E2W Industry Landscape: A Comparative Look at China and India

The global Electric Two-Wheeler (E2W) market is undergoing a transformation, driven by advances in technology, rising fuel costs, and environmental concerns. E2Ws offer an attractive solution for short-distance commuting, with lower operational costs, minimal emissions, and ease of maneuverability. The market’s expansion is further fueled by government policies and incentives focused on reducing carbon footprints and improving air quality in urban areas.

While China has already established itself as the global leader in electric two-wheelers, India is rapidly catching up, leveraging its vast population and rising middle class, combined with an increasing push for sustainable mobility.

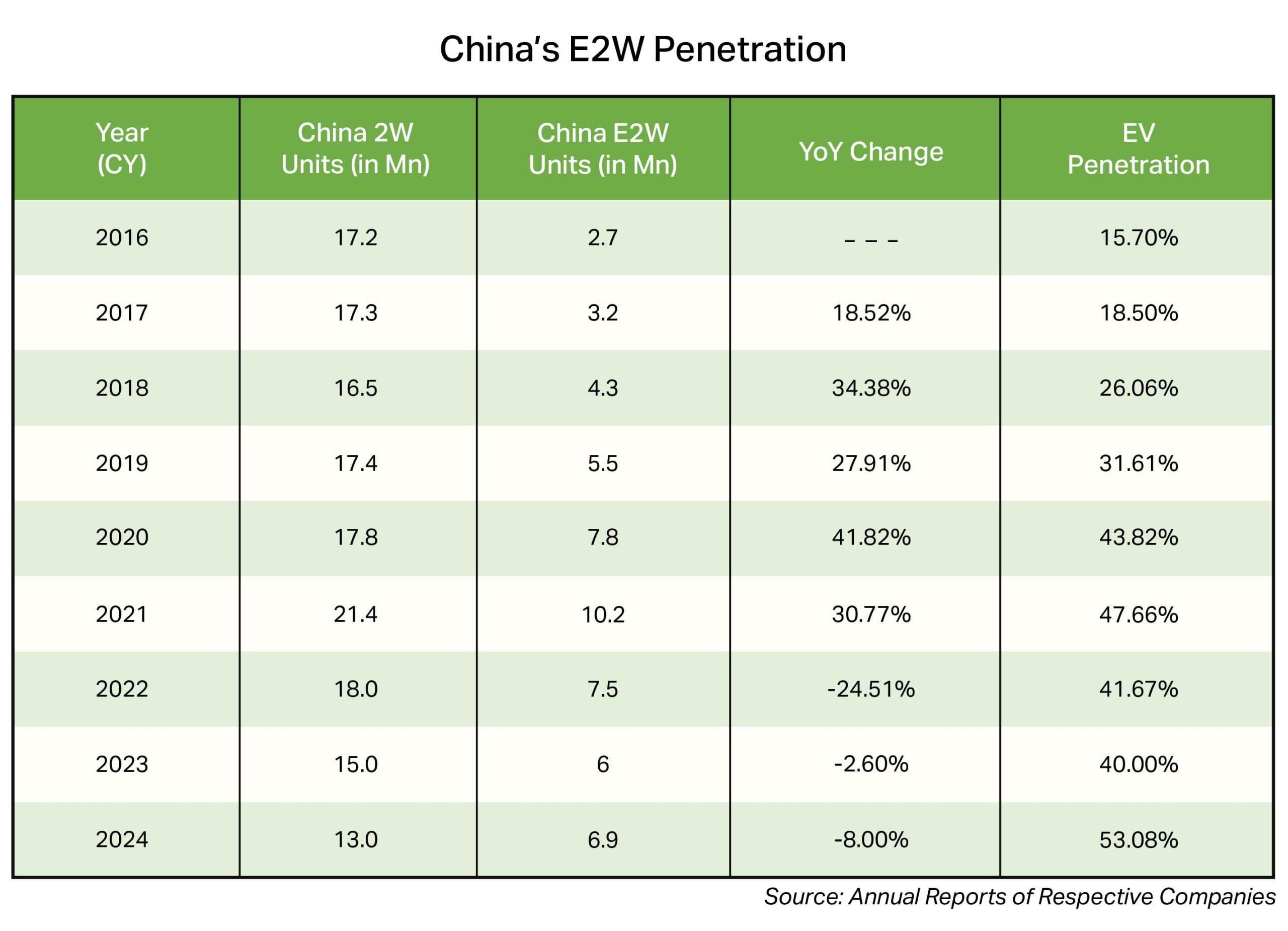

China’s E2W Penetration

China leads the global E2W market, with an estimated 78% share of the world’s total E2W sales. The country’s success in the electric two-wheeler market is underpinned by its massive production base, government incentives, and widespread adoption of lithium-ion batteries. The rise in urbanization, tightening environmental regulations, and the growing demand for efficient urban mobility options have all contributed to China’s dominance in the E2W space.

India’s E2W Landscape

India’s electric two-wheeler market is emerging rapidly, with sales growing from 28,000 units in FY19 to 1.15 million units in FY25. The country’s electric two-wheeler market penetration is expected to rise from ~5.8% in FY25 to ~25% by FY30, driven by government policy incentives, improved charging infrastructure, and the growing cost-efficiency of electric vehicles compared to internal combustion engine (ICE) vehicles.

Key Drivers for Growth:

- Government Policy & FAME-II Scheme: The Indian government’s FAME-II (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) scheme offers subsidies on E2Ws, making them more affordable and attractive for consumers.

- Cost of Ownership: The total cost of ownership (TCO) for E2Ws is significantly lower than ICE vehicles, with an average operational cost of ₹0.09 per km, compared to ₹1.68 per km for petrol vehicles.

- Rising Fuel Costs & Environmental Concerns: The increasing cost of petrol and diesel is driving consumers to explore electric alternatives, while concerns about pollution in major cities also fuel demand for cleaner solutions.

Technology Backbone: Batteries, Chemistry Evolution & India’s Emerging Battery Ecosystem

At the heart of the E2W transition lies the battery, the single most important component that defines performance, cost, range, safety, and consumer confidence. Over the last 24 months, the industry has seen meaningful shifts in battery chemistry, manufacturing localisation, supply chain stability, and charging infrastructure—all of which are structurally accelerating adoption.

1) Battery Cost Reduction is the Biggest Driver of EV Adoption

Batteries comprise 35–40% of the cost of a two-wheeler EV. As battery prices fall globally and chemistries stabilise, OEMs (Original Equipment Manufacturers) can now build high-speed EVs at price points closer to ICE scooters.

Trends that matter are:

a) Sharp decline in global cell prices: Global lithium prices have corrected sharply since late 2023 due to higher supply from Australia, China & Africa. This has brought down cell prices from $135–140/kWh to $95–105/kWh, enabling OEMs to launch mid-range EVs in the ₹90,000–1,20,000 bracket—an important psychological threshold for Indian consumers.

b) Shift from NMC to LFP chemistry: India has begun transitioning from Nickel-Manganese-Cobalt (NMC) batteries to Lithium Iron Phosphate (LFP) for the mass-market segment.

- LFP batteries are safer, cheaper, and more thermally stable, which reduces fire risks.

- They are also more resistant to degradation, giving longer lifecycle.

- Although LFP has lower energy density (slightly lower range), the Indian use-case—shorter, high-frequency trips—matches perfectly with LFP characteristics.

The combination of lower cost + higher safety is removing the biggest buying hesitation for Indian consumers.

2) Technology Stability is Rebuilding Trust in EVs

The initial EV wave (2019–2022) was plagued with battery overheating, BMS issues, software failures, and inconsistent range. Over the last year:

- New BMS architectures have dramatically improved accuracy of range estimation.

- Thermal runaway incidents have materially reduced post the shift to LFP.

- Motor/controller architecture has stabilised (hub motor → mid-drive for premium, hub for cost-efficient segments).

- Software stacks are more stable, with OTA updates fixing issues faster.

Consumers are more confident buying EVs than two years ago. Technology stability is now a tailwind, not a barrier.

3) India’s Battery Ecosystem is Gradually Being Built: India has long depended on imported battery cells (mainly from China & Korea), this is now changing.

a) Cell manufacturing investments in India:

- Ola Electric, Exide, Amara Raja under PLI have begun laying the foundation for full-scale cell manufacturing.

- Ola has begun captive LFP cell production, early-stage but important strategically.

- Amara Raja are pushing indigenised LFP and fast-charging chemistries.

Within 3–5 years, India will have meaningful local capacity, reducing dependence on China.

b) Localisation of battery pack assembly:

Almost every major OEM (Ather, Ola, TVS, Bajaj, Hero) is now Assembling battery packs locally, Designing their own BMS and Signing long-term supply partnerships with cell supplier. This is improving unit economics and giving OEMs tighter control over quality.

The overall ecosystem is shifting from import + assembly to local design + partial localisation, and will move toward full-scale localisation in the next decade.

4) Charging Infrastructure Is Improving, Though Still Behind China

Charging remains a bottleneck, but India is progressing:

- Ola Hypercharger, Ather Grid, Hero Vida and TVS have begun scaling networks.

- More offices, housing societies, and malls are installing chargers.

- Slow-speed and mid-speed EVs succeed even with home charging, reducing dependence on public networks.

China remains the global benchmark, with dense, ultra-fast charging networks, but India is closing the gap faster than expected.

Why All This Matters: Faster Adoption Curve

The convergence of all the above factors – lower battery cost + more stable technology + emerging local ecosystem + improving charging infra is accelerating the adoption of electric two-wheelers.

This is particularly visible in mid-speed EVs around ₹1 lakh, where:

- Battery cost reduction makes pricing competitive

- LFP chemistry gives safety confidence

- Reliability improvements reduce consumer anxiety

- Local pack design and service readiness improve uptime

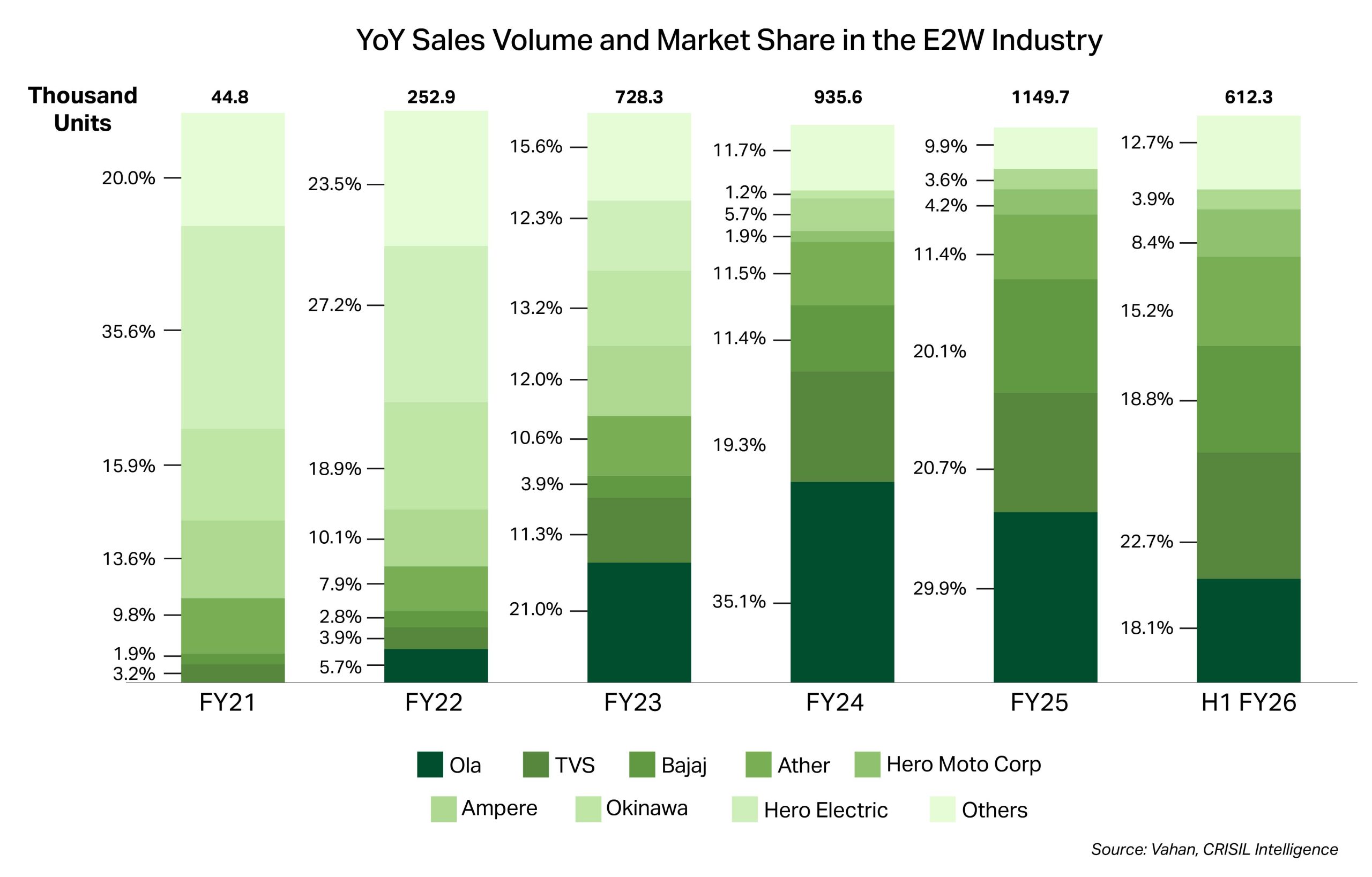

Competitive Landscape & Key Players

The Indian E2W market is competitive, with new players and established automotive giants investing heavily to capture market share. Key players in the Indian market include:

- Ola Electric, the largest player in India, with plans to scale its production to 10 million units annually.

- Ather Energy, which has carved out a strong niche in the premium segment with its 450 series and Rizta series scooters.

- TVS Motors and Bajaj Auto, which have launched electric versions of their traditional ICE models, like the TVS iQube and Bajaj Chetak.

India vs China: A Comparative Perspective

While China’s E2W market is mature, India is on a similar trajectory. India’s rapid urbanization, growing middle class, and strong government support make it an attractive market for E2Ws, particularly as consumer demand for clean, affordable mobility solutions continues to rise.

- Market Size & Growth: China’s E2W market has been stable, but India’s E2W penetration is expected to rise dramatically from 5.8% in FY25 to ~25% by FY30. In comparison, China’s market penetration stood at 31.6% in CY2019 as opposed to 53% in CY2024.

- Government Policies: Both China and India have adopted similar policy-driven approaches to encourage the adoption of electric vehicles. In China, government incentives, including subsidies and battery safety regulations, have driven rapid growth. India has followed suit with FAME-II and PLI schemes aimed at boosting local manufacturing and EV adoption.

Conclusion

The E2W market in India is poised for significant growth, with rising government incentives, falling costs, and improving infrastructure. While China continues to dominate the E2W sector, India’s fast-evolving market and rapid adoption offer a promising future for investors. As Ola Electric, Ather Energy, and other key players scale their operations, the Indian E2W market could mirror the success seen in China, making it a high-potential market for electric mobility in the coming years.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR