India’s retail industry is in the midst of an exciting transformation, and if you’ve been paying attention, you’ve probably noticed the growing shift towards value fashion – affordable yet stylish clothing options that cater to the masses. So, what’s driving this shift? How are brands like Zudio, V2 Retail, and Baazar Style tapping into this booming market? Let’s take a closer look at how these companies aren’t just following the trend—they’re shaping it.

Why This Phase Could Be a Boom for Consumption

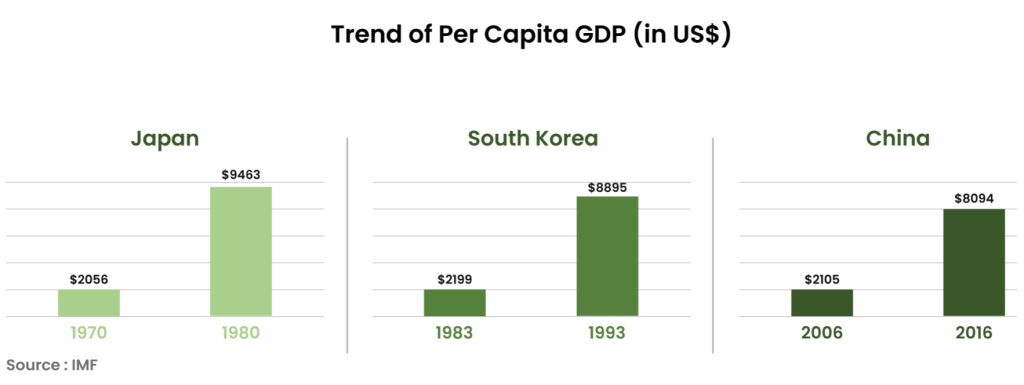

India is stepping into its most exciting consumption era yet. With our per capita GDP now at ~$2,500, we’ve crossed a key economic threshold that historically triggered exponential growth in countries like China, Japan, and South Korea. In each case, once GDP per capita moved beyond $2,000, their economies grew nearly 4x within a decade, driven primarily by consumption-led momentum. India appears to be on a similar trajectory.

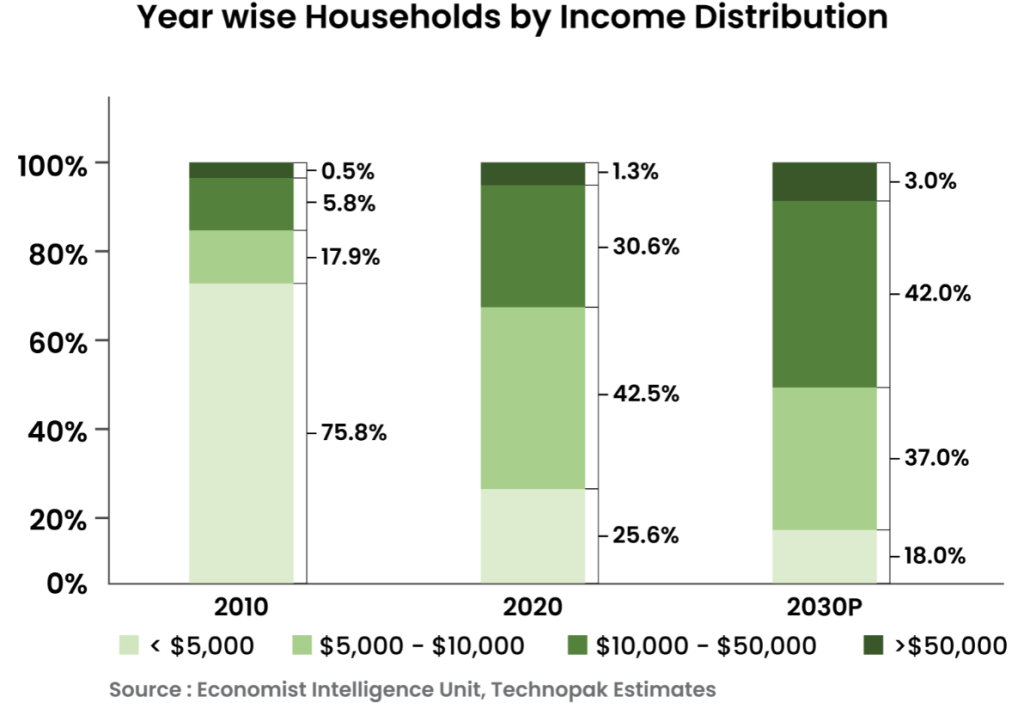

But GDP is just one part of the story. The more powerful shift is happening inside Indian households. In 2010, over 75% of households earned less than $5,000/year. Fast forward to 2030, and that number is projected to shrink dramatically to just 18%, while the share of households earning over $10,000 will surge to 45%. This isn’t just a demographic shift—it’s a fundamental change in how India will spend, save, and aspire.

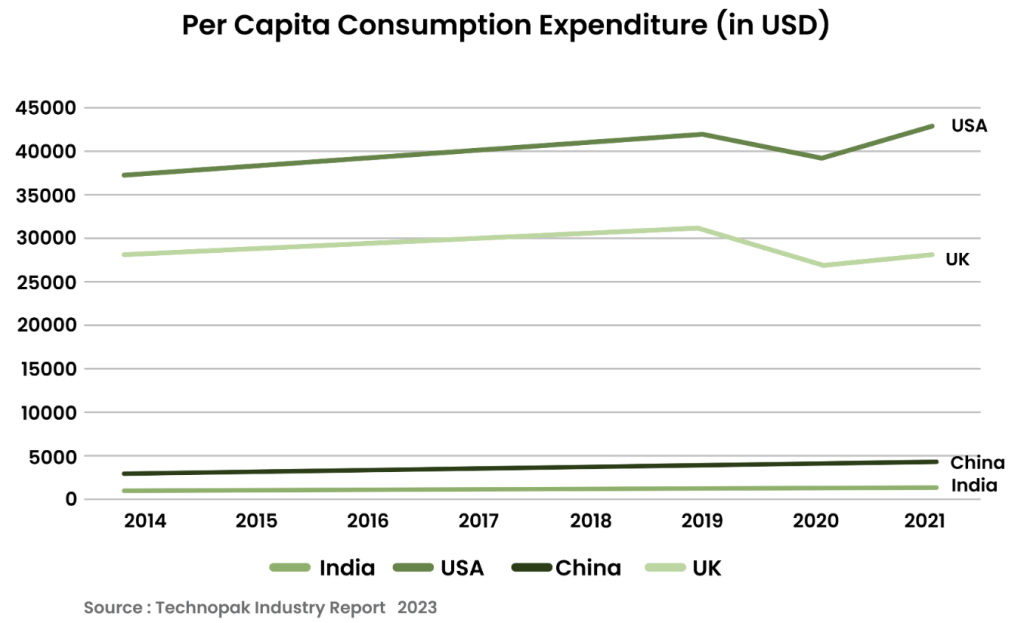

Another strong indicator of India’s consumption readiness is the sharp rise in per capita private consumption expenditure, which has grown from $715 in 2014 to $1,287 in 2021—an impressive 80%+ increase in just seven years. While this figure is still much lower compared to developed economies, it highlights a strong behavioural shift: Indians are now spending more, not just on essentials, but also on lifestyle and aspirational products. This rise becomes even more meaningful when seen alongside improving income levels and better access to credit.

Here’s Why Value Fashion Is Gaining Momentum:

Value fashion is growing quickly—and it makes sense. With more young people starting to earn and spend, the way they shop is changing too. They’re looking for clothes that are trendy, affordable, and easy to find—driving a clear shift towards the organized fashion market.

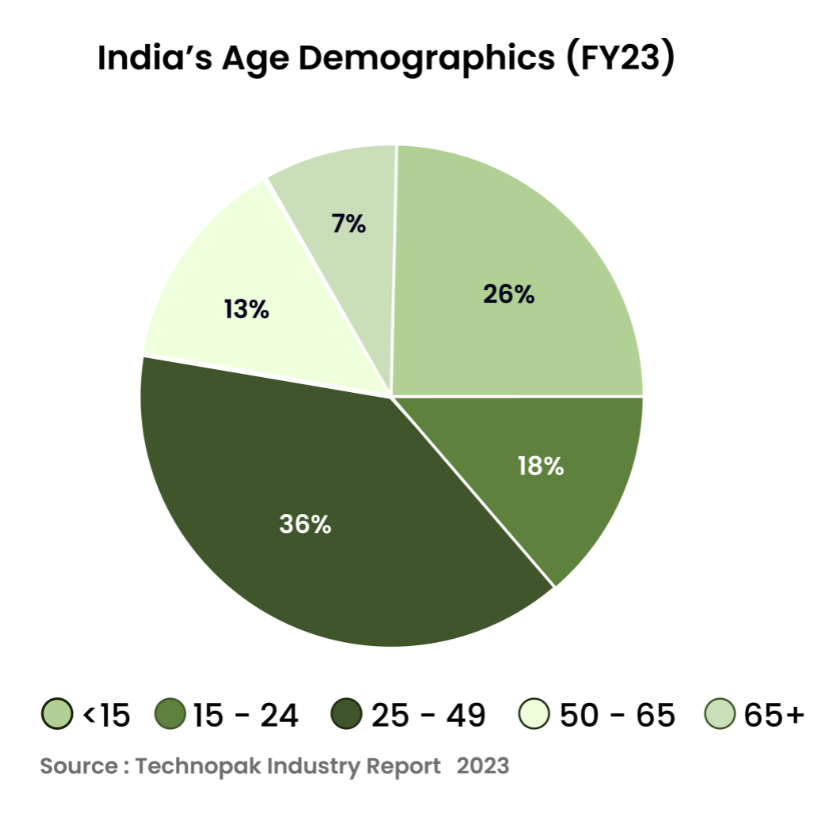

India’s biggest strength is its youthful population—with nearly 80% of people under the age of 50 and a dominant 36% in the 25–49 working-age group, the country is home to one of the largest consumer bases in the world. And it’s not just about age—it’s about behavior. Today’s Gen Z and millennials are driving a new wave of consumption. Unlike earlier generations who shopped for clothes just 2–3 times a year, this generation shops frequently, influenced by digital trends, social media, and a desire to express identity. But while their fashion needs are frequent, their lens is still rooted in affordability—which is exactly where value fashion fits in. It brings together style, aspiration, and accessibility—making it the go-to choice for a generation that wants more, but smarter.

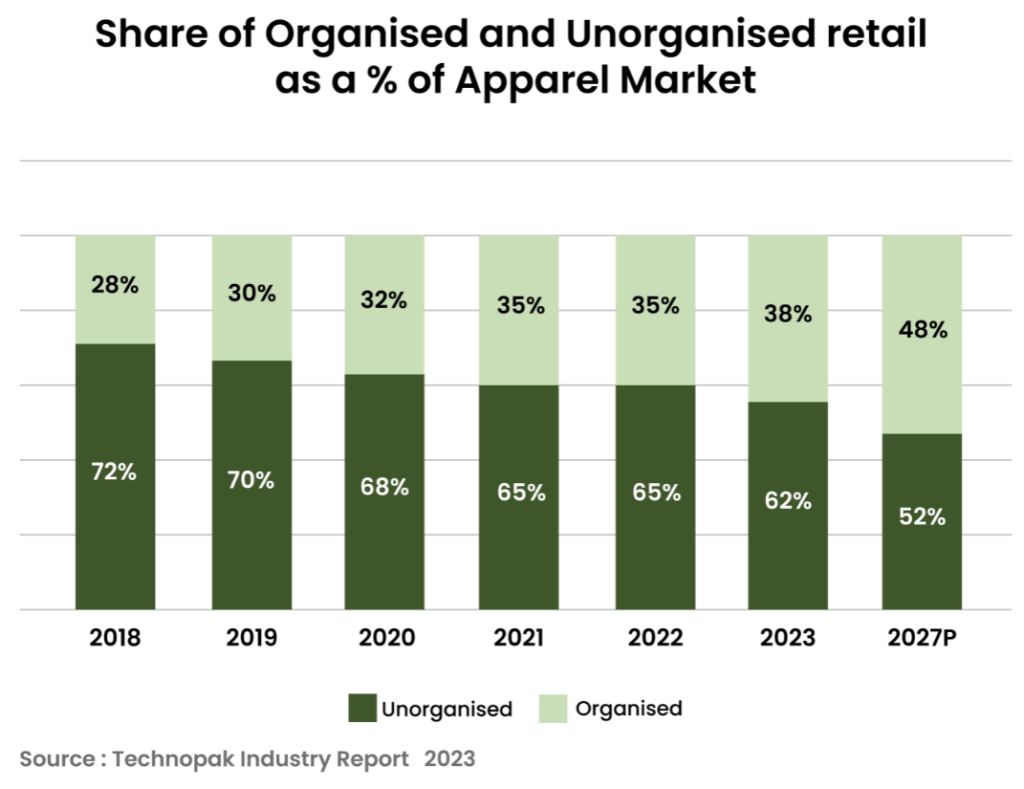

This shift in mindset is driving a major transformation: from unorganised to organised value fashion. Traditionally, a large part of India’s fashion market was dominated by unorganised players—local shops, roadside stalls, and small retailers. But that’s changing fast. As disposable incomes rise and expectations evolve, people are no longer just buying clothes—they’re looking for a better shopping experience. Organised brands are stepping in to offer that premium feel.

This has given rise to brands like Zudio and V2 Retail, who identified the demand for budget-friendly but trendy options. But how exactly are these brands making it work?

Zudio: Fast Fashion at Scale

Zudio, from the house of Tata, has redefined affordable fashion in India. What started as a metro-focused concept with trendy, budget-friendly clothing in air-conditioned stores with a premium-like feel, has today become the fastest-scaling value fashion brand in the country.

How Zudio Played the Game :

Zudio cracked the retail code by blending fast fashion principles—quick refreshes, in-trend designs, and mass availability—with price points accessible to India’s middle class. Its key strength lies in getting the right styles at the right time, thanks to a tight supply chain and consumer feedback loop. Instead of competing on variety, it focuses on simplicity, freshness, and impulse-friendly pricing.

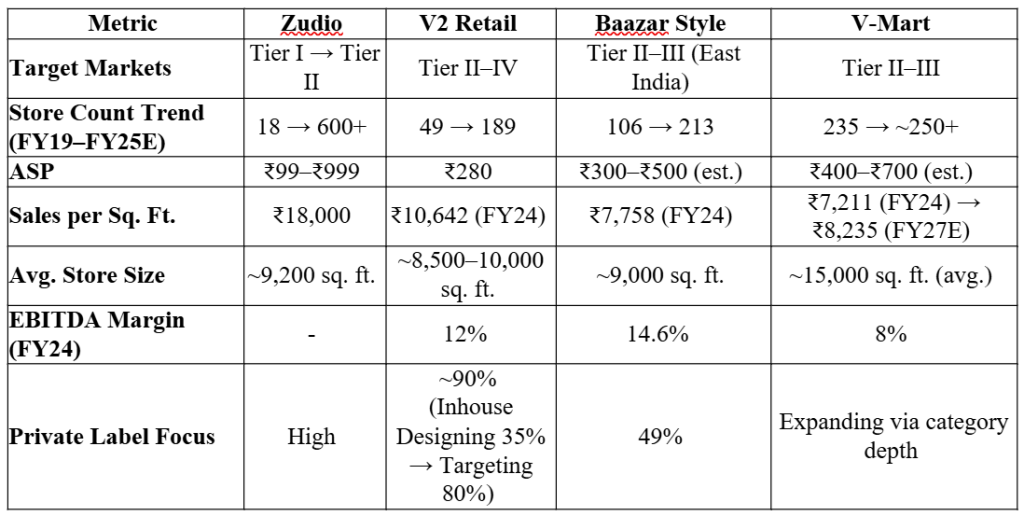

Zudio started with Tier 1 cities but is now aggressively entering Tier 2 towns, riding the familiar pattern that what works in metros eventually gets embraced in smaller cities. And with India’s younger generation shopping more frequently and affordably, Zudio’s model fits perfectly.

What’s Next for Zudio :

Zudio is building a moat through speed and scale. It’s strengthening backend supply chains and adding private label dominance, which not only drives margin but also ensures brand stickiness. The goal is clear: be India’s go-to brand for impulse fashion across every city.

V2 Retail: From Struggler to Challenger

V2 Retail, a rebranded version of the old Vishal Retail, is a story of turnaround. While once bogged down by Debt issues, it has found fresh momentum in Tier II to Tier IV towns, focusing on aspirational, affordable fashion for middle-income households.

How V2 Is Playing It Smart:

With an ASP of just ₹280, V2 directly targets the mass market. It’s not trying to imitate metro formats but instead has optimized layouts for maximum density—vertical shelving, limited SKUs per category, and high turnover of inventory. Around 35% of its merchandise is in-house, giving it price control and differentiation. This is expected to scale to 80%.

V2 is targeting to open 100 new stores in this financial year, signalling strong intent to scale aggressively. Backed by a lean balance sheet and internal accrual-led expansion, the company has also given a strong revenue growth guidance, supported by rising private label mix, better store productivity, and deepening presence in underpenetrated Tier II–IV markets—particularly in East and North India.

Baazar Style Retail: The Eastern Powerhouse

Baazar Style Retail (STYLEBAA) has carved out its niche by building dominance in Eastern India’s Tier II and III cities, especially in West Bengal, Odisha, Jharkhand, and Bihar. It caters to the neo-middle class—a segment that seeks branded experience without premium pricing.

Unlike its peers, Baazar Style goes deeper rather than wider. It follows a cluster-based expansion strategy, which helps lower logistics costs and improve brand visibility within regions. Its stores—averaging ~9,000 sq. ft.—are large enough to offer choice but still compact for smaller cities.

STYLE BAAZAR plans to open 40–50 stores every year, supported by internal accruals, without taking on major debt. The management is focusing on tech (SAP-led inventory control), regional demand analytics, and expanding into Tier IV towns, where over 5,000 markets are still largely unorganised.

V-Mart: The Trusted Brand of Bharat

V-Mart is the original poster child of value fashion in small-town India. With deep roots in Tier II and Tier III cities, V-Mart built its brand on reliability, assortment, and affordability. Post-COVID challenges slowed it down, but the company is once again gaining momentum through sharper execution and better product mix.

V-Mart’s Revival Play:

V-Mart is working on consolidating vendors, improving sourcing margins, and expanding into high-velocity categories like footwear, beauty, and accessories. It’s also focusing on optimising costs, especially rentals and backend operations. Its “Unlimited” format and the integration of Lime road are also part of its omni-channel ambitions.

The focus is on improving store throughput, expanding into high-margin segments, and creating a full-stack retail platform (offline + online). V-Mart’s strength lies in its strong brand trust and understanding of non-metro consumer preferences, which gives it an edge in a cluttered space.

India’s consumption story is no longer a theory—it’s unfolding in real time. With rising incomes, shifting income brackets, growing per capita expenditure, and a young population that shops more frequently and aspires for more, the stage is perfectly set. And value fashion, with its mix of affordability, trendiness, and improving retail experience, stands to gain the most. It’s not just regional specialists driving this wave—even retail powerhouses are stepping in. Reliance has launched Yousta, Aditya Birla is betting on Style Up, and Shoppers Stop is rolling out Intune—all aiming to capture this fast-growing market.