Decoding the Indian Aerospace & Defence Supercycle - Part 2

How global supply-chain fractures, geopolitical realignment, and India's policy pivot are creating a multi-decade opportunity in Aerospace, Defence & Space.

Indian Defence: The cycle is now multi-trigger and self-reinforcing

Modern Warfare Has Changed – Permanently

The character of war is shifting toward drones, electronic warfare, precision strikes, and massive ammunition consumption.

Six Global Conflict Patterns

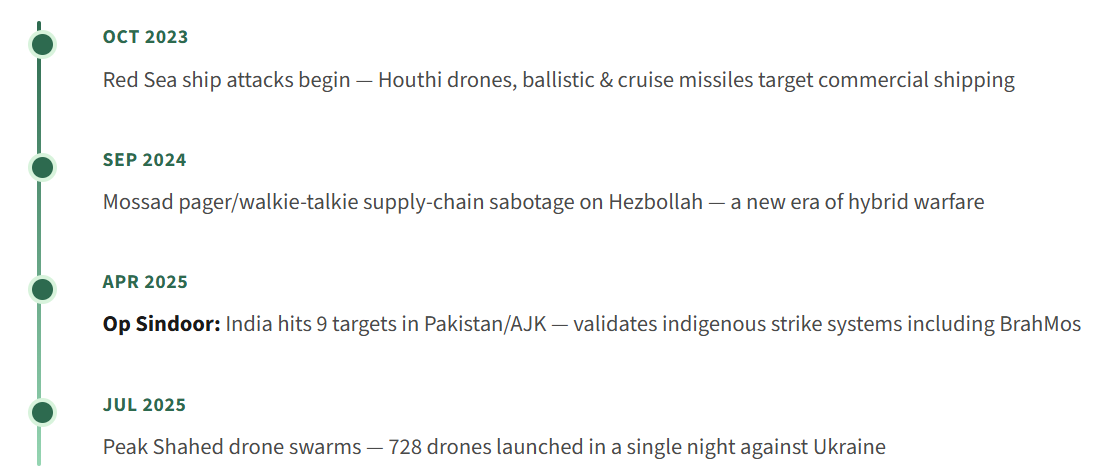

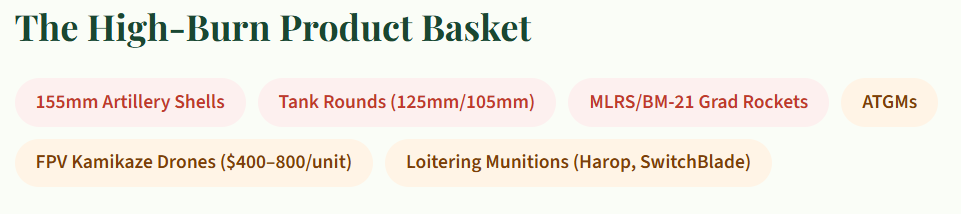

1) Attrition Warfare: 10,000–20,000 shells/day in Russia-Ukraine. Wars wildly exceed initial reserve estimates.

2) Drone Swarm Warfare: 143 Shahed drones/day avg. Ukraine FPV drones destroy tanks at just $400–800 per unit.

3) Saturation Missile Attacks: Iran-Israel exchanges. Red Sea Houthi attacks with ballistic & cruise missiles.

4) Hybrid Warfare: Baltic Sea cable cuts, GPS jamming, supply-chain infiltration, electronic warfare dominance.

5) Autonomous Warfare: AI-guided loitering munitions. Semi-autonomous drone swarms. Armenia-Azerbaijan as proof-of-concept.

6) Grey Zone Strikes: China-Taiwan drone incursions, naval harassment. Op Sindoor: India’s precision multi-target strikes.

The future battlefield is decided not by who has the strongest weapons, but who can defend and strike smarter, at sustainable cost. A $400 FPV drone destroying a multi-million dollar tank changes the math completely.

What Does a Country Look for in Defence?

Modern defence is built on three pillars — and the balance between them defines a nation’s survivability.

Pillar 1: Asymmetric Cost Advantage

Deployment of low-cost drones against high-value, expensive targets. Counter-UAS (C-UAS) systems that are cheaper than standard interceptors. Utilisation of jammers, directed-energy weapons, decoys, spoofing, and electronic warfare. Building layered interception architectures that don’t bankrupt the defender.

Pillar 2: Defending Capabilities

Advanced air defence and counter-drone / C-UAS systems. Electronic warfare (EW) shielding against GPS jamming and communications disruption. Next-generation radar and early warning arrays. Hardened, disruption-proof communication networks that survive first-strike scenarios.

Pillar 3: Offensive Capabilities

Missiles and guided munitions with precision strike capability. Armed drones and loitering munitions for persistent surveillance-strike. Artillery and heavy rocket systems (Pinaka, MLRS). Long-range strike systems, anti-ship weapons, and stand-off platforms that keep the enemy at distance.

⚠️ The cost equation has permanently changed. Maintaining a sustainable cost structure — where defensive interceptors do not vastly outprice incoming threats — is now paramount to long-term survival. Israel’s Iron Dome fires $1–4M interceptors at $20K drones. That math doesn’t scale. Nations need layered, cost-efficient defence architectures — and this is exactly what India’s indigenous industry is building.

Global Defence Spending: A Structural Upcycle

The world is transitioning from a decades-long peace dividend into a sustained rearmament super-cycle.

Growth is aggressively compounding — the 3-year trailing CAGR is more than double the 15-year average. And NATO’s Hague Summit (June 2025) mandated 5% of GDP on defence by 2035 — up from the old 2% target.

📌 The EU’s €800 Bn defence plan requires non-US suppliers (78% is currently procured outside the EU). This perfectly positions India’s ₹500 Bn export target for FY30.

India Defence Demand: Four Structural Pillars

India’s medium-term defence capex CAGR of 17–18% is secured by four distinct, non-overlapping growth engines.

1) Export Opportunity

- NATO 5% GDP mandate; 40+ nations raised budgets >10%

- BrahMos validated by Op Sindoor — 8+ nations evaluating

- 30–50% cheaper vs. Western peers

- India’s neutral geo-position — trusted by Gulf & ASEAN

2) War Wastage Reserve (WWR)

- 10k+ shells & 3k+ FPV drones consumed daily in active wars

- Post-Ukraine NATO restocking demand

- Sovereign production is critical — no imports during wartime

- Emergency FTP: 5,000–10,000 FPV drones post-Op Sindoor

3) New Procurement

- LCA Tejas Mk1A: ₹1,081 Bn & Mk2: ₹720 Bn

- MRFA 114 jets: ~₹1,600 Bn & 26 Rafale-M: IGA signed

- P-75I Submarines: ₹700 Bn | FRCV: ~₹500 Bn

- QRSAM 3 regts: ₹300 Bn | Nag Mk2: ₹790 Bn

4) Existing Modernisation

- Super Sukhoi: 200 Su-30MKI → 4.5-gen (₹600–700 Bn)

- Mirage-2000 MLU (USD 2.4 Bn) & T-90 upgrades (₹540 Bn)

- IAF modernising to bridge 31 vs 42 squadron gap

- Mi-17 EW Suites & Jaguar Darin-III AESA radar

FY27 Budget: ₹7.84T | Capital Procurement: ₹2.19T | FY30 Export Target: ₹500 Bn

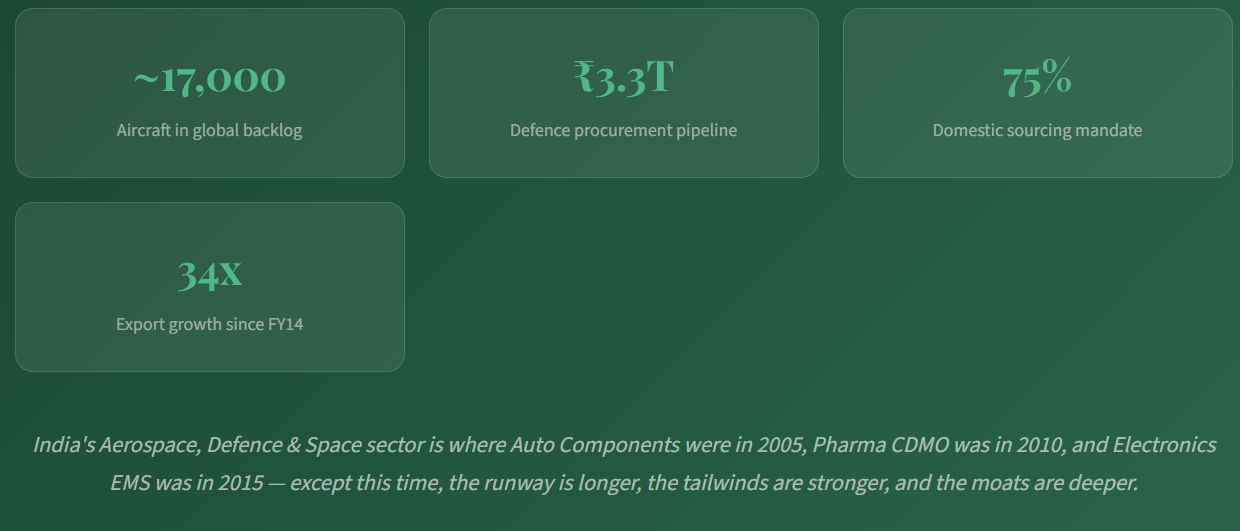

Exports have grown 15x to ₹236 Bn since FY17, evolving from an afterthought to a core revenue pillar. A massive ₹3.3 Trn procurement pipeline is actively flowing to domestic suppliers.

High Burn-Rate Warfare – Why War Wastage Reserves Are Existential

Modern conflicts consume ammunition at rates that obliterate peacetime reserve assumptions.

Evidence from Modern Wars

NATO stockpiles are fully exhausted after three years of supplying Ukraine. Israel fired 1,000+ Iron Dome interceptors in a single barrage. Total shells fired in Ukraine over 3 years are estimated at 10+ million. Red Sea economics expose the cost asymmetry — USD $1–4M interceptors fired at USD $20K drones. Drone factories are now being built mid-war because pre-war production capacity was never designed for this burn rate.

Implications for India

No Import During Wartime: WWR must be entirely domestic. You cannot rely on foreign supply chains during active conflict — sovereign production is a structural moat.

Scale of Capital Committed: ₹7.84T FY27 budget with ₹2.19T capital expenditure backing a ₹3.3 Trn procurement pipeline. The money is allocated and flowing.

Emergency Fast-Track (FTP): Post-Op Sindoor, India initiated emergency procurement of 5,000–10,000 FPV drones. This validates that the military establishment now treats high-burn items as urgent.

⚠️ Modern conflicts have turned episodic defence procurement into continuous, recurring inventory replenishment. Exhausted Western stockpiles prove that wartime imports are unviable — making domestic manufacturing a critical national security imperative, not just an industrial policy preference.

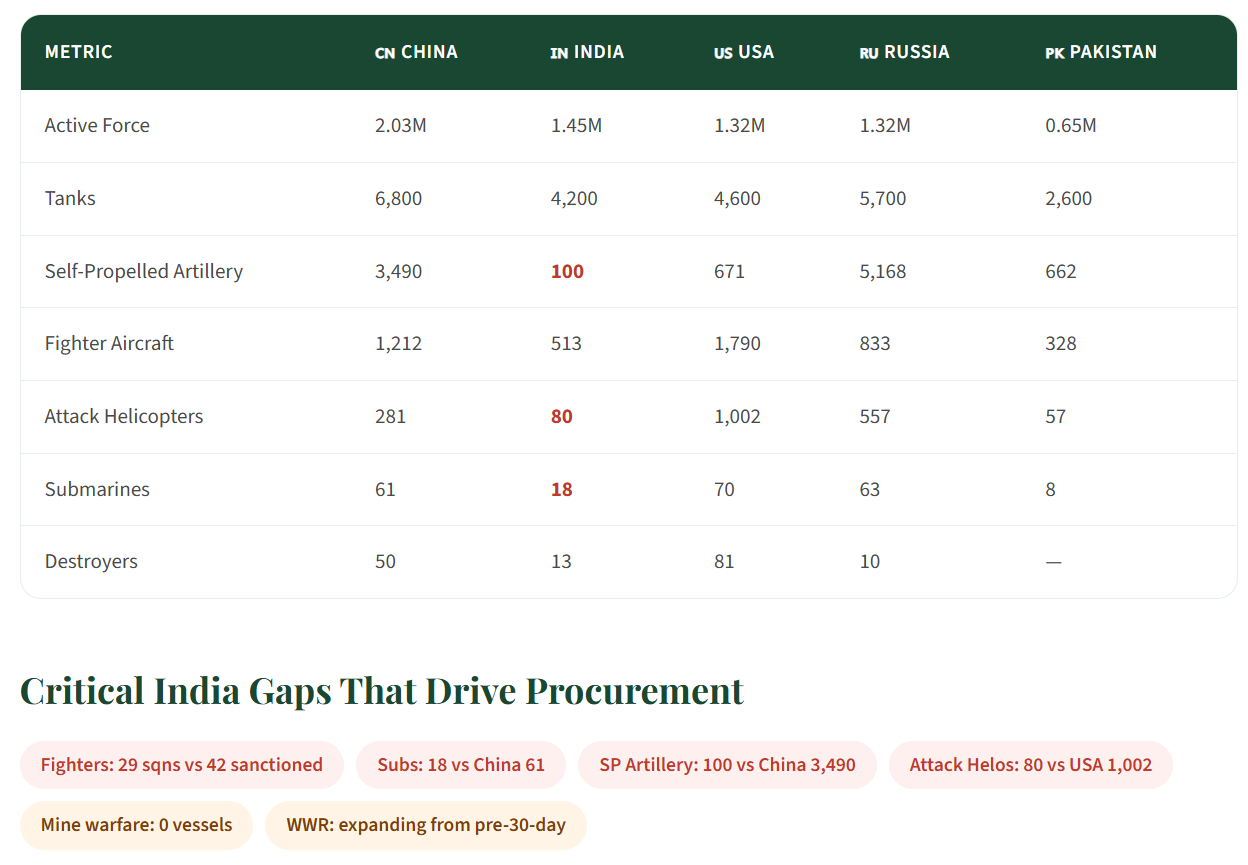

India vs. Global Military Powers — The Gaps

Addressing the two-front vulnerability against China and Pakistan is the primary driver for accelerating indigenous procurement.

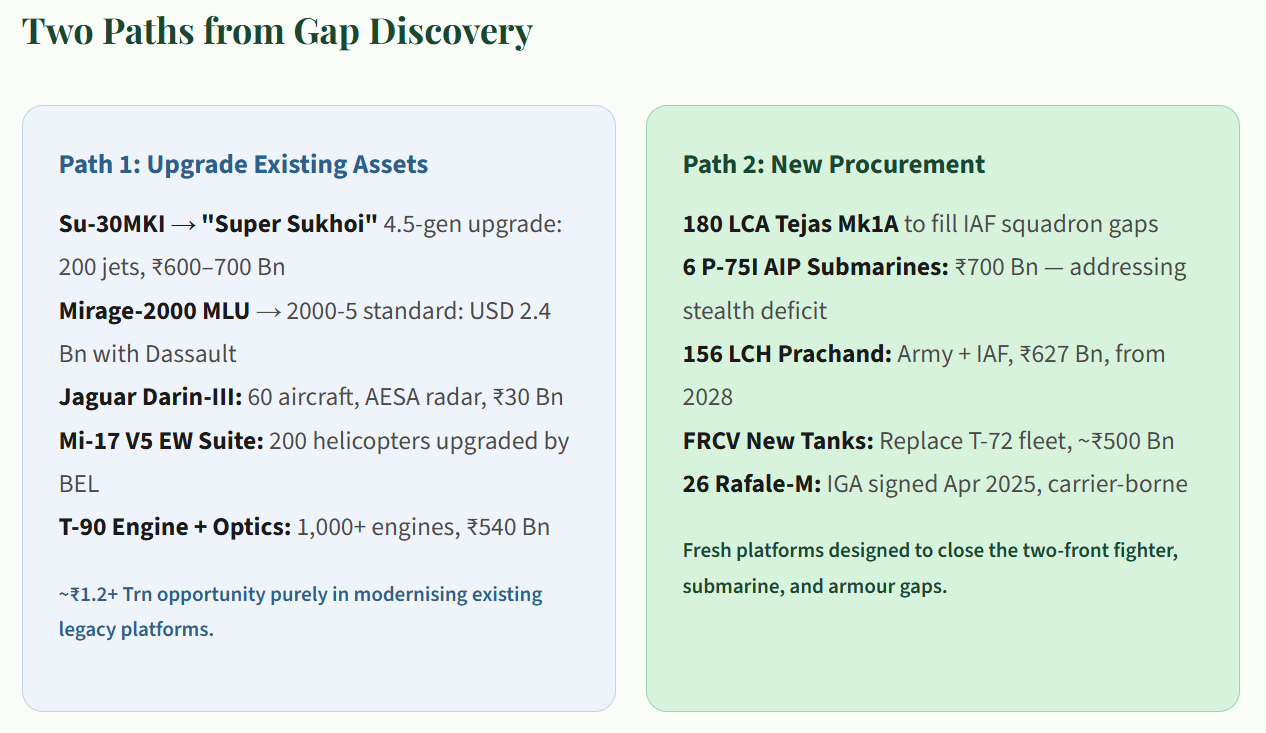

Exercise-Led Demand — Gap Discovery to Procurement

Extensive multi-theatre exercises directly expose operational gaps, triggering fast-tracked capital allocation.

India doesn’t just plan defence procurement in boardrooms — it stress-tests its military in large-scale exercises, discovers what’s missing, and then procures urgently. In FY24–25, a series of landmark exercises across all three services and multi-nation formats systematically mapped India’s capability shortfalls and accelerated procurement decisions.

The Trigger: Joint Exercises FY24–25

Gagan Shakti 24: IAF multi-theatre air exercise — tested two-front readiness, identified squadron deficit severity

TROPEX 25: Navy tri-service maritime exercise — exposed submarine and mine warfare gaps

Tarang Shakti 24: Multi-nation air exercise — benchmarked India against allied capabilities, identified interoperability needs

Malabar 24: India-US-Japan-Australia (Quad) naval exercise — tested blue-water coordination and ASW capabilities

Base Layer: Indigenous Innovation

Underneath both paths, a growing base of startup-led innovation is feeding into heavy platforms through iDEX (300+ startups, ₹5 Bn funding), ADITI (deep-tech: AI, quantum, directed energy), and DRDO MAKE I/II/III categories. This decentralised innovation pipeline ensures that India isn’t just buying systems — it’s building the IP and talent base to sustain indigenous production over decades.

India’s Import→Export Pivot: A Structural Inflection

From the world’s #2 arms importer to an emerging exporter — driven by a once-in-a-generation realignment of global supplier dynamics.

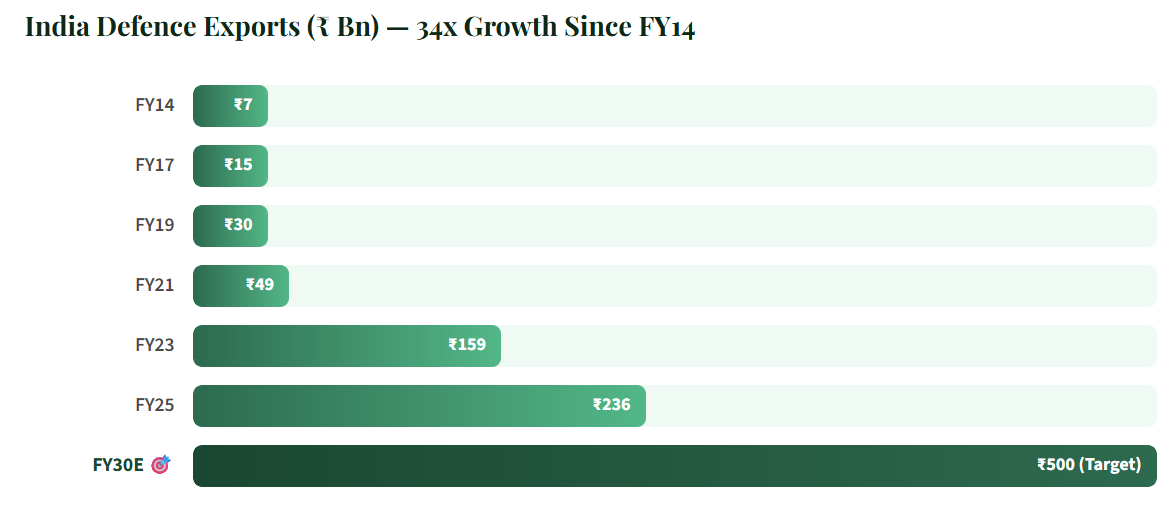

For decades, India was the world’s largest or second-largest arms importer, with 65–70% of defence equipment sourced from abroad — predominantly Russia. That dependency is now inverting. India’s defence exports have surged 34x since FY14, from ₹7 Bn in FY14 to ₹236 Bn in FY25, with a stated government target of ₹500 Bn by FY30. What makes this achievable is not just India’s growing industrial capability — it is that every traditional arms supplier is simultaneously compromised.

Why Traditional Suppliers Are Structurally Constrained

Russia — Consumed by Its Own War

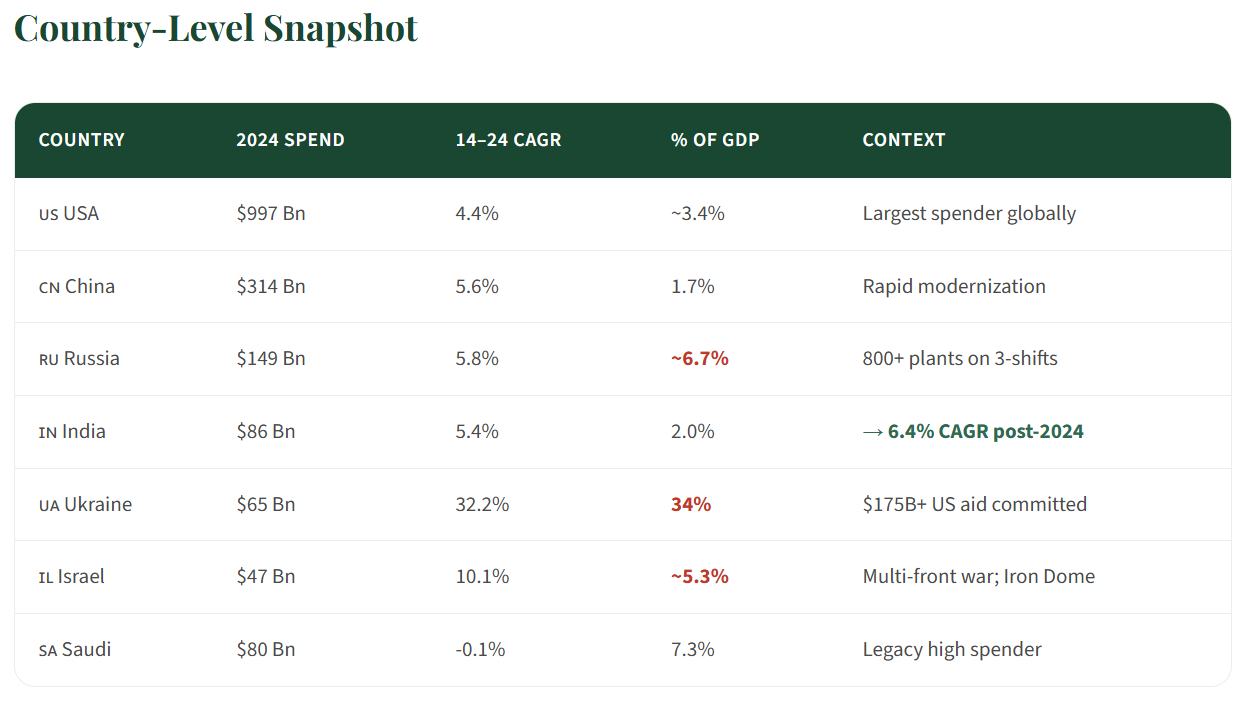

Russia historically supplied 55% of India’s defence imports. Today, it is spending ~6.7% of GDP on defence, running 800+ factories on 3-shift production just to meet domestic wartime demand. Russian defence plants cannot simultaneously feed the Ukraine frontline and fulfill multi-billion dollar export commitments. Delivery timelines have stretched, spare parts are delayed, and new order fulfilment has become unreliable. Russia’s share of Indian imports has already dropped from 55% to 36% — and this trend is structural, not temporary.

Israel — Stretched Across Multiple Fronts

Israel, a critical supplier of radars, missiles, and EW systems globally, is fighting a multi-front conflict — Gaza, Lebanon, Houthi threats from Yemen, and Iranian exchanges. At ~5.3% of GDP on defence, Israel’s industrial base is fully mobilised for its own survival needs. Iron Dome interceptors alone cost $1–4M each, and Israel has fired 1,000+ in single barrages. Export capacity for discretionary orders is materially constrained, and delivery schedules for international buyers have slipped.

USA — Effective but Conditional

American defence equipment is among the most advanced globally, but it comes with significant conditions. CAATSA sanctions risk (as seen with India’s S-400 deliberations), end-use monitoring requirements, technology denial on critical sub-systems, political conditionality on human rights and foreign policy alignment, and high acquisition costs make US procurement a complex proposition. For many nations in the Gulf, ASEAN, and Africa, these strings make American equipment a difficult choice — even when they can afford it.

🎯 The structural insight: Russia cannot deliver, Israel is stretched, and the USA comes with conditions. This creates a widening gap in global arms supply precisely when demand is surging (NATO 5% GDP mandate, 40+ nations raised budgets >10%). India — geopolitically non-aligned, cost-competitive at 30–50% lower than Western peers, and now combat-validated through Op Sindoor — sits at the centre of this gap.

India’s Unique Position in the Export Market

Geopolitical Neutrality

India is trusted by Gulf states, ASEAN nations, African countries, and even some European buyers — precisely because it does not impose political conditionality on arms sales. This is a rare and valuable positioning.

Cost-Competitive

Indian defence products are 30–50% cheaper than Western equivalents. BrahMos, Akash SAM, 155mm ammunition, and Dornier-228 aircraft offer compelling value-for-money for developing nation defence budgets.

Combat-Validated

Op Sindoor (April 2025) proved Indian systems under real combat conditions. BrahMos performed exactly as designed. 8+ nations are now actively evaluating Indian platforms — this is the most powerful sales credential in the defence industry.

EU Needs Non-US Suppliers

The EU’s €800 Bn defence plan is critical — 78% of European procurement currently comes from outside the EU. With the NATO 5% GDP mandate by 2035, Europe needs affordable, scalable supply. India fits.

The Export Surge: ₹7 Bn → ₹236 Bn → ₹500 Bn

The Import Shift — De-Risking Russia

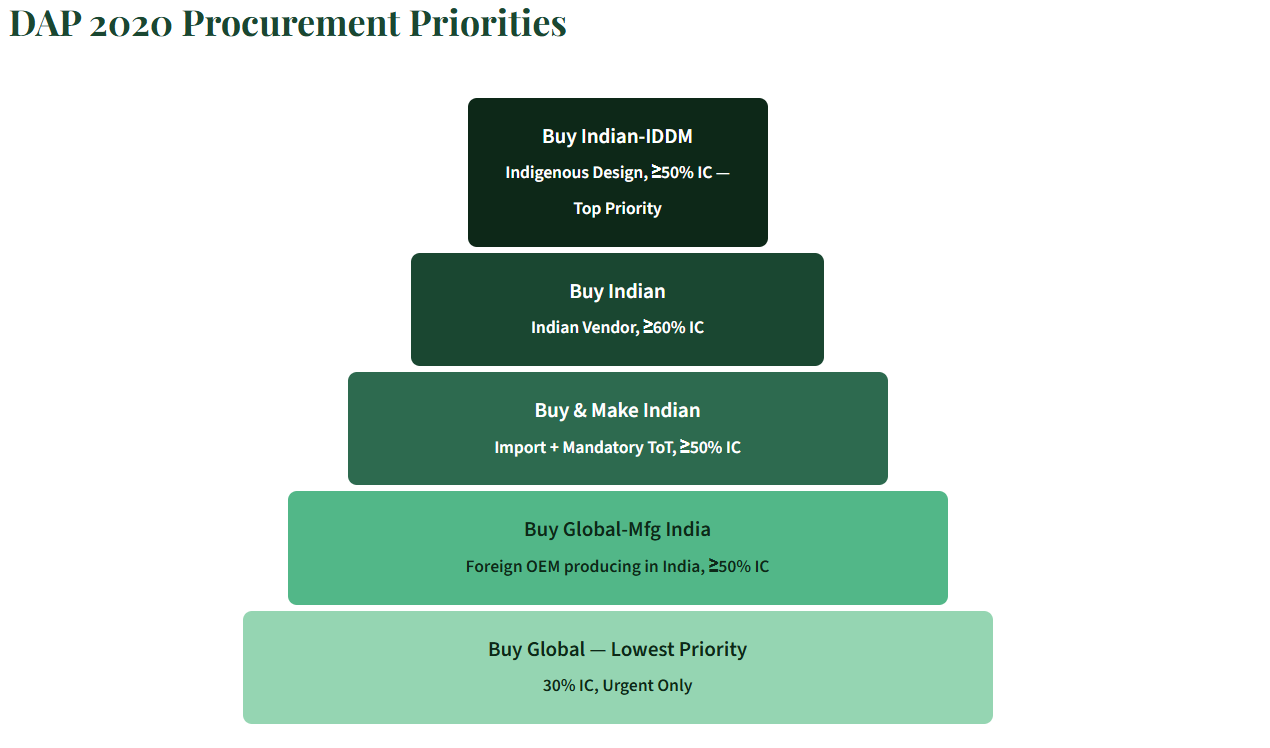

India’s import dependency has fundamentally realigned. Russia’s share has dropped from 55% to 36%, while France has risen from ~12% to 33% and the USA from ~8% to ~15%. Critically, the domestic industry now supplies ~75% of Indian military needs under DAP-2020 mandates. India remains the #2 global importer (8.3% global share), but the trajectory is clear — import substitution is accelerating, and exports are becoming a core revenue pillar.

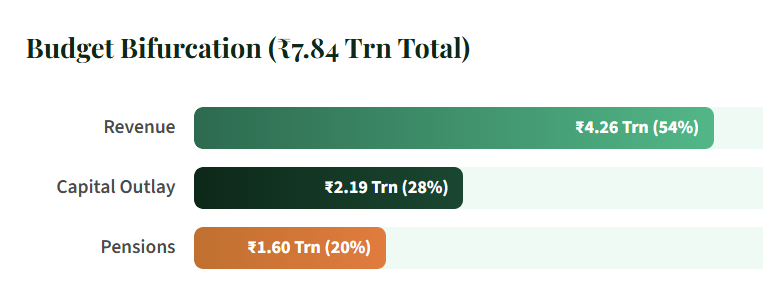

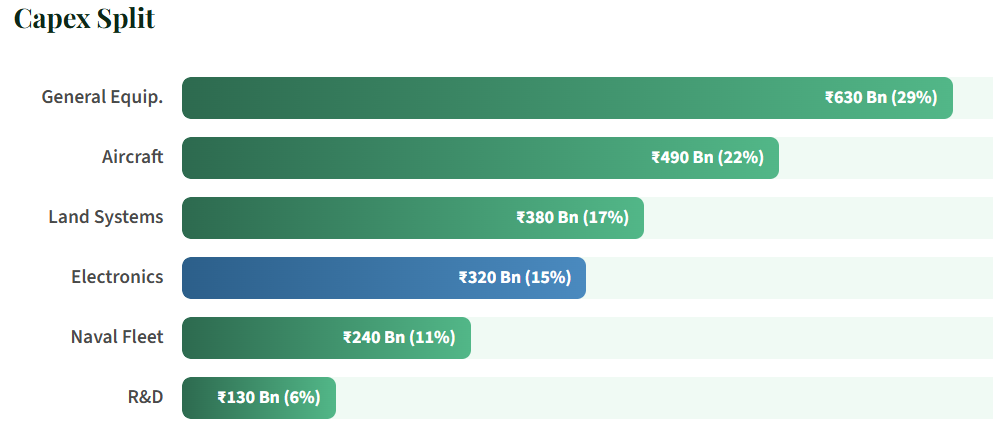

India’s Defence Budget Breakdown — FY27

₹7.84 Trn total (+15% YoY) — 14.7% of Union Budget, ~2.0% of GDP

Where the ₹2.19 Trn Capital Goes

🎯 The Air Force dominates capital allocation at 39–44%, followed by Navy (22–33%) and Army (18–31%). A strict mandate requires 75% of this capital to be sourced from domestic vendors.

25 Years of Policy Evolution: DPP 2002 → DAP 2026

From 65–70% import dependency in 2000 to 75% domestic mandate today.

Ecosystem Scale Achieved

The SRIJAN portal allows MSMEs to bid directly on 4,600+ imported items, shifting ₹75.7 Bn in DPSU orders to local vendors. Two defence corridors (UP: 6 nodes, TN: 5 nodes) have attracted ₹300+ Bn in MoUs. FDI is now allowed up to 74% via automatic route.

The Op Sindoor Effect — A Game-Changing Moment

Real-world combat validation of Indian systems has drastically shortened procurement timelines.

In April 2025, India’s Operation Sindoor struck 9 targets in Pakistan/AJK, field-proving indigenous systems like BrahMos. This single event triggered a ₹3.3 Trn AoN approval wave and unleashed fast-track procurement across drones, loitering munitions, and counter-UAS systems.

India’s Future Defence Programs — Vision 2035

A comprehensive indigenous capability build spanning air, naval, missile, space, cyber, and directed-energy domains.

India is not just buying equipment — it is building an indigenous defence-industrial ecosystem across 8 capability domains under the Atmanirbhar Bharat vision. These programs represent the next 10–15 years of capital allocation and industrial growth.

1. Air Combat Platforms

AMCA — 5th-Gen Stealth Fighter (fly 2029)

Tejas Mk2 — 4.5-Gen (fly 2026-27, ₹720 Bn)

TEDBF — Carrier-borne fighter

Ghatak UCAV — Stealth unmanned wing

MRFA 114 jets — ~₹1,600 Bn

CATS Warrior — Manned-unmanned teaming

2. Missiles & Strike Systems

ET-LDHCM & BrahMos-II — Hypersonic

Project Vishnu — HCM variants

Astra Mk-2/3 — Beyond Visual Range

Pralay / BrahMos-NG — TBM/LACM

Akash-NG / QRSAM / VSHORADS — Air Defence

3. Air Defence — Sudarshan Chakra

Mission Sudarshan Chakra — Nationwide shield

Project Kusha — Long-range SAMs

IADWS — Counter-drone / C-UAS

Akashteer / IACCS — C2 sensor fusion

Anti-Hypersonic — Next-gen interceptors

4. Naval & Submarine Programs

P-75(I) — 6 AIP submarines (₹700 Bn)

Project 76 & 77 — Indigenous SSKs/SSNs

S5-Class SSBN — Nuclear deterrent

IAC-II / IAC-III — CATOBAR carriers

USV & Torpedo — Autonomous swarms

5. Space Defence & Surveillance

SBS-III — ISR/Comms/Nav satellites

Spy Sat Network — SAR constellation

Joint Space Doctrine — DSA-led

Threat Detection / ASAT — LiDAR/BMD

6. Directed Energy & AI Weapons

Sahastra Shakti — Anti-drone laser

Project DURGA II — Multi-platform DEW

AI Kill-Web — Autonomous C2

High-Power Microwave — Anti-drone

Swarms & EW — ALFA-S, DRFM

7. Quantum & Cyber Warfare

Military Quantum Mission — Comm, Compute, Sense

QKD & Crypto — Unhackable comms

Quantum Radar / Nav — Stealth detection

Cyber Defence — AI-driven framework

Quantum Computing — Simulation/decisions

8. Engines, Comms & Enablers

AMCA Engine — Indigenous/co-development

Kaveri Dry — Ghatak engine

Scramjet Tech — Hypersonic propulsion

Netra / MTA — AEW&CS / transport

Secure Satcom — Tri-service satellites

iDEX & AIDWS — Startups / Big data / LLMs

India’s defence program landscape spans from conventional platforms (fighters, submarines) through next-gen systems (hypersonics, directed energy) to frontier technologies (quantum, AI-autonomous). The 15-year TPCR-2025 technology roadmap accelerates indigenous capabilities across all domains — this is not a single procurement cycle, but a generational industrial build.

Bringing It All Together

What makes the Indian A&D opportunity different from a typical sector cycle is the convergence of multiple independent forces — each of which alone would be significant, but together create a self-reinforcing supercycle.

On the aerospace side, the Western supply chain is structurally broken — labour shortages, financial stress across tiers, 17,000 aircraft in backlog, and 7-year lead times. China is no longer a safe outsourcing answer. India, with its deep auto-ancillary base, cost advantage, and growing OEM certifications, is absorbing this capacity shift — not as a possibility, but as an ongoing reality already visible in Boeing and Airbus supplier expansion.

On the defence side, the picture is equally compelling. Global military spending is at an all-time high of $2,653 Bn with accelerating CAGRs. Modern warfare — as seen in Ukraine, Gaza, and the Red Sea — has permanently changed the character of conflict toward high-consumption, drone-heavy, precision-strike warfare. India’s own Operation Sindoor validated indigenous systems under combat conditions, triggering a ₹3.3 Trn procurement wave. Simultaneously, the traditional global suppliers — Russia consumed by its own war, Israel stretched across multiple fronts, the USA burdened by political conditionality — have created a structural gap in global arms supply that India is uniquely positioned to fill.

Underneath all of this sits a 25-year policy evolution — from 65–70% import dependency to a 75% domestic sourcing mandate — backed by ₹7.84 Trn in FY27 budget, 16,000+ MSMEs in the ecosystem, 2,851+ items restricted from import, and 300+ iDEX startups building the next generation of defence technology. This is not a single budget cycle. This is a structural, multi-decade industrial build — and we are in the early innings.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR