Decoding the Indian Aerospace & Defence Supercycle - Part 1

How global supply-chain fractures, geopolitical realignment, and India's policy pivot are creating a multi-decade opportunity in Aerospace, Defence & Space.

The Big Picture: India’s Next Outsourcing Wave

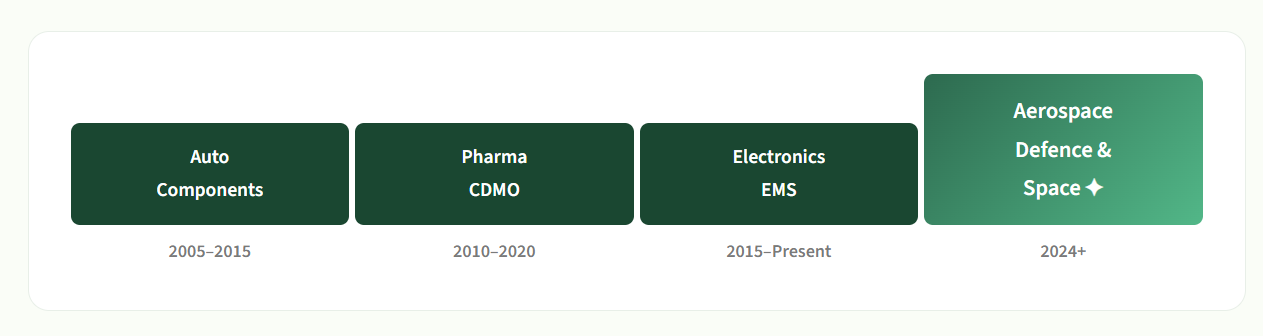

We’ve seen this pattern before — and the next wave is aerospace, defence & space.

India has a proven playbook for capturing global manufacturing share. It happened with auto components (2005–2015), then pharma CDMO (2010–2020), then electronics EMS (2015–present). The next wave – Aerospace, Defence & Space, is just beginning, and it carries the longest compounding runway of them all.

The key players riding this wave include companies like Sansera Engineering, Azad Engineering, Rossell Techsys, Dynamatic Technologies, Aequs, Sasmos, Unimech, Avalon, Avantel, JSR Dynamics, and many more. We’re in the early innings of a secular trend with long-duration compounding.

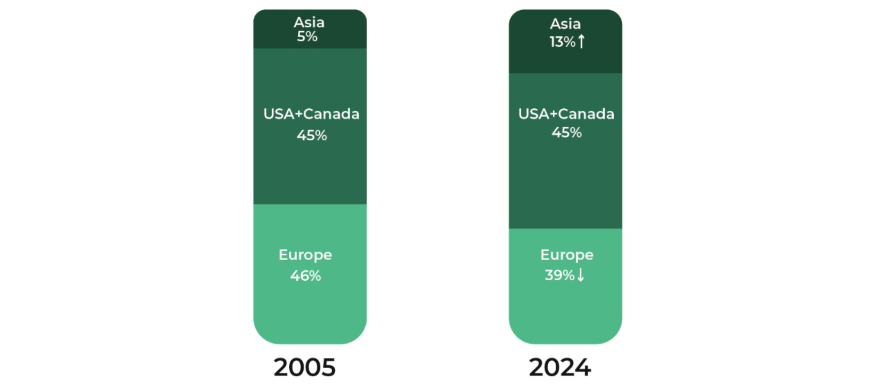

Global Manufacturing Is Shifting East

Europe has lost significant market share in aerospace exports while Asia has nearly tripled its share.

What’s Driving This Shift?

Geopolitical Mandate: OEMs are building parallel supply chains to reduce China dependence – ‘Europe+1’ and ‘China+1’ strategies are now standard.

Capex Divergence: Asian manufacturers are investing fresh capital in capacity, while European players are trapped by leveraged balance sheets and fixed-price contracts.

Operational Integration: Asia is moving up from simple assembly to faster certification learning curves and full sub-system integration.

This shift is happening across 7+ sectors simultaneously: Space, Commercial Aerospace, Defence (UFVs), Energy, Semiconductors, Industrial Panels, and Aero-Engine derivatives.

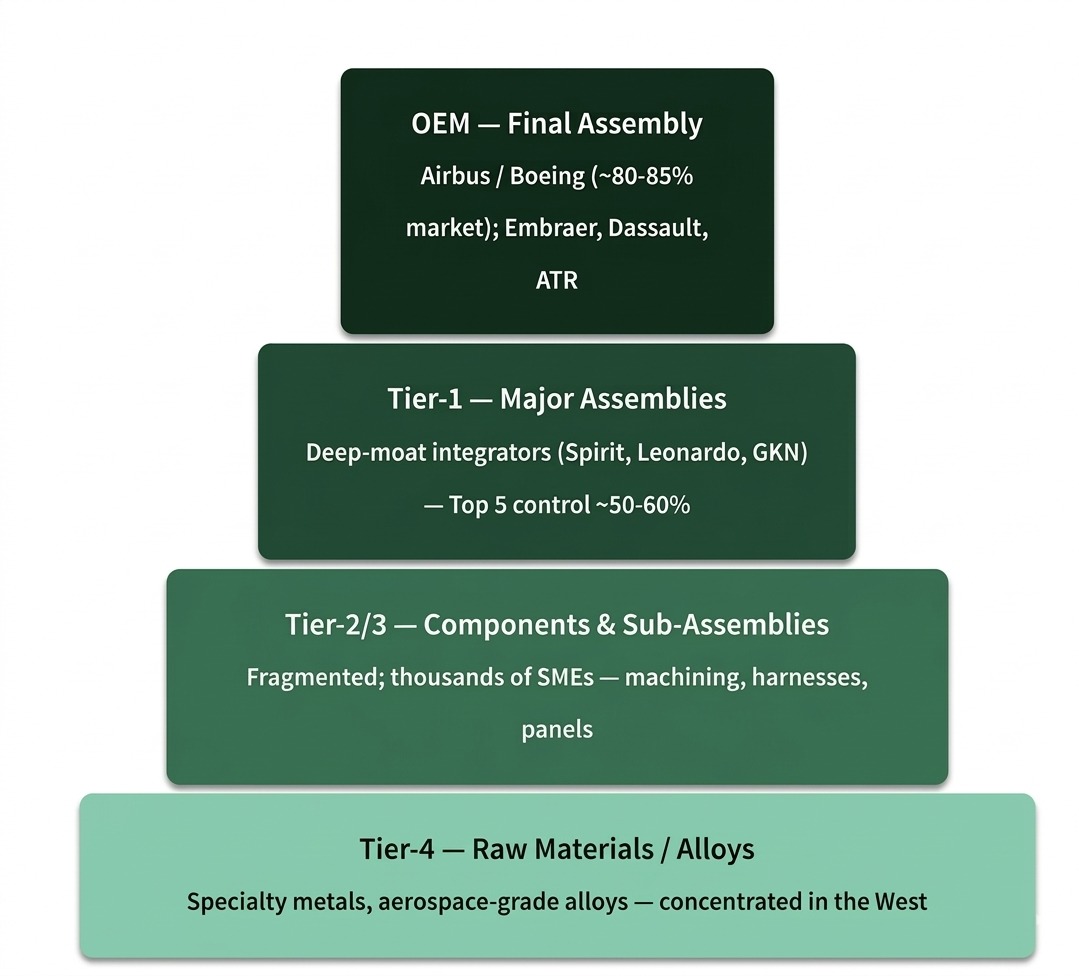

A Consolidated Top Resting on a Fragmented Base

The aerospace supply chain is a pyramid, a tight duopoly at the top, with thousands of fragmented suppliers at the base.

The global aerospace industry has an unusual structure: Airbus and Boeing control ~80–85% of the commercial aircraft market at the final assembly level – a near-duopoly. But as you move down the pyramid, the supply chain fragments dramatically. This matters because it is at the lower tiers – Tier-2/3 (components, sub-assemblies) and Tier-4 (raw materials), where India’s opportunity is most immediate and most actionable.

OEMs – The Duopoly: Airbus and Boeing dominate. Aircraft programs include A320, A350, 737 MAX, 787, E190, Falcon 7X, and ATR 72.

Engines – Tight Oligopoly: CFM International, Pratt & Whitney, and Rolls-Royce, the top 3–4 engine makers control ~90%+ of the market.

Structures – India’s Entry Point: Spirit AeroSystems, Leonardo, and GKN lead, but the top 5 control only ~50–60%. This is where Indian Tier-2/3 players can win.

🔑 Key insight: The duopoly controls final assembly, and Tier-1 integrators hold deep moats. But at Tier-2/3 and below, where the supply base is fragmented, financially stressed, and facing labour shortages, the door is wide open for qualified Indian manufacturers to step in.

The Western Vicious Cycle

Recovery collides with structural constraints, shifting gravity to the East.

Western aerospace manufacturing is stuck in a self-reinforcing trap. New aircraft deliveries get delayed → airlines fly older planes longer → maintenance (MRO) consumes scarce resources → manufacturing capacity starves further → more delays. The result? Gravity shifts East.

⚠️ Western manufacturing is structurally constrained by three forces: labour shortages, cost inflation on fixed-price contracts, and limited physical capacity with slow certifications.

What the OEMs Are Saying

Airbus (June ’25): Aircraft assembled but sitting on tarmac awaiting engines and interiors, a symptom of supplier bottlenecks and workforce issues.

Boeing (CY24–25): Supplier labour shortages, wage inflation impacting production. A strike by 3,200 machinists highlighted acute manpower crisis.

RTX / Pratt & Whitney: Skilled labor remains the primary constraint on MRO capacity expansion, human capital is the bottleneck, not capital.

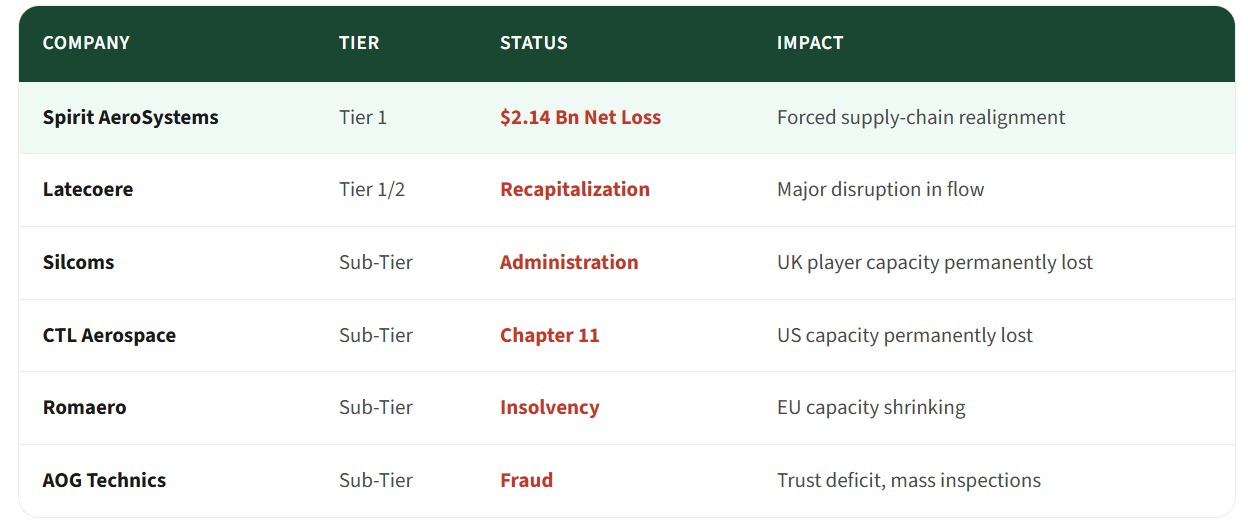

Widespread Financial Stress in the Supply Chain

Post-COVID impact has caused insolvency across Tiers 1 through 4 of the Western aerospace supply chain:

The System Is Full

Backlogs up, deliveries down, lead times longer, the global aerospace pipeline is jammed.

The backlog keeps building while throughput remains well below peak. This creates a structural, not cyclical, need for new capacity and that capacity is increasingly coming from Asia, specifically India.

Why China Is No Longer the Default Answer

How This Industry Should Be Read

Demand is not the bottleneck. Certified supply is scarce. And geography is shifting.

The aerospace investment thesis is often misunderstood. It is not a demand story, demand is abundant and growing. It is a supply-side story playing out across four dimensions simultaneously.

Demand

- Secular passenger growth fully absorbing existing fleets

- Fleet replacement cycle triggered by high maintenance and fuel costs of 15-year-old aircraft

- ~17,000 aircraft in backlog, demand is locked in for 7+ years

Capacity

- Incumbent Western suppliers hampered by legacy fixed-price contracts

- Unable to absorb inflation, capping capital available for expansion

- Margin pressure limits incremental investment in new capacity

Qualification Friction

- Stringent certification requirements create a 5-year gestation period for new suppliers

- Prevents rapid greenfield capacity additions, you cannot shortcut trust

- Companies already qualified today have a massive head start

Geography Shift

- China’s emergence as a competitor (COMAC C919) has altered OEM risk perceptions

- OEMs actively seeking politically aligned, scalable capacity alternatives

- India ticks every box: scale, cost, talent, and geopolitical alignment

🎯 The right framework: Don’t ask ‘will demand grow?’ it already has. Ask instead: ‘who has the certified capacity to deliver?’ That filter narrows the investable universe dramatically and India’s qualified suppliers sit at the centre of that answer.

The India Advantage

A unique convergence of engineering depth, cost competitiveness, and policy support.

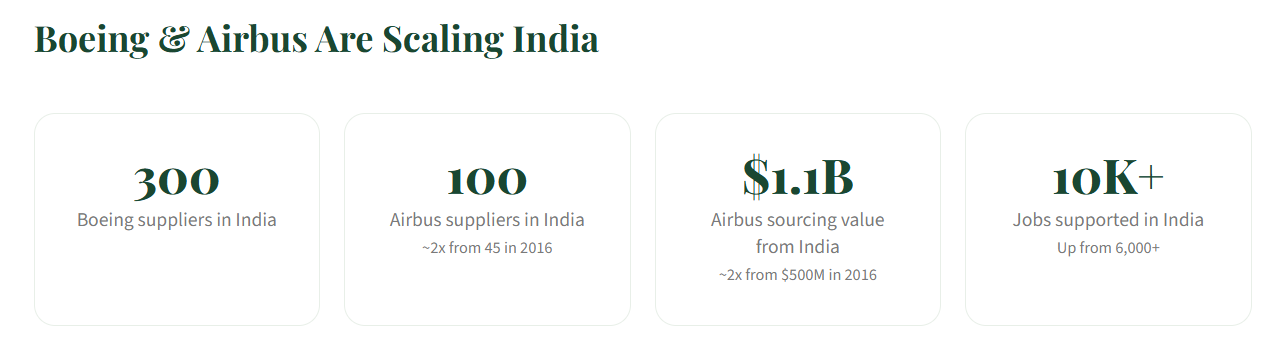

Order-Book Relevance: India represents 10–12% of the global aerospace backlog. It’s among the top 4 countries in Boeing’s order book at 7%.

Auto-Ancillary Capability: Transfer of high-precision skills from India’s massive auto components base, this is NOT greenfield capability building.

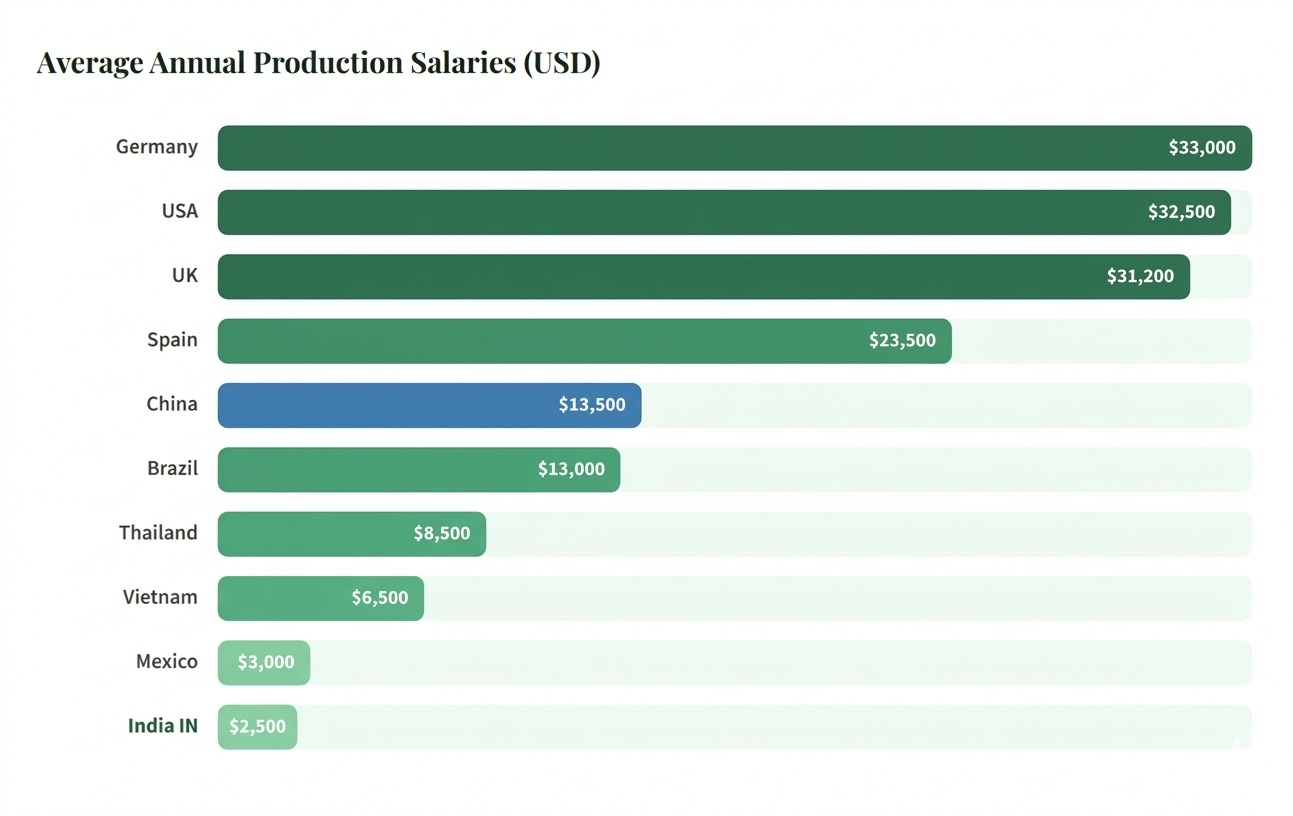

Cost-Competitive Scaling: India production wages (~$2,500/yr) are a fraction of US/EU ($30k+), delivering 30%+ savings on harness and component work.

The Salary Arbitrage Is Massive

🎯 The US median aerospace worker is >50 years old. Over 33% of skilled machinists are retiring in the next decade. Boeing recently gave a 40% wage hike. India’s young, deep engineering talent pool is the structural answer.

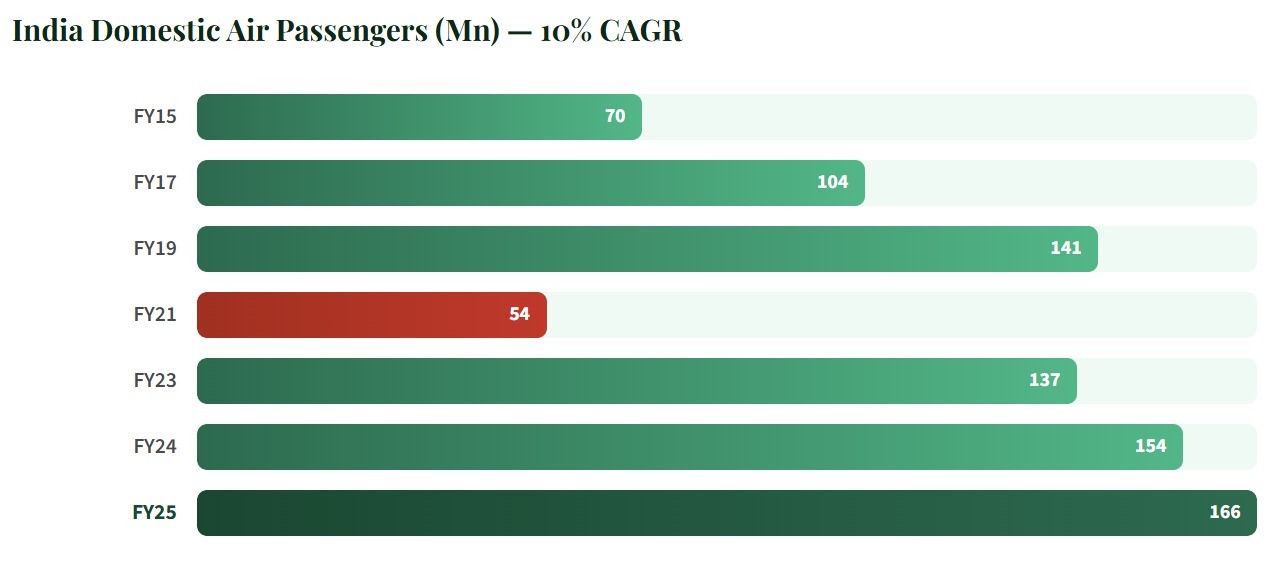

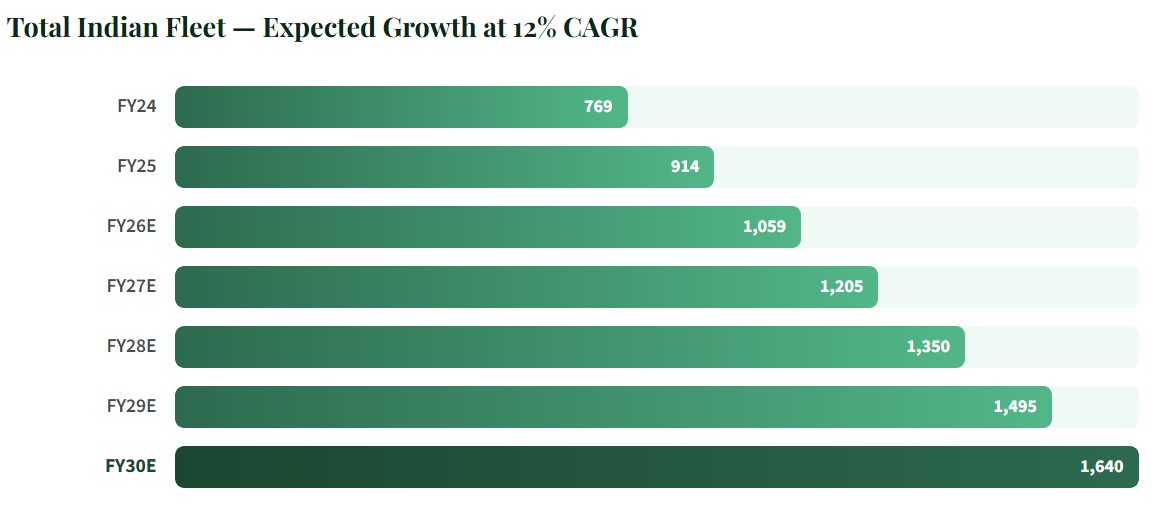

India’s Domestic Aviation Growth

India is one of the fastest-growing aviation markets in the world, with domestic passenger traffic compounding at ~10% CAGR and fleet expansion expected at ~12% CAGR over the next 5 years. This makes India a critical demand anchor for both Airbus and Boeing.

India is among the top 4 countries in Boeing’s CY25 orderbook, contributing 7% — behind only the USA (23%), UAE (8%), and Ireland (8%). Airbus gross orders from Indian carriers peaked at 750 aircraft in CY23.

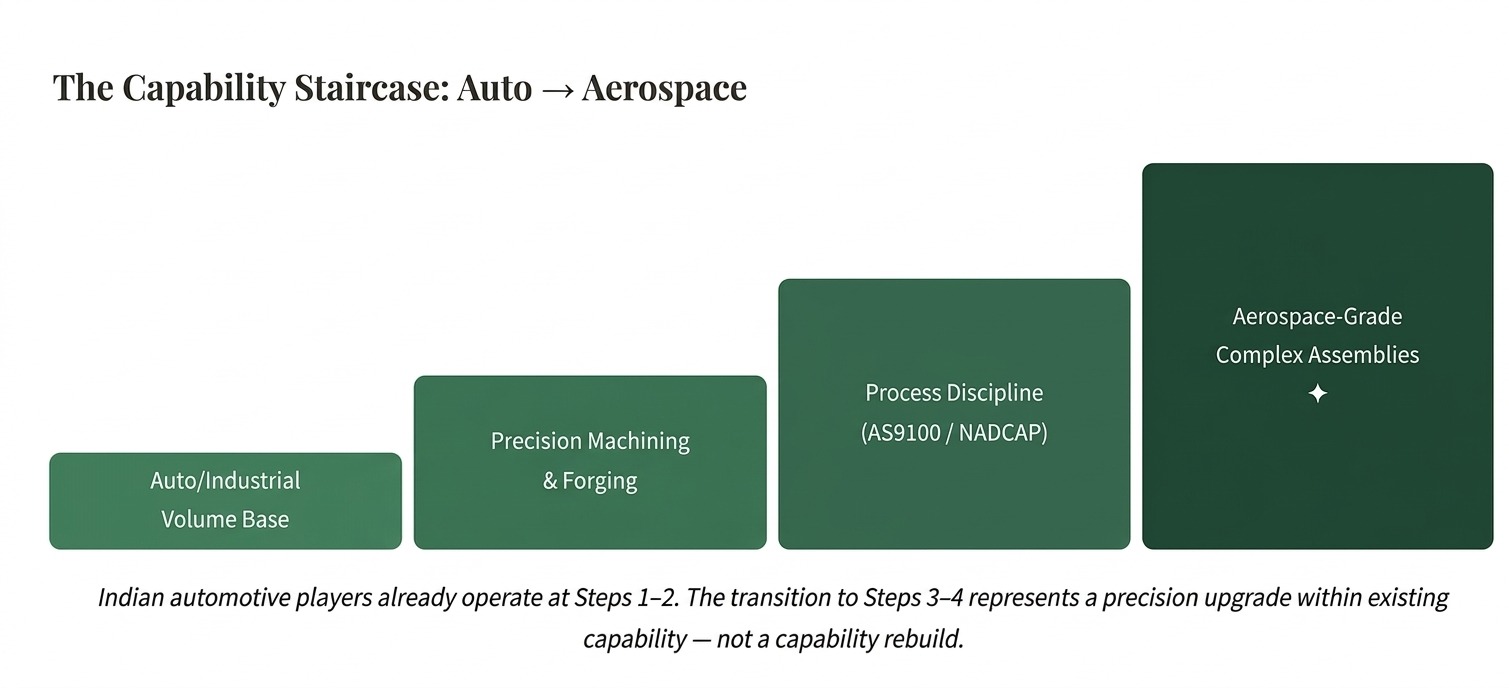

India’s Auto Base Is the Training Ground for Aerospace

High-precision automotive manufacturers carry a structural advantage in the transition to aerospace-grade production.

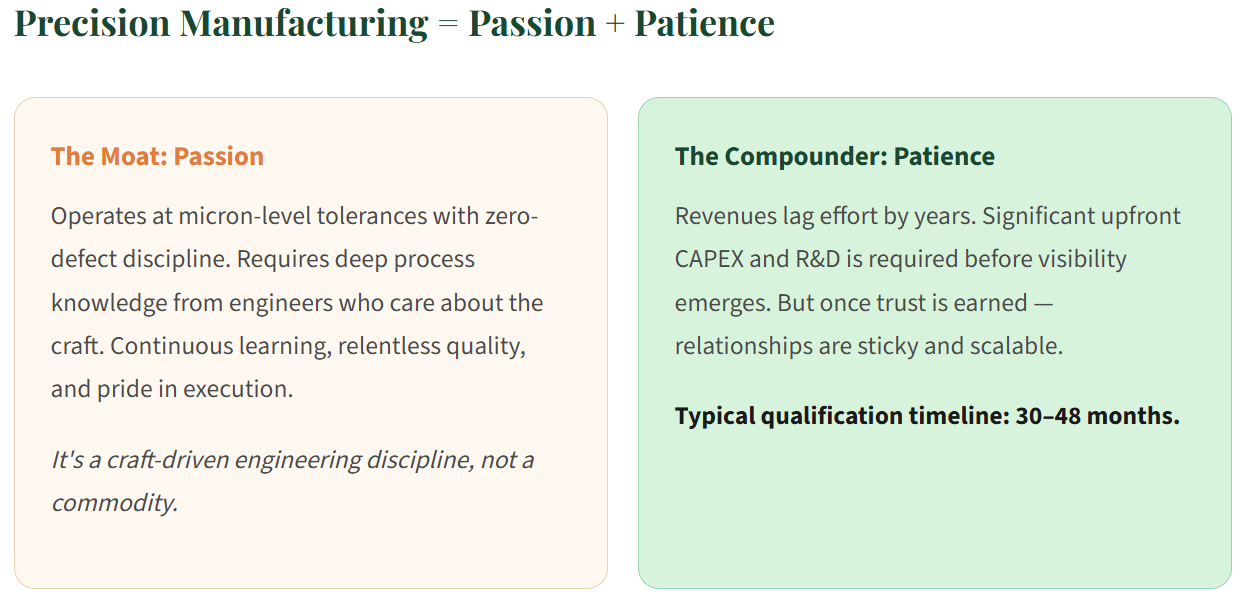

Aerospace manufacturing is among the most demanding industrial disciplines globally — it requires micron-level tolerances, zero-defect traceability, and rigorous process certifications (AS9100, NADCAP) that take years to achieve. However, Indian automotive component manufacturers who already operate at high-precision machining levels hold a distinct structural advantage in making this transition. Companies running multi-axis CNC machining, precision forging, complex surface treatment, and advanced metallurgical processes for automotive OEMs already possess the foundational capability infrastructure that aerospace supply chains demand. The step from automotive-grade precision to aerospace-grade precision is an incremental tightening of tolerances — not a fundamental reinvention of capability.

This is precisely what makes India’s position different from a greenfield entrant. Automotive machining may operate at ±25 micron tolerances; aerospace demands ±5 microns. The gap is real, but it is a calibration upgrade, not a capability rebuild. For a company that has already invested in 5-axis CNC infrastructure, precision forging lines, and disciplined shop-floor processes, the path to aerospace certification (typically 30–48 months) becomes a natural, high-value progression up the manufacturing value chain.

💡 The core thesis: Aerospace does not require a fundamentally different manufacturing DNA , it requires a higher-fidelity expression of the same DNA. Indian companies already operating precision forging, tight-tolerance CNC machining, and complex harness/wiring assembly for automotive and industrial OEMs carry a built-in advantage. Their existing shop-floor processes, quality culture, and engineering talent provide the foundation. What follows NADCAP accreditation, first-article inspections, OEM qualification cycles, is a structured 30–48 month transition, not a decade-long capability build. This is why adjacency matters: it compresses the qualification timeline and reduces execution risk significantly.

The proof is already visible across multiple Indian companies that have successfully made this transition:

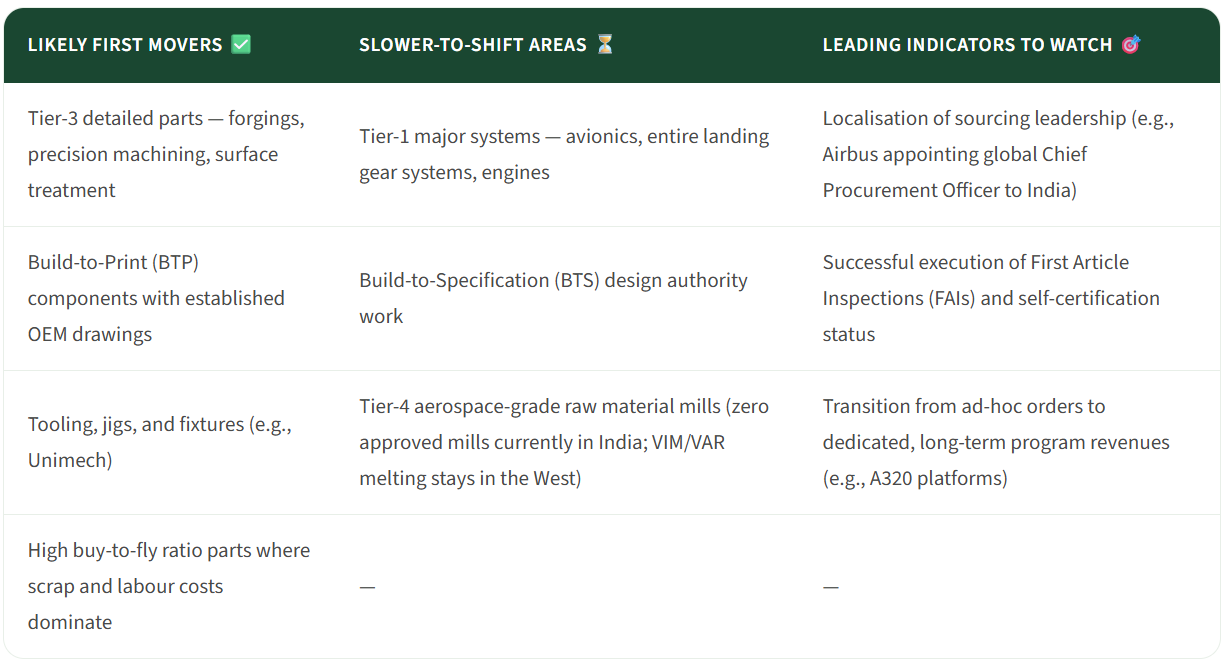

What Moves First in an Aerospace Capacity Shift

Watch procurement before headlines. Qualified suppliers benefit first. The capacity shift is gradual — not overnight.

Not all aerospace work packages shift at the same pace. Understanding what moves first versus what stays entrenched in the West is critical for identifying where value accrues earliest.

📌 Investor takeaway: The first revenue gains accrue to Indian companies that are already qualified on Tier-3 parts, BTP components, and tooling. These are the companies with existing OEM relationships and completed first-article inspections — not those still in the qualification pipeline.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR