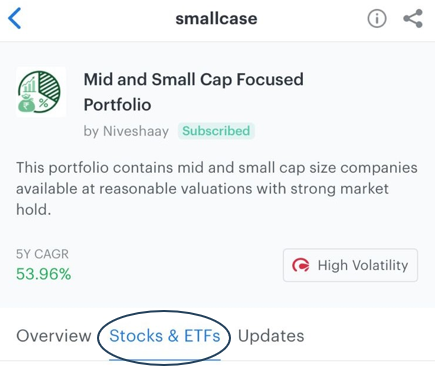

Q13. Where can we find the original composition of smallcase?

You can find the original composition by following these steps:

Log in to your smallcase app.

Navigate to the ‘Discover’ section and search your subscribed Niveshaay smallcase.

Click on “Stocks and ETFs” to explore the detailed breakdown of the original portfolio composition.

Q14. What are your charges above subscription fees?

We prioritize your trust and satisfaction and do not levy any extra charges beyond our subscription fees. However, it’s essential to acknowledge that, apart from subscription fees, there are transaction charges imposed by smallcase, along with brokerage and STT, applicable each time you trade shares through your broker. Nevertheless, the primary expense remains the subscription fees, with these supplementary charges kept minimal on the platform to enhance your investment journey.

Q15. Can we add or remove stocks from Smallcase?

You have complete control over adding or removing stocks at any time.

Select a smallcase from your Investments page and click on “Manage”

Change the quantities of your constituents OR add OR remove a stock.

Once done, review the changes and place your order.

Please Note: If you manage smallcase then it will deviate from the original idea, and we do not recommend doing the same. However, if you still wish to continue, you will continue to receive rebalance updates, and your SIP (if active) will also be updated accordingly.

Q16. What is an expense ratio, and how much should be the ideal expense ratio?

The expense ratio is the ratio of the subscription fee to your total investment value.

Expense Ratio = Annual Subscription Fee / Total Planned Investment by Year

For example, if the expense ratio is 20%, it means you’re paying 20% of your total investment value as a subscription fee. That means you need to earn a minimum of 20% returns just to break even with your investment value.

It’s advisable to keep your expense ratio minimal for any investment. We recommend aiming for an expense ratio between 2–3% for Niveshaay smallcase. Considering our subscription fees, we suggest investing a minimum amount of Rs. 4–5 lakhs to maintain the desired ratio.

Note: Subscription fees are a major expense, and all other expenses are very minimal compared to others.

It’s that time of the year when we put our thoughts to perspective, reflect on our past successes and what didn’t work for us, evaluate areas for improvement, and convene with our team to set goals and agendas for the upcoming year. First and foremost, we’re pleased that we’ve concluded this eventful year on a positive note, with favorable returns attributed to our continued investment in previously identified opportunities over the past few years, as well as discovering new prospects within the sectors where we’ve already invested, and perhaps a bit of good luck as well. Our investments in high-growth sectors like Energy Transition, Capital Goods, and Manufacturing, particularly in the early stages, turned out to be advantageous this year.

The Indian equity markets sustained their upward trend, surpassing many global counterparts, largely due to favourable government policies reigniting investment activity. Our decision to invest a lump sum during the February-March-23 volatility proved beneficial, contributing to generating slightly higher returns throughout the year. Additionally, we’ve gleaned some important lessons this year. Firstly, the value of time spent in the market and prior thorough research in specific sectors greatly facilitates swift decision-making. Moreover, we’ve realized that valuation alone cannot serve as the sole criterion when considering investments in companies or businesses. The predictability of earnings growth, the competitive landscape, and the sustainability of business trends or tailwinds are equally critical factors that were also taken into account when we were making an investment decision.

At the outset, we launched our flagship smallcase, ‘Mid and Small Cap,’ which comprises a diversified portfolio that allocates across major sectors. Analysing, the tailwinds and expected accelerated adoption in the renewable sector, we launched the ‘Green Energy’ portfolio in 2021. The sector has garnered a lot of attention due to the government’s commitment to sustainability. It’s now when we realise, our portfolios were rightly placed in the journey to take advantage of the potential growth. Further, we believed that the supply chain re-arrangement post the pandemic coupled with government-led favorable policies aimed at reigniting the investment cycle in the country, promoting import substitution, and intensifying focus on exports, would contribute to the growth of Indian manufacturing.

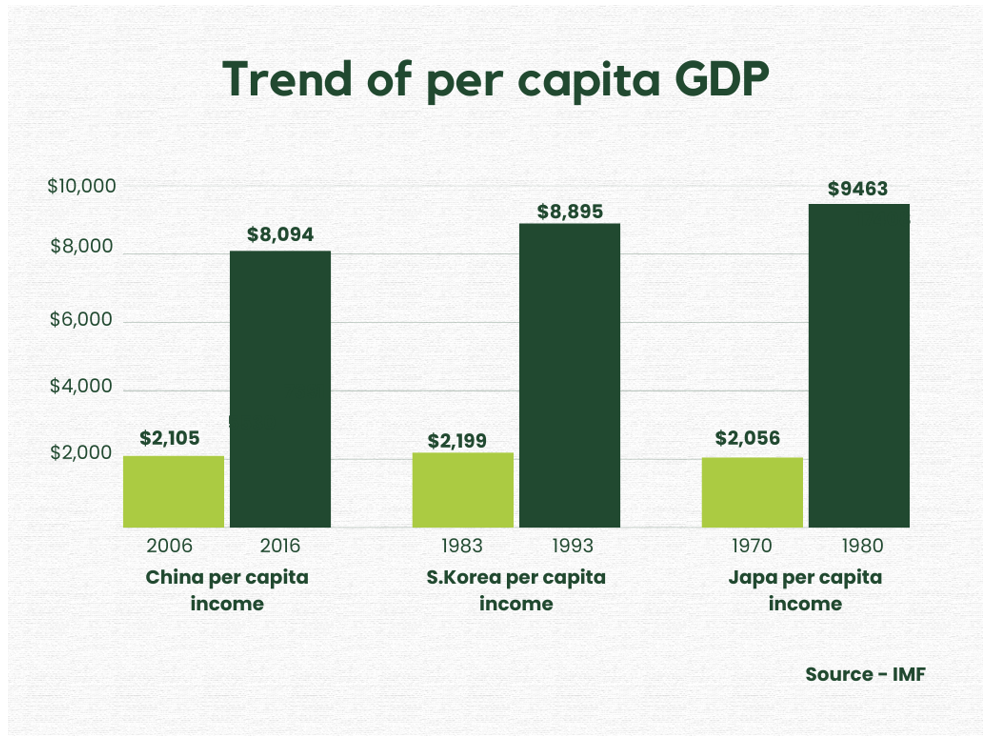

This conviction prompted us to introduce the ‘China Plus One’ smallcase. When these initiatives started to translate in numbers, we believed that the higher investment in India’s manufacturing sector is expected to have a ripple effect by boosting consumption. Government policies have created significant growth opportunities, resulting in per capita GDP surpassing $2000. Historically, countries like China, Japan, and South Korea experienced a surge in consumption spending upon reaching this income level. In the last few years, a rise in consumption has been observed due to increasing disposable income and changing habits. We believe it’s the beginning of a new consumption story in India where premiumization will take a substantial share. With these thoughts in mind, we launched another portfolio, ‘Consumer Trends’ during Diwali, focused on discretionary consumption and premiumization. Lastly, our ‘Trends Trilogy’ smallcase is all about playing the three trends: Business, Financial and Technical Trends in a concentrated manner.

Commencing with the power sector, which is witnessing significant global investments, primarily due to the swift transition towards renewable energy sources. This surge in power generation prompts the growth of transmission and distribution companies. We integrated this theme into our portfolio by allocating investments in Transformers & Rectifiers (India), a prominent power transformer manufacturer and Skipper, the largest power transmission tower manufacturer in India. The ambitious target of achieving approximately 500 GW in renewable energy capacity by FY30, up from 179 GW in FY24, is anticipated to attract significant investments across the entire sector, encompassing generation, transmission, and distribution.

Supported by favourable policies and consistent government backing, India’s manufacturing and infrastructure real estate sector is witnessing a sectoral tailwind. We took exposure in this sector through Action Construction Equipment (ACE), dominating crane manufacturing with over 65% market share, and Sanghvi Movers, India’s largest crane rental company.

The ‘China Plus One’ strategy and the trend of supply re-arrangement present promising opportunities for India’s textile industry, a sentiment reaffirmed at the Bharat Tex expo. We maintain our optimism regarding this theme, and our early recognition of this sector and analysis of the value chain have enabled us to benefit either by investing in highly efficient garmenting companies or in growing home textile companies.

India has also undertaken similar government policies, such as supporting end-user industries through export tariffs and stimulating domestic demand via import substitution policies aimed at promoting indigenisation. For instance, these policies have strengthened India’s defence ecosystem, contributing to the nation’s self-reliance and economic growth. Defence exports increased from Rs. 10,746 crores in FY19 to Rs. 21,083 crores in FY24, and the target is to reach Rs. 35,000 crores by FY25. The import substitution in industries like the electronics manufacturing and food equipment industries has resulted in Indian companies being preferred over imported ones due to cost savings, reduced lead time, and good quality. According to Bloomberg, India’s electronics exports to the USA as a ratio of China’s increased from 2.51% in November 2021 to 7.65% in November 2023. In the UK, the share rose from 4.79% to 10% during the same period. From exporting zero mobile phones in 2014 to now becoming the 2nd largest exporter globally, electronic exports increased from $8.4 billion in FY19 to $23.6 billion in FY23.

Samsung and Foxconn, the manufacturer of Apple’s iPhone, are leading the charge in relocating their manufacturing operations to India. Supportive government policies incentivizing local production, combined with favourable production factors, are positioning India as an appealing destination for multinational corporations (MNCs) aiming to establish manufacturing facilities. Recently, Tesla has also signalled its intent to establish a manufacturing unit in India. This trend not only enhances the global competitiveness of MNCs but also encourages other companies to establish plants in India while fostering the growth of the component ecosystem and promoting increased domestic sourcing within the country.

As we observe manufacturing sector thriving, it naturally elevates the per capita income, consequently fuelling an increase in discretionary spending. This trend is expected to significantly boost consumer spending in India. Within the consumer discretionary space, the premiumization trend is gaining momentum. India can rely on its own domestic demand to firepower its growth, specifically, private consumption (accounts 60% of its GDP) and investment spending. Staying invested in the theme can yield good results in the long term.

As much as our thesis played out, certain companies, such as Hindware Home Innovation Ltd. even booked losses due to underperformance relative to our expectations. Initially, we viewed it as a promising undervalued brand play on real estate, but subsequently exited when the numbers didn’t comply with our investment thesis due to delayed or subdued consumption in the affordable segment. In China Plus One and Trends Trilogy Smallcase, we believed IFGL refractories to be a good ancillary play on the rapidly growing Steel industry but booked losses as the performance of the company was not on par with our expectations, largely attributed to ongoing geopolitical issues in Europe. These challenges impacted the company’s sales volume, which we expect to persist in the upcoming quarters.

We have received tremendous support throughout, and our Smallcase family has now grown to 25,000+ active subscribers. We hosted regular Webinars and conducted Ask Me Anything (AMA) sessions to share valuable insights and opportunities to stay informed about the ever-evolving financial landscape. To engage more personally with our subscribers, we organized meet-and-greet gatherings in Mumbai and Bangalore, allowing us to connect with our audience. We’re excited to continue hosting similar events and look forward to visiting more cities in the future!

This year, we closed favourable deals in the private equity market, driven by our philosophy of having ‘skin in the game’ and investing in sectors exhibiting bullish trends. In the private sector, we look for opportunities where companies need growth capital and where IPOs are expected to come in the range of 6 months – 4 years. For instance, to name some:

We came across Waaree Energies Ltd. while exploring opportunities in the renewable sector. With a current capacity of 11 GW, it is India’s largest solar PV module manufacturing company. Considering it had only 2GW capacity in 2021, it has exponentially increased its capacity because of rising demand and a healthy order book. It has turned out to be an outperformer, with its valuation now more than triple since our investment in the second fund raise round. The company is now vertically integrating into cell manufacturing, which will further expand operating margins. A very good company to analyse the execution capabilities of any entrepreneur translating into tangible numerical results.

Similarly, we’ll continue to actively pursue investment opportunities in private markets, particularly in sectors such as manufacturing, power, renewables, and others.

While these sectors are experiencing huge tailwinds, and analysis of end-user industries’ capital expenditure plans reveals numerous promising opportunities across various sectors. But, the dilemma here these days is between the rich valuations and high expected earnings growth. Staying invested in the already identified stocks can turn out to be a good decision or invest in companies where earnings predictability is high and available at reasonable valuations.

We sincerely thank you for entrusting us with your wealth creation journey. Your confidence in us, particularly during volatile periods with a high churn in the portfolio is valued greatly. We remain committed to delivering exceptional service, as always.

The first two decades of this century were China’s, then this decade and beyond will be India’s. The consumption story in India is just unfolding.– Sanjiv Mehta, Former CEO and MD, HUL

India, boasting a population of 1.4 billion, has recently surpassed China to become the world’s most populous country. Beyond economic indicators, India’s demographic profile, characterised by a sizable youth population and an expanding middle class, underscores the nation’s growing consumer potential.

Headlines announcing India’s remarkable GDP growth of 7.6% have captured widespread attention, showcasing the country’s growing manufacturing prowess. Increased investment in India’s manufacturing sector is anticipated to have a ripple down effect, spurring consumption.

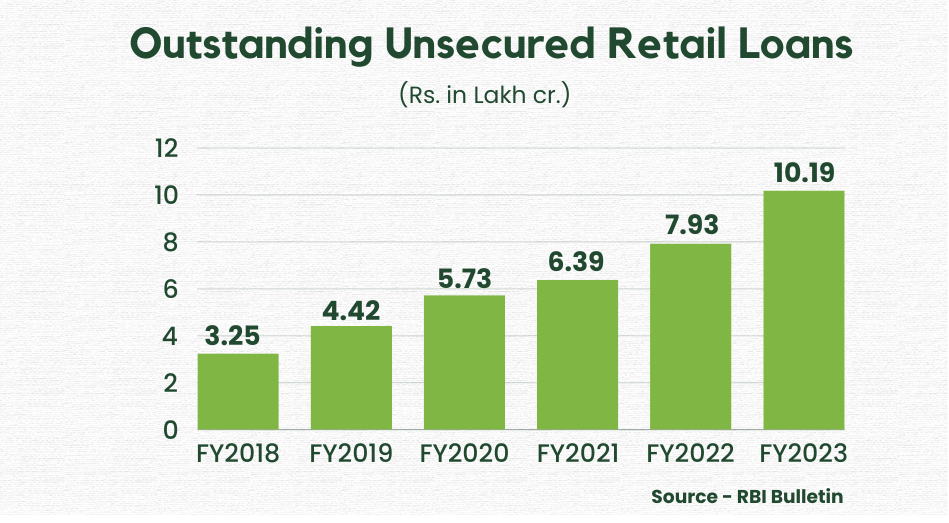

The surge in retail lending activity provides tangible evidence of increasing consumer demand. India’s credit boom has fuelled a resurgence in sectors such as luxury real estate, automotive industries, and high-end consumer goods, reflecting a robust appetite for discretionary spending.

Economists forecast that when per capita GDP exceeds $2,000, a notable transformation occurs where countries observe a consistent trend of increased consumption, particularly discretionary spending. A similar trend was observed in the United States in the 1950s/60s, Japan in the 1970s, South Korea in the 1980s, and China in the 2000s.

Guess what? India has crossed the crucial inflexion point where per capita GDP has exceeded $2500. This is the stage where consumption skyrockets and moves from spending on needs to indulging in wants. Moreover, the trend towards premiumization spurs an increase in demand for luxury and high-end products. According to Bain & Co., the luxury market in India could burgeon to $200 billion by 2030, marking a threefold increase from its current size.

Forecasts from S&P Global Market Intelligence indicate that India’s GDP could soar to an impressive $7.3 trillion by 2030. Such growth prospects are underpinned by escalating manufacturing activity, which is expected to translate into heightened consumer spending and stimulate economic growth.

This demographic dividend, combined with rising aspirations for an elevated lifestyle, drives demand across various sectors. Some of the interesting sectors that can benefit from this trend are:

Wealth Management Industry:

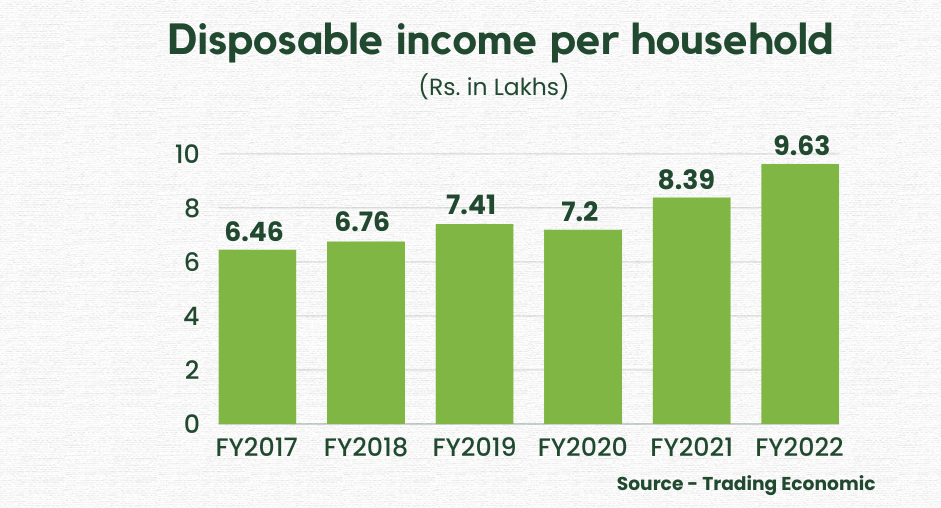

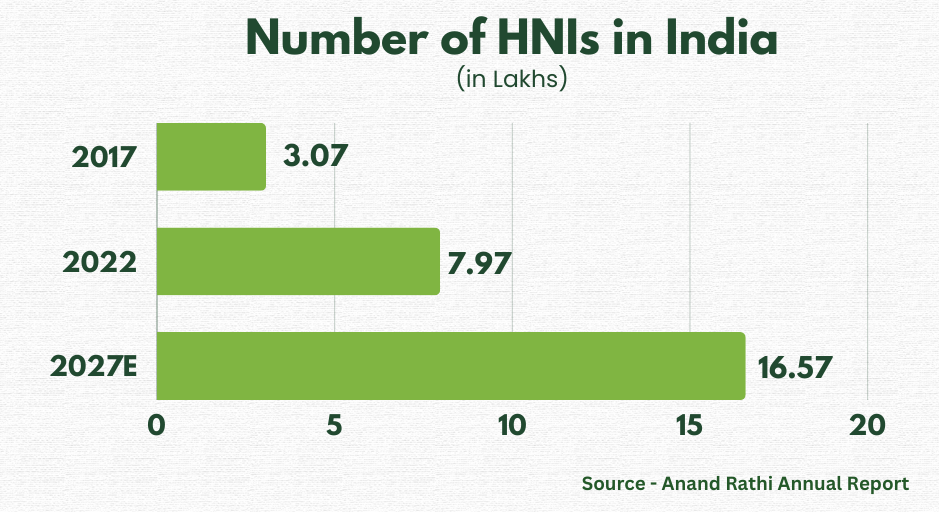

Savings remain at the heart of every Indian. The rising per capita income will robustly drive India’s consumption story, but not at the cost of investments. Overall, the rising per capita income will simultaneously promote a culture of responsible investment. This dual momentum is harnessed by the wealth management sector to help individuals maximize the potential of their savings and navigate the complexities of wealth accumulation in an evolving economic landscape. With the rising number of demat accounts and high-net-worth-individuals (HNIs) in India, the wealth management industry is poised for inevitable growth. As individuals accumulate wealth, there is a growing need for professional management of their assets.

Luxury Segment:

One of the segments that can benefit from this ongoing premiumization trend is the luxury segment. Indians are embracing premium products and luxury fashion, creating significant growth opportunities for the luxury segment in India.

Luxury watches

Luxury watches have always been a statement of elegance, status, and timeless style. The majority of luxury watches are Swiss watches. There has been a remarkable growth in the consumption of Swiss watches in India, reflecting an increasing preference for high-end watches among Indian consumers. The recently signed India-Europe free trade agreement will further boost the demand for Swiss watches as customs duties on imports will be removed over a period of 7 years.

Luxury Cars

Another segment benefiting from India’s economic growth is the luxury car segment, which has achieved its best-ever sales in the recently concluded financial year 2023-24. Carmakers attribute the increase in sales to a lifestyle shift post-Covid-19, with younger professionals opting for high-end cars. The booming market reflects an increasing appetite among Indian consumers for luxury and exclusivity. Also, considering the under penetration of luxury cars in India, where luxury car sales represent only 1% of total car sales, compared to higher percentages in countries like Japan (5%), Europe (18%), and China (17%), it’s evident that India’s luxury market holds immense potential for growth.

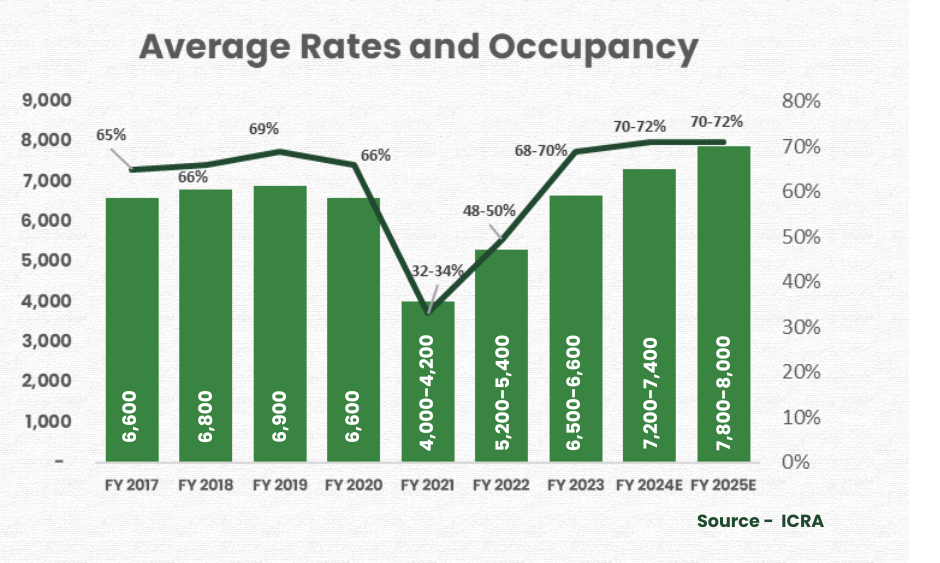

Hospitality sector

India’s hotel industry surged back to life, driven by a post-covid uptick in travel. Double-digit revenue growth was propelled by domestic leisure trips, meetings, incentives, conferences, and exhibition (MICE) events, the G20 Summit, and the return of business travellers. The added excitement of the ICC Cricket World Cup saw hotels fill up, and unorganized accommodations were abuzz.

Currently, India’s share in the total global MICE tourism (meetings, incentives, conferences, and exhibitions) is less than 1%, valued at USD 876.42 billion in 2022. This global market is projected to grow at a CAGR of 7.5% from 2023 to 2030. In India, it is expected to reach 2% within the next five years.

India is the fastest-growing aviation market in the world, with a projected growth in air trips of 7-8% between 2023 and 2030. To match the growing demand, Indian airlines have placed record orders for over 1,500 aircraft (discussed in the aviation blog).

All these indicators point to India emerging as a focal point for significant investment opportunities. The infusion of nearly $12.2 billion by foreign fund managers in the first half of 2023 alone underscores the growing interest in India’s economy. With private consumption contributing a substantial 60% to India’s GDP, it is clear that the nation’s consumer market is on track to become the world’s third-largest by 2027.

Moreover, India’s trajectory suggests that it will evolve into a $5 trillion consumption economy by 2031, with the middle class expected to drive 53% of incremental consumption. This underscores the enduring appeal of India’s consumption story, making it one of the most compelling long-term investment opportunities.