India's Solar Manufacturing: Clarification on recent MNRE circular

The Extraordinary Growth Story

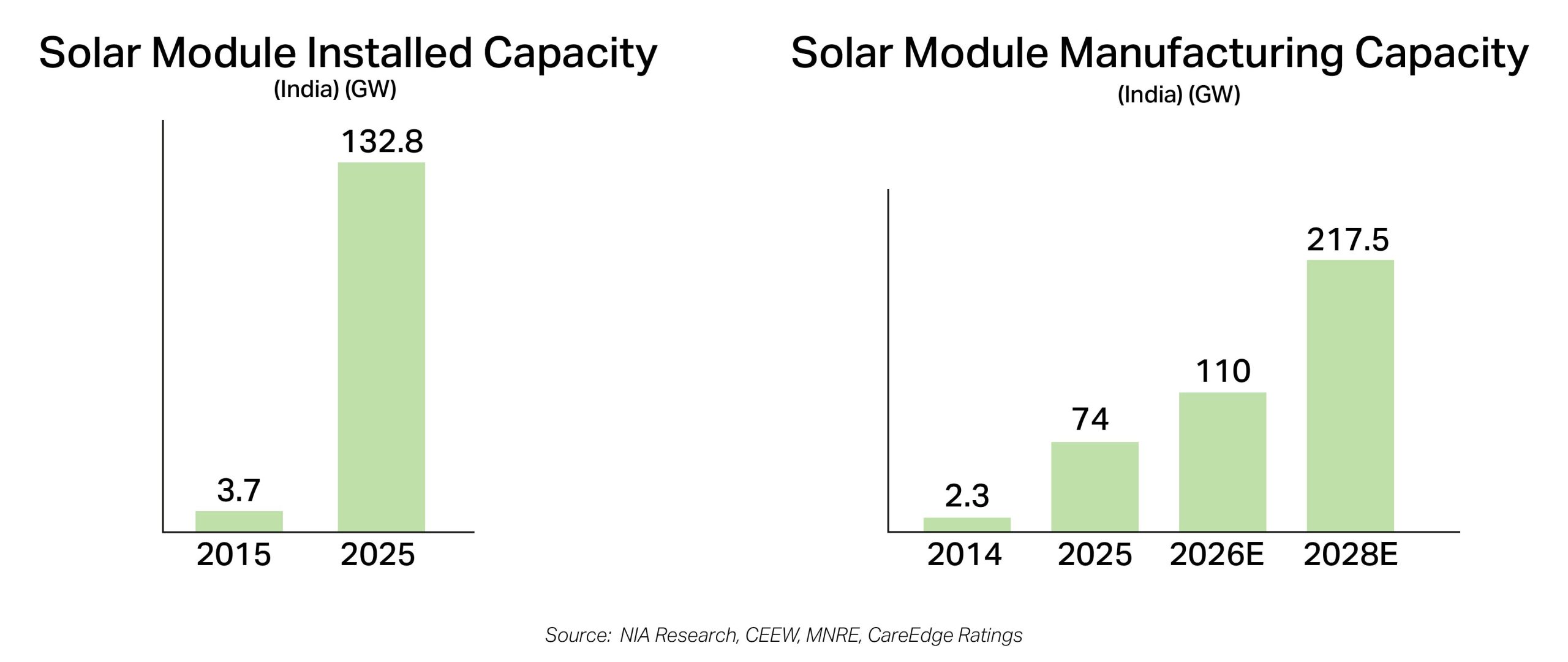

India’s solar expansion over the past decade has been extraordinary. India had just 4 GW of installed solar capacity 10 year ago. Today, it stands at ~132.8 GW, making India the world’s third-largest solar nation after China and the United States. But manufacturing has grown even more aggressively. India’s module manufacturing capacity has risen from ~2.3 GW in 2014 to ~74 GW by March 2025. This is expected to cross ~110 GW by March 2026 and approach ~215-220 GW by 2028. This explosive capacity addition, while impressive on paper, could lead to a significant mismatch- expected to create distress in the market.

The solar journey for us has been equally exciting — particularly backing industry leaders during their ramp-up phase, where favourable policies and superior economics drove exponential growth. As with any high-growth sector, strong profitability inevitably invites capacity expansion. Over the past year, we have consistently highlighted that standalone module manufacturers will come under pressure as numerous smaller capacities enter the market, intensifying competition and setting the stage for industry consolidation.

In such a landscape, niche, lower-competition integrated and component players — notably solar glass manufacturers — are well positioned to benefit as module capacities expand and the ecosystem shifts toward grid stabilisation and energy storage. With robust cash flows, scale, and disciplined capital allocation, they are best placed to outperform and sustain leadership as the solar industry continues on its strong structural growth trajectory.

The Confusion: What Did MNRE Actually Say?

Recent weeks saw considerable confusion in the renewable market following reports that the MNRE had recommended NBFCs halt lending to the renewable energy sector due to overcapacity concerns. The ministry quickly issued a clarification, stating there has been no advisory to Financial Institutions for stopping lending to either renewable energy power projects or to renewable energy equipment manufacturing facilities.

However, the clarification revealed something more nuanced and strategically important for the industry as well as the investors. MNRE confirmed it had shared information about domestic manufacturing capacities with the Department of Financial Services and institutions like PFC, REC, and IREDA. It emphasized that it is not retreating from renewable energy—it is encouraging smarter capital deployment toward difficult-to-replicate parts of the value chain rather than being limited to financing solar module manufacturing alone.

This includes upstream manufacturing (cells, wafers, polysilicon) and critical components (solar glass, frames, backsheets, junction boxes) where India needs to build capability. This is not a blanket warning on solar—it is a targeted message about where overcapacity exists and where investment is still needed.

The Reality of Overcapacity: Uneven Impact

Large players like Waaree, Adani, Premier, Vikram, etc continue to run at about 80–85% capacity. But many smaller manufacturers are struggling to utilize even 20–25% as they face higher inventory losses and weaker margins. Clients of module-only players are leveraging the oversupply and minimum product differentiation to negotiate aggressively.

While modules face severe overcapacity, upstream segments present a fundamentally different picture. Manufacturers with strong balance sheets, and deeper integration spanning cells, ingots, and wafers, are relatively better placed as they can absorb volatility in any single segment. Integrated players are able to control costs, achieve economies of scale and invest in technological upgrades while smaller players struggle to keep plants running.

The Indian government’s push to backward integrate creates both pressure and opportunity—but these segments have not seen an aggressive capacity addition as modules. The reason is straightforward: capital intensity and technical complexity. CAPEX per GW for each integration can be Rs. 500-600cr versus Rs. 100cr for only-modules. Beyond the capital requirement, these are technically challenging, involving significant complexity that creates natural entry barriers. The supply-demand dynamics here remain far more balanced, protecting margins and creating sustainable business models for players with required technical capabilities.

We believe 6-7 large industry players who are able to vertically and horizontally integrate will ultimately hold scale advantages, with rest of the players expected to consolidate or shut down by end of the decade.

The Component Story: Strategic Chokepoints in the Value Chain

MNRE’s clarification specifically mentioned solar glass and aluminium frames as areas where lending should be expanded, recognizing these as strategic components were domestic capacity needs development. This is not coincidental—components represent the parts of the value chain where India still has significant import dependence and where technical barriers provide natural protection against overcapacity.

The consolidation in modules doesn’t eliminate component demand—it concentrates it among stronger, more creditworthy players. Consider Borosil renewables, one of our investee companies and a solar glass player. Unlike modules, solar glass manufacturing and stabilization take considerable time to set up. The technical challenges of preparing consistent quality glass mean capacities will not come online quickly despite increase in domestic demand. This barrier creates a natural protection against the kind of rapid overcapacity seen in modules.

The government’s push to protect domestic component manufacturers through anti-dumping duties would further strengthen their competitive position. Borosil supplies product to multiple customers maintaining bargaining power as compared to manufacturers competing in an oversupplied end-product market.

Our View

The module overcapacity will coexist with opportunities in upstream and specialised component manufacturers who occupy strategic, hard-to-replicate positions in the supply chain and will emerge stronger from this consolidation. Even these players will face near-term margin pressure as overcapacity works through the system but the long-term theme remains intact. Success requires differentiation—identifying players with technical moats, capital advantages, and positions in supply-constrained segments rather than commoditized, oversupplied ones.

The Indian solar manufacturing story is maturing. The module segment’s overcapacity is real and will drive painful consolidation, but this is a natural evolution, not a crisis. India’s solar story remains compelling, but returns will accrue only to those positioned in the right parts of the value chain—where sustainable economics prevail over structural headwinds.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR