India's Energy Risk: Why Green Energy Is the Structural Answer

Nearly 9 out of 10 barrels of oil India uses, are imported. That single fact costs ₹4.10 lakh every second. And it is the main reason green energy has become a national priority.

India has sunlight that most countries would build an entire energy policy around.

It has wind. It has engineers. It has land.

What India never had is an energy system that actually uses any of this, at home, at scale.

That is changing now.

When You Buy Energy from Outside, You Accept Conditions You Never Agreed To.

Four risks come bundled with every barrel of imported oil.

- Price: The global market sets it. A decision made in Riyadh or Moscow, and India’s fuel bill changes overnight.

- Supply: Most of India’s oil comes from the Middle East and Russia. If something goes wrong in either place, there is no backup at home.

- Route: The oil travels through the Strait of Hormuz, a 54-km waterway India has no control over. Even paid-for oil still has to get here.

- Currency: Oil is priced in dollars. Every time the rupee weakens, the same barrel costs more, even if the global price hasn’t moved.

India’s crude oil import bill, FY26: $134 billion, roughly ₹11 lakh crore.

A 5% shift in the exchange rate: Adds thousands of crores overnight, without anyone raising the price of oil.

A single conflict thousands of kilometres away can reprice every litre of petrol in India overnight, as we are witnessing right now.

The Hidden Dependency Inside the Dependency

The ~88% import dependency number understates the real problem.

India’s import bill fell recently partly because it shifted heavily to discounted Russian crude. Russia’s share of India’s imports went from just 2% in FY20 to 35.8% in FY24–25.

That looked like smart procurement. What it actually did was concentrate a new geopolitical risk in one direction.

- In August 2025, the US placed punitive tariffs specifically targeting India’s Russian oil purchases, bringing total US duties on Indian exports to 50%.

- US sanctions on Rosneft and Lukoil, which supply 60% of India’s Russian crude, created immediate payment disruption.

- Russia’s share fell from 35.8% to 21.2% in a single quarter, not because India chose to diversify, but because the geopolitical floor gave way.

India traded Middle East price risk for Russia political risk.

Both are import dependent.

The only structural exit is a domestic energy system that reduces how much oil India needs from anyone.

The Feedback Loop Nobody Talks About

When oil prices rise, India’s import bill increases → the current account deficit widens → the rupee weakens → oil costs even more in rupee terms → the RBI must defend the currency by selling dollars → reserves fall.

RBI dollar sales in FY26: over $100 billion in spot and forward markets to defend the rupee

Forex reserve drawdown (Feb–May 2026): $728 billion → $690 billion, a $38 billion fall in three months

The ₹11 lakh crore import bill is the visible cost. The ₹9.58 lakh crore in RBI intervention is not reported alongside it.

Together, they are what oil dependency actually costs, not just in foreign exchange, but in rate cuts postponed and monetary policy flexibility surrendered.

Every unit of domestic renewable electricity produced removes one unit of this loop from the system.

The Gap That Keeps Widening

Domestic oil production FY12: ~38 MMT

Domestic oil production FY25: ~28.7 MMT, a 25% drop over 13 years

Demand kept growing at 4–5% every year. The gap gets filled by imports, and it widens every year.

Importing more is not a solution. It is the problem. The only fix is a new domestic energy system built on what India already has.

What Europe 2022 Proved

In 2022, Russia cut gas to Europe. Industrial electricity spiked to €0.20–0.30/kWh, two to three times normal.

- Aluminium smelters shut down

- Fertiliser plants relocated to cheaper countries

- Chemical makers started looking for new locations

Manufacturing follows the lower-cost electricity. Always. Europe 2022 proved it in real time.

Europe’s response was REPowerEU, an emergency domestic renewable buildout.

Gulf states put sovereign wealth into solar.

China built 80%+ of global solar manufacturing.

India is now building the same system, with one advantage none of them had at the time:

solar already costs ₹2.5/kWh.

Green Energy Changes the Address

An electron from a solar panel in Rajasthan has no Hormuz risk. Its supply cannot be disrupted overseas. Its price cannot be set by another country.

Solar tariff in 2010: ₹10.95/kWh

Solar tariff in 2026: ~₹2.5/kWh

Decline: 77% in 15 years, driven entirely by technology, not policy

That is not a subsidy outcome. It is a cost curve. And cost curves only go one direction.

The Milestone That Just Happened

New solar capacity FY26: 44.6 GW, an 87% year-on-year increase, highest ever in a single year

Cumulative installed (March 2026): 150.26 GW, world’s third-largest solar-base.

PM Surya Ghar scheme: 2.6 million homes covered; rooftop solar up 69% YoY.

2030 non-fossil target: 50% achieved, five years early. Target now raised to 60% non-fossil by 2035

The cost curve did this. Not mandates. Not subsidies. Technology economics.

What This Means in Rupee Terms

India spends ₹12–14 lakh crore per year on energy imports. But that number becomes real when you see where most of it goes.

Transport consumes 60–70% of all petroleum India uses. Every petrol pump, every highway truck, every auto-rickshaw- that is where the import bill lives.

That makes transport the single highest-leverage point for substitution. And the substitute is already cheaper.

Replacing even 20% of transport fuel with domestic renewable electricity saves ₹2.4–2.8 lakh crore annually, money that stays inside India instead of leaving as foreign exchange.

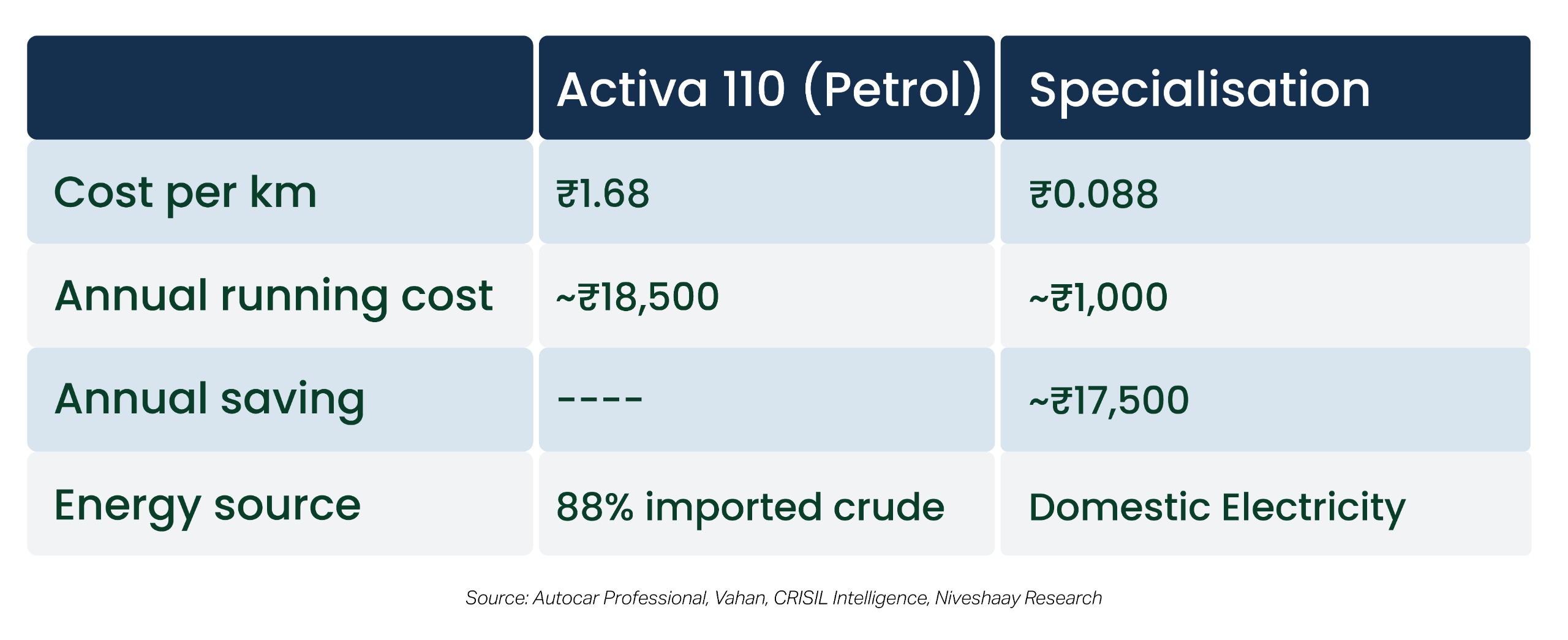

The numbers at the vehicle level make it concrete.

₹17,500 saved per vehicle, without any subsidy. India has 300 million two-wheelers.

At national scale, that is not a transport story. It is a balance-of-payments story.

Investor’s Perspective

· The energy address shift is a multi-decade investment theme.

· Every rupee of import substitution flows through domestic IPPs, grid infrastructure, EV manufacturing, and battery storage.

· India’s T&D market alone represents ₹9.15 lakh crore of committed capex through 2032, not projected, tendered and executing.

· The solar manufacturing base at 210 GW module capacity is an export platform, not just a domestic supply story.

· The question for an investor is not whether this transition happens. It is which part of the value chain captures the value as it does.

Key Insight:

Green energy moves India’s energy address from abroad to at home. This argument is not about climate. It is about who controls the price, the supply, and the route. Right now, that is not India.

Green energy changes that, structurally, permanently, and faster than most analysis has priced.

→ The energy address is changing. But the second layer of this story arrived faster than anyone expected, because AI suddenly needs electricity in amounts no grid was designed for.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR