India’s Defence Sector: From Dependent to Dominant

June 18, 2025 | Deep Dives

Follow

Follow

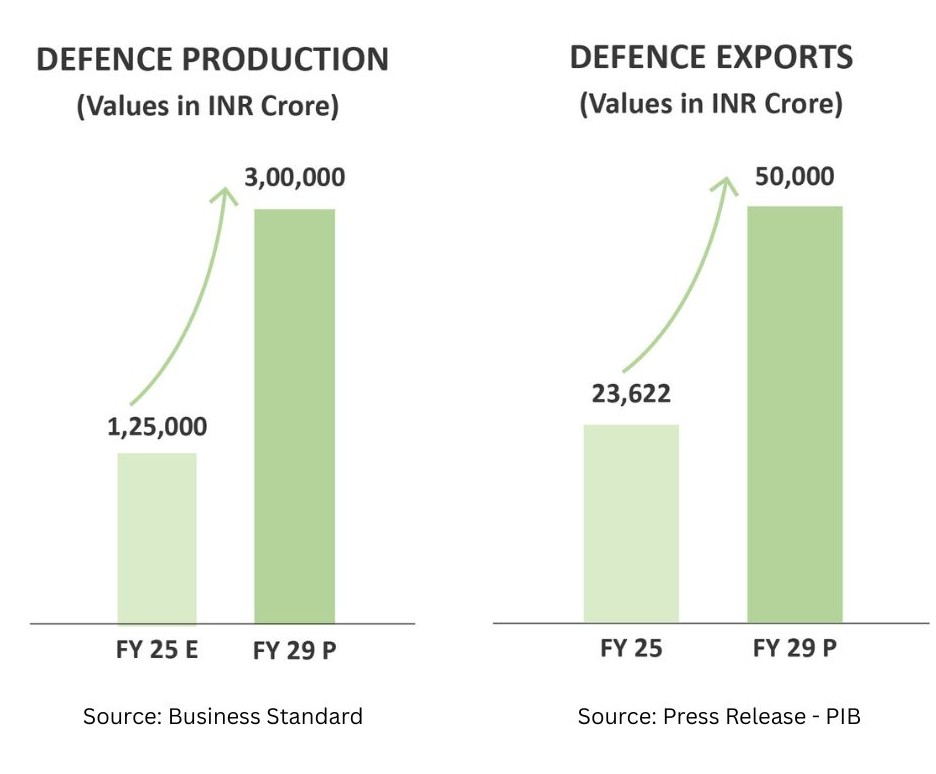

From DPP 2002 to DAP 2020, India’s defence procurement has evolved from a slow, import-dependent structure to a fast-tracked, indigenous-first ecosystem — unlocking a ₹3 lakh crore domestic opportunity and a ₹50,000 crore export ambition by 2030.

It started quietly.

A policy here. A reform there. A shift in mindset.

Then it picked up speed.

The defence sector is no longer what it used to be.

India, once a heavy importer, is now pushing the limits of innovation.

The evolution of India’s Defence Procurement Procedure (DPP) from 2002 to the Defence Acquisition Procedure (DAP) 2020 marks a significant shift from an import-dependent model to an indigenous, innovation-driven ecosystem. Starting with transparency reforms and the introduction of offsets in the early 2000s, the major turning point came in 2016 with the introduction of the Indigenous Design, Development, and Manufacturing (IDDM) category, prioritizing local design and production. DAP 2020 further accelerated this transformation with rationalized offsets, positive indigenisation lists, and support for startups and MSMEs.

The IDDM policy (Indigenous Design, Development, and Manufacturing) introduced in 2016 turned the tables. It made self-reliance a priority. Indigenous procurement has risen from ~25% in 2014 to ~68-70% in 2024, defence production value has grown from ₹70,000 crore to ₹1.27 lakh crore, and exports have surged from ₹6,600 crore to ₹24,000 crore, positioning India’s defence sector for a ₹3 lakh crore output and ₹50,000–60,000 crore in exports by 2030.

A New Era: India’s Defence Ecosystem and Emerging Opportunities

Historically, India depended heavily on foreign suppliers for critical defence equipment. While public sector undertakings (PSUs) like HAL and DRDO laid the foundation for indigenous capabilities, progress was slow and often limited to licensed production. However, the past decade has seen a decisive pivot. The turning point came with the launch of the “Make in India” initiative. This policy framework catalyzed private sector participation, streamlined procurement processes, and emphasized self-reliance. The introduction of Positive Indigenisation Lists, banning the import of over 5,500 items, created a guaranteed market for domestic manufacturers. With dedicated defence corridors in Uttar Pradesh and Tamil Nadu, liberalized FDI policies, and a more inclusive industrial approach, the private sector has moved from the sidelines to the centre of India’s defence ambitions.

Global geopolitics has only accelerated this trajectory. The disruption caused by the Russia-Ukraine conflict has forced nations to diversify their defence procurement away from traditional suppliers. India, with its neutral diplomatic posture and maturing industrial base, has emerged as a reliable alternative. Indian-made 155mm artillery shells, missile systems, and secure communication technologies are now finding demand from countries across Europe, Africa, and Southeast Asia. More importantly, India is not just supplying — it is co-developing solutions, moving up the value chain from being a manufacturing hub to becoming a partner in next-generation system development. Defence exports, which stood at ₹6,600 crore in 2014-15, have surged to ₹24,000 crore in 2023-24. The government has laid out an ambitious target of ₹50,000 to ₹60,000 crore in exports by 2030, firmly placing India among the leading defence exporters globally.

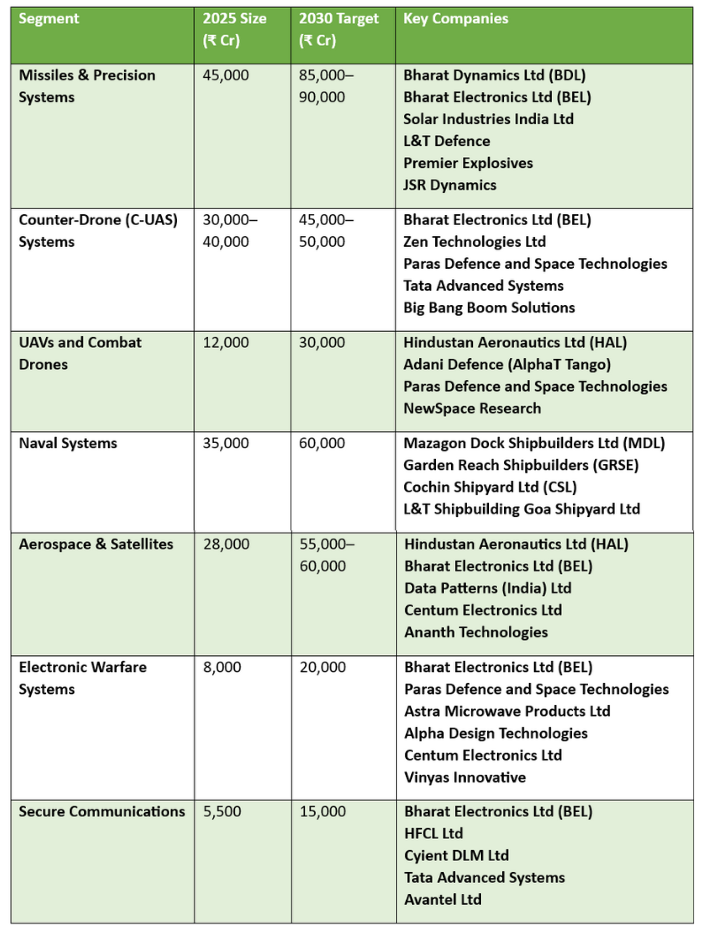

At the core of this transformation lies a robust and multi-layered defence ecosystem. India has moved beyond traditional arms imports and licensed production models, establishing itself in areas like missile technology, unmanned systems, counter-drone technologies, and aerospace platforms. Indigenous missile programs such as BrahMos, Akash, and Astra have matured to the point where India is not just self-reliant but is actively pursuing export markets. Meanwhile, India’s focus on developing combat drones and surveillance UAVs, alongside indigenous initiatives in naval platforms like destroyers and submarines, underscores the ambition to secure a dominant share in both regional and global markets. In aerospace, the success of platforms like the Tejas Light Combat Aircraft and Light Combat Helicopters (LCH) marks India’s transition from licensed assembly to full-cycle manufacturing and system integration.

However, the real revolution is unfolding in enabling and emerging defence technologies. India is rapidly innovating in electronic warfare systems, secure communications, and counter-drone solutions. As warfare evolves into domains driven by cyber, space, and unmanned systems, India’s defence manufacturing base is keeping pace. Indigenous firms are leading advancements in radar, sonar, and jamming technologies, while secure encrypted communications — essential for network-centric warfare — are becoming core competencies for Indian companies. The counter-drone segment, in particular, is witnessing explosive growth. India's response to the growing threat from UAVs involves cutting-edge solutions ranging from RF jammers to hard-kill laser interceptors, positioning the country as a key player in what is fast becoming a global security priority.

The scale of this transformation is best understood through numbers. These projections are not aspirational; they are anchored in structured policy support and market shifts that India is exploiting astutely.

Niveshaay’s Approach to India’s Defence Manufacturing Shift

India’s defence and aerospace sector is undergoing a profound transformation. At Niveshaay, we believe this shift is not just policy-driven but powered by a new generation of companies — entrepreneurs and engineers who are quietly building the backbone of India's strategic independence.

While evaluating opportunities in India's growing defence and aerospace sector, we focused on companies deeply aligned with the Make in India initiative, offering differentiated capabilities and addressing critical gaps historically filled by imports. In building a truly self-reliant defence sector, it rests equally on two critical pillars: companies that innovate at the system level through research and development, and companies that quietly supply mission-critical subsystems and components, enabling these platforms to perform.

Our approach to investing in India's defence and aerospace sector reflects this dual view. Our conviction in India’s defence sector is reflected in the companies we have invested in — businesses building indigenous capabilities across missile systems, aerospace, secure communications, and defence electronics.

- R&D-Driven System Innovators:

Companies like Zen Technologies, Avantel, and JSR Dynamics represent this cohort. These are businesses that believed early in their ability to develop indigenous technologies — simulators, secure communications systems, and precision-guided munitions — and have built strong positions through sustained R&D efforts.

- Strategic Ancillary Enablers:

On the other side are companies like Centum Electronics, Vinyas Innovative Technologies, HBL Power Systems, and Premier Explosives. These companies provide the essential subsystems — defence-grade electronics, power solutions, and specialized propellants — that power India’s strategic platforms across land, air, sea, and space. While they operate behind the scenes, their contribution is indispensable to the functioning and reliability of complex defence systems.

Below, we share a closer look at select companies from both categories that we once invested with, each playing a unique role in strengthening India’s defence and aerospace future.

Zen Technologies Ltd.

Zen Technologies exemplifies the power of perseverance and indigenous innovation in India’s defence sector. In the early 2010s, while larger players hesitated, Zen was quietly building live-virtual-constructive simulators and developing early prototypes for counter-drone systems around 2017— a segment still nascent globally. Despite facing slow-moving defence procurements, Zen stayed the course, refining its simulators through Army field exercises and rigorously improving its drone detection and neutralization technologies. This commitment paid off with significant order wins, and today, Zen stands as a market leader in military simulators and counter-drone technologies, offering solutions critical for modern battlefield readiness and homeland security.

Avantel Ltd.

Avantel’s journey reflects the same ethos of disciplined innovation and resilience. Focused on secure communications, Avantel invested early in developing encrypted microwave links and ruggedized communication routers, often embedding ex-servicemen and DRDO veterans to fine-tune its offerings. Unlike many contemporaries who scaled back during procurement delays, Avantel doubled down on R&D, iteratively hardening its products for real-world military requirements. By 2018, Avantel’s persistence was rewarded with a multi-year contract to supply secure communication systems to armoured divisions — a move that transitioned the company from break-even to consistent profitability. Today, Avantel is recognized for its critical role in delivering secure, resilient communications infrastructure for India’s armed forces, with a strong reputation for reliability in hostile environments.

Centum Electronics Ltd.

Centum Electronics stood out for its role as a key ancillary partner to India’s aerospace, defence, and space programs. Their full-stack capability — from design to mass manufacturing — and deep partnerships with clients like DRDO, ISRO, and Thales have made them strategic contributors to marquee projects like Chandrayaan, Mangalyaan, Aditya-L1, and the T-90 tank upgrade. Their move towards complete satellite builds and system integration further strengthens their positioning as India scales up space situational awareness and ISR capabilities.

Vinyas Innovative Technologies Ltd.

In Vinyas Innovative Technologies, we found a company advancing India’s defence indigenisation agenda through its participation in critical programs like multifunction naval radars, AESA radars, and UAV payloads. Their transition from PCB assembly to qualified system integration, coupled with critical global certifications, positions them well to serve both domestic and export-controlled markets, aligning with the long-cycle defence electronics opportunity we see emerging.

HBL Power Systems Ltd.

HBL Power Systems impressed us with its niche focus on high-complexity defence technologies like submarine batteries, thermal batteries for strategic missiles, and electronic artillery fuzes — areas with limited competition. Their sustained in-house R&D efforts and strategic backing of companies like Tonbo Imaging reflect a broader commitment to building indigenous defence capabilities. We see HBL as a key beneficiary as India shifts from imports to local manufacturing in strategic technologies.

Premier Explosives Ltd.

Premier Explosives caught our interest due to its position as the sole indigenous manufacturer of chaffs, flares, and solid propellants critical to India’s missile programs, including Astra, Akash, LRSAM/MRSAM, and Agni. Its approved supplier status for ISRO’s PSLV program further extends its strategic relevance. The company’s focus on specialized defence and space-grade explosives, supported by in-house R&D capabilities and limited domestic competition, aligns closely with critical national security and space infrastructure requirements.

JSR Dynamics Ltd.

Finally, JSR Dynamics caught our attention with its R&D-led approach to precision-guided munitions (PGMs) — glide bombs, decoys, and range extension kits — where dependency on imports has traditionally been high. With complete in-house design and IP ownership under the leadership of Air Marshal Shirish B. Deo (Retd), and a strong order book from premier defence clients, JSR is uniquely placed to capture a significant share of India's growing guided weapons market.

These companies adopted a common formula: maintain discipline through downturns, continue R&D when others paused, and refine products relentlessly based on real-world feedback. Their growth was neither sudden nor accidental; it was the outcome of slow and deliberate execution. Together, these companies represent differentiated plays on India's defence self-reliance journey, each targeting strategic areas where the demand is structural, giving us long-term confidence in their growth trajectory.

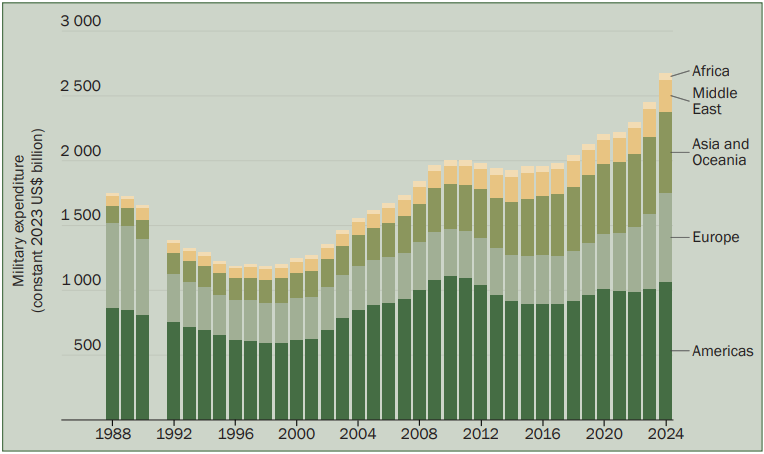

Global Military Budgets Surge

In 2024, global military spending reached an unprecedented $2.72 trillion, reflecting a 9.4% increase from the previous year, driven largely by escalating geopolitical tensions in Europe and the Middle East. Europe saw a 17% rise in military expenditure, reaching $693 billion, with Germany's spending increasing by 28% to $88.5 billion, Poland's by 31% to $38.0 billion, and Russia's by 38% to $149 billion, surpassing Cold War-era levels. The Middle East also saw significant growth, with military expenditure reaching an estimated $243 billion, up 15% from 2023, and Israel’s military spending surging by 65% to $46.5 billion, the largest increase since the Six-Day War in 1967. In Asia, China’s military expenditure grew by 7% to $314 billion, marking three decades of continuous growth, while Japan’s spending rose by 21% to $55.3 billion, the largest annual increase since 1952. Meanwhile, the USA, maintaining its position as the largest military spender, saw a 5.72% increase in its defence budget, bringing it to approximately $877 billion, a reflection of ongoing global security concerns and military expansion efforts.

Global Military Expenditure: A Surge in 2024

Source: SIPRI Military Expenditure Database, Apr. 2025

India's defence expenditure increased by 4.6% from $82.29 billion in 2023 to $86.12 billion in 2024. India's defense sector is experiencing significant growth, with major private players like Tata, L&T, and Adani increasing investments and consolidating capabilities. The private sector now contributes around 20.8% of India's total defence production, valued at ₹1.27 lakh crore in FY24, and accounts for 60% of defence exports. Tata Advanced Systems is forming a unified defence arm (Tata A&D) by merging its defence businesses to focus on larger, global projects. L&T is producing Zorawar light tanks and advanced submarine systems, while Adani Defence is expanding its portfolio through strategic acquisitions and joint ventures.

The defence ecosystem is rapidly evolving, which includes critical suppliers of raw materials, components, and specialized machinery for defence systems. The increasing number of defence-tech startups is further bolstering the ecosystem, providing innovative solutions in areas such as artificial intelligence, machine learning, and robotics, thereby contributing to the overall technological sophistication. The government's push for indigenization under the "Make in India" initiative has spurred the creation of state-of-the-art manufacturing facilities and has attracted global players to establish joint ventures and technology transfer agreements, further enhancing domestic production capabilities.

The sector is also witnessing a shift towards high-growth opportunities, driven by strong government support and rising investments. In FY24 alone, ₹2,000 crore was invested in defence-tech startups. Post the India-Pakistan war, the Indian defence sector is becoming an increasingly attractive area for investors. Heightened tensions would likely lead to increased defence spending driven by emergency procurement. However, investors should be mindful of challenges such as lengthy order execution, long inventory cycles, and working capital management. Despite these hurdles, the rising deal flow and increased fundraising activity signal robust opportunities, with the potential for high rewards.

The journey is far from over, and we continue to explore more opportunities aligned with India’s shift toward self-reliance and global competitiveness.

Disclaimers and Disclosures

SEBI Registration No. :INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607 | BASL Membership ID: 6276

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing. The securities quoted are for illustration only and are not recommendatory. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.