Elecon Engineering Ltd.

Inside the report

- What led us to research on this industry?

- Understanding the product

- Why Gear Industry can do well?

- Competitive Scenario

- Niveshaay Scuttlebutt Analysis

- Elecon Engineering Ltd

- Key Risks

- Financials

- Conclusion

Research Analyst - Gunjan Kabra (gunjankabra@niveshaay.com)

What led us to research this industry?

We did a top-down analysis at macro level and analyzed that Indian capex cycle can rebound. India’s capex cycle has been muted since last 10 years as private capex was flat. It was only the government capex that had supported infrastructure spending with 13% CAGR over FY10-20. What has changed now?

- Investment cycle has bottomed out. Investment contribution to GDP has reduced to 26.7% in FY21 from peak of 36% in FY07.

- Healthy Balance Sheet and Good Cash Flows of corporates

- Accommodative Monetary Policy: Low cost of funds & Adequate Liquidity

- High Demand from domestic as well as export markets

- Cut in corporate tax rate for new capex (15%)

- Reforms done in the past like RERA, GST etc.

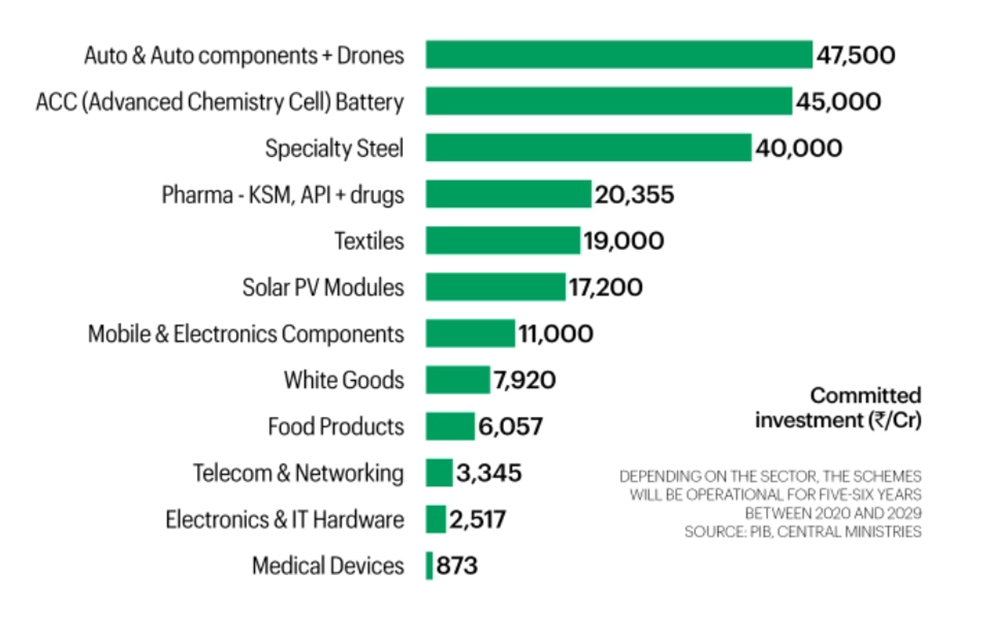

- Government initiatives to boost manufacturing activities like PLI Scheme, import substitution initiatives

- National Infrastructure Pipeline of Rs. 1.1 trillion over FY20-25 which is twice of the total spending done in FY13-19.

- China plus one strategy helping India to boost manufacturing activities

- Indian Renewable/Clean Energy in focus

Government spending is the first to revive in any capex cycle. This gives confidence to private players to make expansion. Hence, we see an upsurge in capital expenditure. Order Flows for capital goods companies are growing. For instance, Thermax Limited is engaged in the business of manufacture and sale of boilers, heating and cooling equipment, industrial chemicals, and water and waste management equipment. The following table highlights the order book trend.

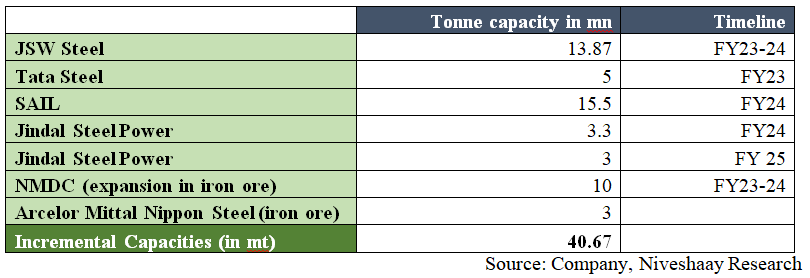

JSW Steel, for instance, plans to spend around ₹28,000 crore to expand steel-making capacity from 24.5 million tones (MT) to 36.5 MT by March 2024,

Tata Motors is investing ₹28,900 crore in subsidiary Jaguar Land Rover and hydrogen fuel cell vehicles in FY2022.

PLI Scheme will be a key driver of Private Sector Investments

Sticking to our investment style, we have chosen a company whose product is irreplaceable, plays a pivotal role in the capex cycle. Interestingly, the product looks simple and yet the industry is dominated by 2-3 players.

The sector is Gears/Gearbox industry.

Understanding the Product: Gears

What is a Gear?

An industrial gearbox is a system in which the mechanical energy is transferred from one device to another and is used to alter torque (force) and speed. It is used in conjunction with electric motor.

Types of Gear:

- Helical

- Bevel

- Worm

- Planetary

- Gear Motors

Classification of gears:

- Standard Gears: Order is chosen from standard catalogues

- Customised Gears: Lead time is higher

How is it used ?

- Combination of these gears can be used

- Usage depends on the industry served

- In worm gears, efficiency is less and priced lower too when compared to Helical and Bevel Gears. Gear Motors work in a similar way.

Can the gears be manufactured interchangeably?

- Bevel Gears require specialised machinery for production. There are companies that manufacture only Bevel Gears also.

- There is a difference in the manufacturing process and how they look. Hence, they can’t be interchangeably manufactured.

Industries Served:

Gears are used in automotive and industrial sector. Here, we’ll be discussing gears used in industrial space only.

Value Chain

Loose Gears >> Gearbox

Gearbox – Not all gear companies make gear box. It is essentially an assembly work.

Applications: End User Industry

- Sugar

- Steel

- Cement

- Renewables

- Marine

- Defence to name a few

Raw Material Used

- Aluminium

- Iron

Margin Profile

- According to industry profile, margins do change.

- Marine and defence gears command high margin

- Elecon Engineering Ltd. – High Presence in Marine Sector and also present in defence segment. The company is present in small, mid and large size gears.

- Shanthi Gears Ltd. - Present in defence and renewables segment, no presence in marine segment.

Industry Working

- Hierarchy of importance while sourcing gears

- Client Relationship

- Technical

- Pricing

- Business Order Cycle

Generally, its 3-5 months. Hence, passing on the hike in raw material prices isn’t an issue. For marine and defence, order execution takes time. Here, orders are delivered in phased manner. - Ability to pass on the margins

Since, the order cycle is short, it is easier to pass on the hike in raw material prices. In the current scenario, where steel prices have decreased, the company can improve spreads a bit in short term but in long term, it’ll pass on the decrease in prices. In export markets, the company would benefit in the decreased raw material pricing environment.

Classification of Gears

- Standard Gears (Elecon Engineering Ltd.)

There is a standard catalogue and order is given through that. It can cater to large volumes. Elecon Engineering is majorly into standard products. - Customised Gears (Shanthi Gears Ltd. )

Gears are manufactured according to client’s specific requirements. Here, lead time is high and attracts less competition.

Why, we prefer investment product this time?

Before, we go further and discuss Elecon in detail, wanted to highlight few things. In the previous two reports on RHI Magnesita and Usha Martin Ltd., we discussed whether the product is investment or a consumable to visualise the scope of growth.

As an investor, you and we at Niveshaay, would prefer consumable products. Repeat orders, short manufacturing cycle helps us to visualise scope of growth. Here, replacement cycle is very long. But as they say, always have a fresh perspective while investing to overcome previous biases. Ruling out a company should have proper reasoning. Visiting gears and grinding expo in Pune, some more dig down into the sector helped us to understand the industry composition and structure in great detail.

What made us consider this industry?

- The industry growth has remained muted since a very long time.

- Initial signs of good order book visibility

- Low-capacity utilisation in the industry prompting no new capex requirements to cater to higher demand.

- Fragmented Market but Elecon Engineering holds 35-38% market share in India and Shanthi Gears attracts limited competition as it is into customised gears.

- The quality of the product plays an important role in functioning of the machinery. These two companies are known for their quality in the industry, got this insight from various other small players exhibited at the expo. This point makes it a sticky business.

Why Gear Industry can do well ?

1. Capex in end-user industries in next 2-3 years

- Indian Steel Industry Capex Plans for the period FY23-25

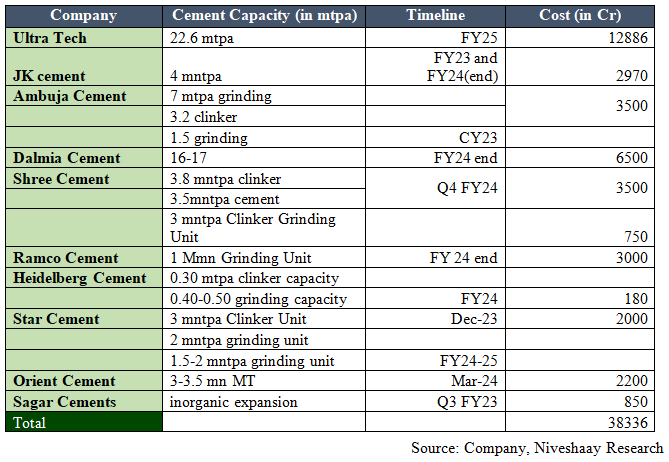

- Indian Cement Industry Capex Plans for the period FY23-25

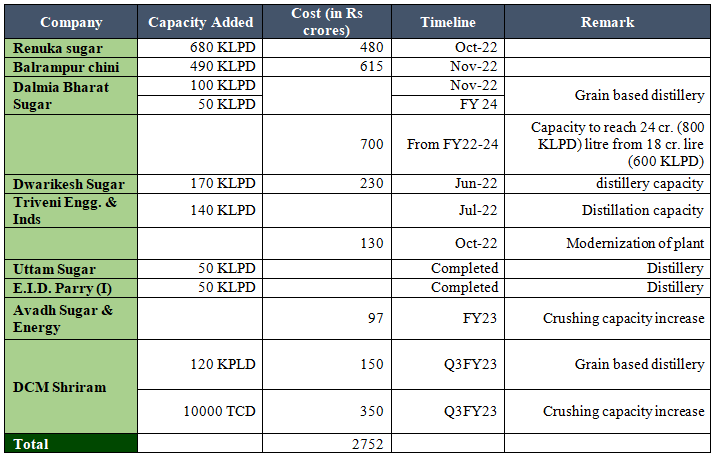

- Indian Sugar Industry Capex Plans for the period FY23-25

2. Healthy Order Book

They are witnessing healthy order book after a very long time as guided by the management.

3. Operating Leverage Play

Industry has been operating at low-capacity utilisation and both of these companies have doubled their capacities in the last decade. With any growth in the order book, company can easily ramp up their existing capacities.

4.Export Focus

Indian engineering components exports grew by 37% when compared to 2019 and grew to $ 111 billion in 2022, a rise of 50% from 2021 levels. Acceptance of any product increases when one gets an opportunity to try and experience new products. India just got that and few companies totally grabbed these favourable opportunities to provide to international as well as domestic clients. This is also happening in the case of gears business. Interestingly, Elecon’s management also highlighted in one of the conference calls that how with word of mouth and recommendations, exports for them are increasing.

Competitive Scenario

- Elecon Engineering Ltd. (38% Market Share)

- Shanthi Gears Ltd.

- Premium Transmission Pvt Ltd.

- Flender – German Brand (Mostly into big gears)

-Main competitor of Elecon Engineering Ltd.

Niveshaay Scuttlebutt Analysis:

Visit to IPTEX GRINDEX Gear and Grinding Products & Technology Expo

We recently visited this gear exhibition in Pune and gained the following insights:

- Understood the structure, manufacturing process and applications of different types of gears in great detail.

- Most importantly, different types of gears aren’t manufactured inter-changeably. For instance, Bevel Gears are manufactured using specialized machines and there are companies manufacturing only these gears. I had this question in mind, browsing at office and got it cleared by visiting this expo

3. Worm Gears are little less efficient and priced lower when compared to Helical and Bevel Gears. Geared Motors work in a similar way.

4. Interacting with various exhibitors, got quite positive feedback of gears manufactured by Elecon Engineering and Shanthi Gears.

5. Also, got an idea about the orderbook visibility. Many companies exhibited there guided about good traction in orders and enquiries.

Gear Box- Shanthi Gear Product

Elecon Engineering Ltd.

About the Company

- Products: Gears and Material Handling Division

- Revenue Mix: Gears 89% & MHE- 11%

- Gears: 60% Standard & 40% Customised, After sales service - 20-22% of the business

- Market Position: 38% market share in India in gears (Pan India Presence)

- Geographic Presence: 70% India & 30% Outside India

- Caters to diverse sectors: Steel, Cement, Sugar, Marine, Defence etc.

- Plant Location: Anand-Gujarat

- Good Presence: Marine Gearbox for Defence, Vertical Mill Gearboxes in Cement & Power, Rolling Mill Pinion Stands, and Sugar Mill Planetary Drives.

Why Elecon Engineering Ltd.?

- 38 % Market Share in India

The company has strong presence in standard gears. Here, orders are placed from catalogues by customers.

- Operating Leverage: Currently, operating at lower capacity utilisation

The company is operating at 60% capacity utilisation and can easily ramp up the capacity. With higher utilisations, margins can also improve. During the last decade, company almost doubled its capacity. As utilisation of asset increases, fixed costs will go down. Hence, it can improve EBITDA margins.

- Healthy Order Book for the year

As per the management guidelines, 20-25% is expected in FY23. Current order book stands at Rs. 605 crores in gears business and in MHE orders on hand are of Rs. 127 crores.

4. Restructuring done in MHE division, positive contribution this year onwards with improved margins Company has done away with their legacy business model (contracting). Here, expected EBITDA margins is around 15-20%.

Here, they’ve changed their strategy. Majority of the business is now, coming from after sales which is revamping or modernizing material handling plants as well as providing services and manufacturing spares and delivering to customers. These are profitable business and have healthy margins. These products have good payment terms unlike the previous model.

5.Focus on Exports

All the overseas entities have now turned profitable due to re-structuring initiatives. Interestingly, in one of the conference calls, they highlighted how acceptance of their products overseas happen when they use it once, finds out that the product is robust and reliable. This leads to repeat orders. This happened with the company in South America. With local reference, they tend to receive repeat orders. In export market, bargaining power is high. US markets prefer to buy from India and China. Europe markets prefer

local market products. Also, with lower metal prices, export products can command high margins too.

6. It aims to be net debt free by FY23.

7. It is a fantastic combination to play on a company when the following happens together:

- Volume Growth

- Margins Growth Probability

- Restructuring

- Operating Leverage Play

- Focus on to be net debt free

All these points are expected to play on Elecon Engineering Ltd.

Elecon Engineering Ltd. Conference Call Q4FY22 excerpts

- Growth guidance in gears division for FY23: 15-20%

- Margins should improve as utilization improves

- They have a o/s orderbook of Rs. 490 crores. Product cycle varies from 3-5 months. This high order-book at the beginning of the year has happened after a very long period of time.

- For, 98-99% of the orders, the company will be able to pass on the higher prices.

- Focus on exports. Overseas subsidiaries have turned profitable now.

Key Risks

- Slowdown in capex cycle

- Hike in raw material prices- They are able to pass on due to short delivery cycle.

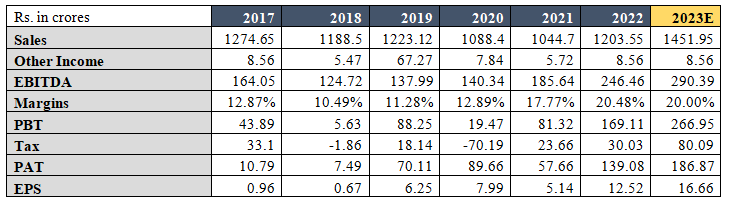

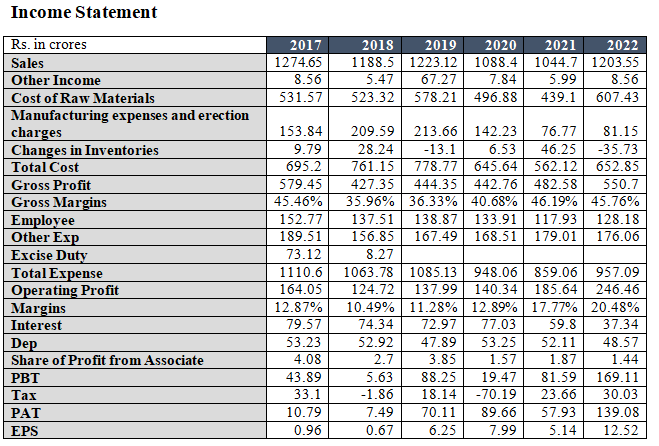

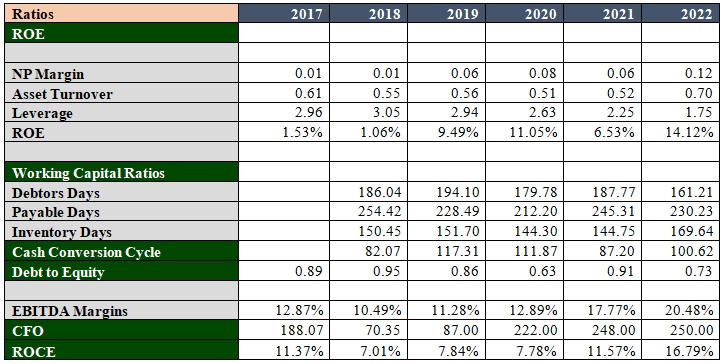

Financials

Conclusion

In the current scenario, we can classify Elecon Engineering Ltd. under a category where the company doesn’t require further investments to grow for a foreseeable future. Also, with revival in capex cycle expected, restructuring and operating leverage play, the company is expected to perform well in the coming quarters.

Disclaimer:

Niveshaay is a SEBI Registered (SEBI Registration No. INA000008552) Investment Advisory Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use. This report does not represent an investment advice or a recommendation or a solicitation to buy any securities.

Disclaimers and Disclosures

SEBI Registration No. :INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607 | BASL Membership ID: 6276

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing. The securities quoted are for illustration only and are not recommendatory. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR