Indian Paper Industry – Tactical Play on JK Paper Ltd.

Inside the report

- Part I: Indian Paper Industry

- Recent Trends in Paper Industry

- JK Paper

- Why JK Paper?

- Part II: Indian Paper Industry

- Part III: How is it different from global industry?

- Indian Paper Companies: Classification based on Raw Materials Used

- Financials

Research Analyst - Gunjan Kabra (info@gunjankabra.com)

The Paper Industry is classified into four segments:

- Printing and Writing (30%)

- Coated

- Uncoated: Creamwove, Maplitho, Copier

- Packaging and Paper Board

- Duplex Boards (used in small –packaging: FMCG)

- Kraft Paper (used in packaging for transportation)

- Specialty Papers (9%)

- Tissue Paper

- Newsprint (15%)

Characteristics of the Indian Paper Industry

- Capital, Energy and Water Intensive

- The paper factories in South India are facing issues in sourcing water, so one should be careful while choosing a company as the requirement of water is huge.

- Fragmented

- Small units account for ~60% of the Industry Size.

Paper can be produced by any of the following Raw Materials:

- Wood Pulp (30-35% paper is made from wood pulp): Hardwood and Softwood

- Waste Paper (45-50% paper is made from Waste Paper)

- Agri Residue (20-22% paper is made from Agri Residue)

Raw Materials used in producing paper will help you in identifying which company to invest in based on the industry dynamics.

- High demand and scant supply in Europe driving increase in paper prices

- Restricted supply and high energy cost put upward pressure on prices

Against the background of an unprecedented rise in energy prices and other costs, paper producers have almost doubled prices for their products (fine paper grades) compared to January last year. Paper manufacturers explain that in some of their mill's production costs have risen by several hundred euro per tonne of paper.

- Strike at UPM, Finland leading to supply issues

UPM supplies Europe with about 40 percent of the backing sheets for labels.

- Russia-Ukraine War Impact

How much paper and board does the EU export to and import from Russia and Ukraine?

Pulp and paper trade between the EU and Ukraine goes mainly one way: about 440,000 t of paper and board are imported by Ukraine from the EU. Ukraine's exports are very limited.

When it comes to Russia, around 900,000 t of paper and board are imported by Russia from the EU, while Russia exports close to 700,000 t to the EU (accounting for 50% of the Russian exports). Regarding pulp, EU-Russia trade is quite balanced with around 400,000 tonnes traded in total.

2. Rise in prices of Waste Paper/Kraft Paper, availability being an issue

- From February 1, the US waste paper rates have been increased to $400 from $300 a tonne.

- Ban on exports of waste paper from Europe to India likely to get resolved.

- The corrugated box manufacturer, recycled paper manufacturers are having a hard time in sourcing raw materials and maintaining margins. Viability is becoming an issue for small players.

- Waste Paper isn’t a high value item to afford such huge freight costs whereas pulp is a high value product. Hence, the high freight costs are still manageable comparatively.

3. Also, when the global wood prices are higher, Indian paper manufacturing companies tend to become competitive and are expected to perform well.

Under normal circumstances, Indian paper companies become globally competitive when the prices are beyond $650-700/tonne. The reason is discussed in detail in the later part of the report.

4. Paper Demand is back to normal with higher demand on the packaging side

Office paper demand is back to normalized levels. Also, with the opening of schools, the demand for paper is expected to resume to normalized levels.

Currently, the industry dynamics guide that wood-pulp-based paper manufacturers are expected to do well. Also, keep in mind that a vertically-integrated business model is a huge added advantage and should be given a preference.

Increased E-commerce penetration, anti-plastic sentiment, a recycled feature of the paper is leading to increased demand for paper.

5. Cost Pressure

The cost of production is increasing on all fronts, from raw material, chemicals to power and logistics.

Also, consider that the paper industry is a cyclical industry. We prefer sticking to a market leader who has been able to maintain its growth, margins and has already done capex.

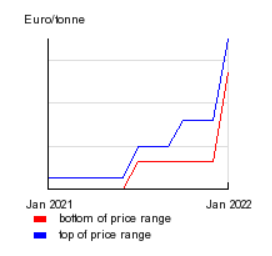

6. Recent Price Trend

The buoyancy in the prices continues due to issues in raw material availability, rise in chemical prices, logistics prices. Mondi, a leading packaging company in Europe highlighted in its conference call on 3rd March 2022 that the prices are 20-25% higher than the average of 2021. The high-cost base remains amid favorable demand and tight supply scenarios.

With hike in prices by recycled paper manufacturers, Wood Pulp based manufacturers also took a hike even when their raw material prices remained stable.

Vertically-Integrated Business Model is a huge added advantage and should be given a preference. When wood pulp prices are higher globally, Indian companies tend to become competitive.

Hardwood: Domestic secured supply

Softwood: India is import dependent

About the Company

- Leading player in Office papers, Coated papers and Packaging boards

- It has a ~24% market share in the branded copier segment, 12% in coated paper segment and 13% in packaging board segment in India.

- Robust distribution network of over 300 trade partners and 4000 dealers with 15 pan-India depots

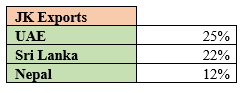

- 15% revenue is derived from export markets

- Export Destinations:

- Industry Dynamics suggest wood-pulp based companies are expected to perform well.

- It’s a leading wood-pulp based paper manufacturer. As explained above, this is expected to perform well.

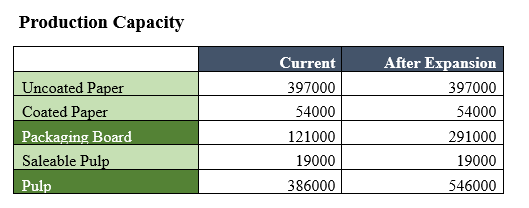

2. Capacity Expansion:

- Packaging Board Plant Commenced in Jan 2022

The company did an expansion by 170,000 TPA in the packaging board segment at Songadh, Gujarat to take advantage of this growing segment in the paper industry. The company also set up a pulp mill to cater to the new expansion.

The packaging board was commissioned in Jan 2022. The plant is operating at 80% C.U. and is expected to reach 90% in the next 2-3 months. At peak capacity, it is expected around Rs. 1200-1600 crores of revenue ending on the price realization. 10-15% of the revenue from this plant is expected to be derived from exports.

- Plans to set up a corrugated packaging paper in Ludhiana

Capex- Rs. 150 crores

Peak Revenue: Rs. 150-170 crores

Commencement: Q2 FY23

Revenue Target Guidance: ~Rs. 3500 crores in FY22

- Acquisition of Sirpur Paper Mills

In Aug-2018, JK Paper had announced the acquisition of sick company Sirpur Paper Mills. It has an integrated paper and pulp mill with a capacity of 1,38,000 tonnes per annum. Currently, it is operating at 80% capacity utilization and is expected to reach 90% in Q1 FY23.

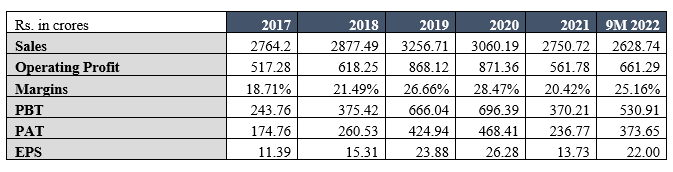

3. The company has been able to maintain sales growth and range-bound EBITDA margins

4. Rise in demand for packaging:

- Growth in E-Commerce

This segment can lead to a huge demand for paper boards. With fall in the price of waste paper and rise in the finished paper can lead to an increase in turnover and profitability for companies making Duplex Board. For example, Smruti Kappa and Mondi are the leading Packaging companies who got benefitted due to e-commerce growth, improving European Industrial production.

- Plastic Ban

- Companies like Mc. Donalds have limited the use of plastic and encouraging more use of paper (shift to paper straws)

- Hotel Chains are now focussing to eliminate plastic and shifting to glass bottle and paper-based products.

- India is a growing country

The growth in the paper industry is linked to the growth of the economy. More Industrial Production translates into more demand for packaging boxes.

Over years, Indian Paper Industry hasn’t been able to compete with the international players on account of the higher cost of production due to a deficit in wood pulp availability, not enough availability of waste paper, etc. According to IPMA, the cost of domestic wood in India was higher by almost $30-40 tonnes as compared to other Asian Countries. Due to this single factor, the cost of paper production in India used to be higher by $100 a tonne.

By FY2010, the paper industry was facing a supply deficit. Hence, the companies started expanding capacities. the industry saw significant capacity additions of 1.6 million MT during FY09 - FY11 (~15% of domestic paper capacity in FY09), particularly in the Printing and Writing Paper segment. This led to an over-supply scenario, build-up of inventories together with pricing pressures. Moreover, there was also an issue in sourcing wood pulp. There wasn’t enough availability of wood pulp domestically for the new capacities added. As a result, companies had to import higher expensive wood pulp. The companies were unable to pass on the higher prices to consumers and at the same time also faced stiff competition from cheap imports. Profits were severely impacted, especially for leveraged companies. After this, the industry along with government measures has taken steps to be self-sufficient in sourcing wood pulp locally.

Indian paper industry is highly fragmented: the top 3 players account for only 9% market share unlike 68% in USA, 72% in Indonesia and 21% in China. The Indian Paper Industry should also consolidate gradually

- Wood-Pulp

i. JK Paper (Writing, Printing and Packaging Board)

ii. West Coast Paper Ltd. (Writing, Printing and Packaging Board)

iii. Seshasayee Papers Ltd. (Writing & Printing Paper)

iv. Orient Paper & Industries Ltd. (Writing, Printing and Speciality Paper- Tissues & Chemicals)

v. Star Paper Mill Ltd. (Cultural Papers & Industrial Paper)

vi. ITC (Paper Board)

vii. Andhra Paper (Wood Pulp and Recycled Fibres: Writing and Printing Paper)

2. Waste Paper

i. South India Paper Mill (Paper Boards)

ii. Emami Paper Mills Ltd. (Newsprint, Printing & Writing Paper, Kraft Paper and Paper Board)

iii. N R Agarwal Industries Ltd. (Writing & Printing, Duplex Board)

iv. Astron Paper & Board Mill Ltd. ( Kraft Paper)

v. Shree Ajit Pulp and Paper Mill Ltd. ( Kraft Paper)

vi. Genus Paper & Boards Ltd. (Kraft Paper)

3. Agri Residue

i. Tamil Nadu Newsprint & Paper Ltd. (Paper & Paper Board)

ii. Ruchira Papers Ltd. (Kraft Paper & Writing & Printing Paper)

iii. Kuantum Papers Ltd. (Writing & Printing Paper)

iv. Yash Pakka (Speciality Packaging Products)

Please find the attached link for pdf file

Niveshaay JK Paper Research Report

Outlook Interpretation

- Positive – Expected Return of 12%+ on annualized basis in the long term

- Neutral – Expected return in the range of +/- 12%

- Negative – Expected return in negative

Disclaimer: Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Disclaimers and Disclosures

SEBI Registration No. :INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607 | BASL Membership ID: 6276

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing. The securities quoted are for illustration only and are not recommendatory. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR