Copper Prices May Dip, but Recycling Still Shines: Copper’s Second Act

A scrap dealer empties a gunny sack onto the floor, old phone chargers, a burnt motor, a bundle of dusty wires. It looks like junk until you remember what’s inside it. That dull reddish strand is the same metal that keeps an EV moving, a solar inverter humming, and an AI data center cool. Copper prices can swing with sentiment and cycles. But copper’s role in electrification is structural. And that’s why when primary supply takes years to respond, recycling comes into the picture; it isn’t a side story anymore. It’s turning into the main plot.

And that is exactly what this blog is trying to trace: how copper recycling is moving from the margins to the center of the value chain. As demand rises from grids, EVs, renewables, and data centers, secondary copper is becoming the fastest way to add supply without waiting a decade for new mines. The story now is not just about scrap, it is about scale, cleaner processing, policy support, and the companies building the rails for a more circular copper economy.

Copper’s Endless Appetite: Demand Signal’s a New Era

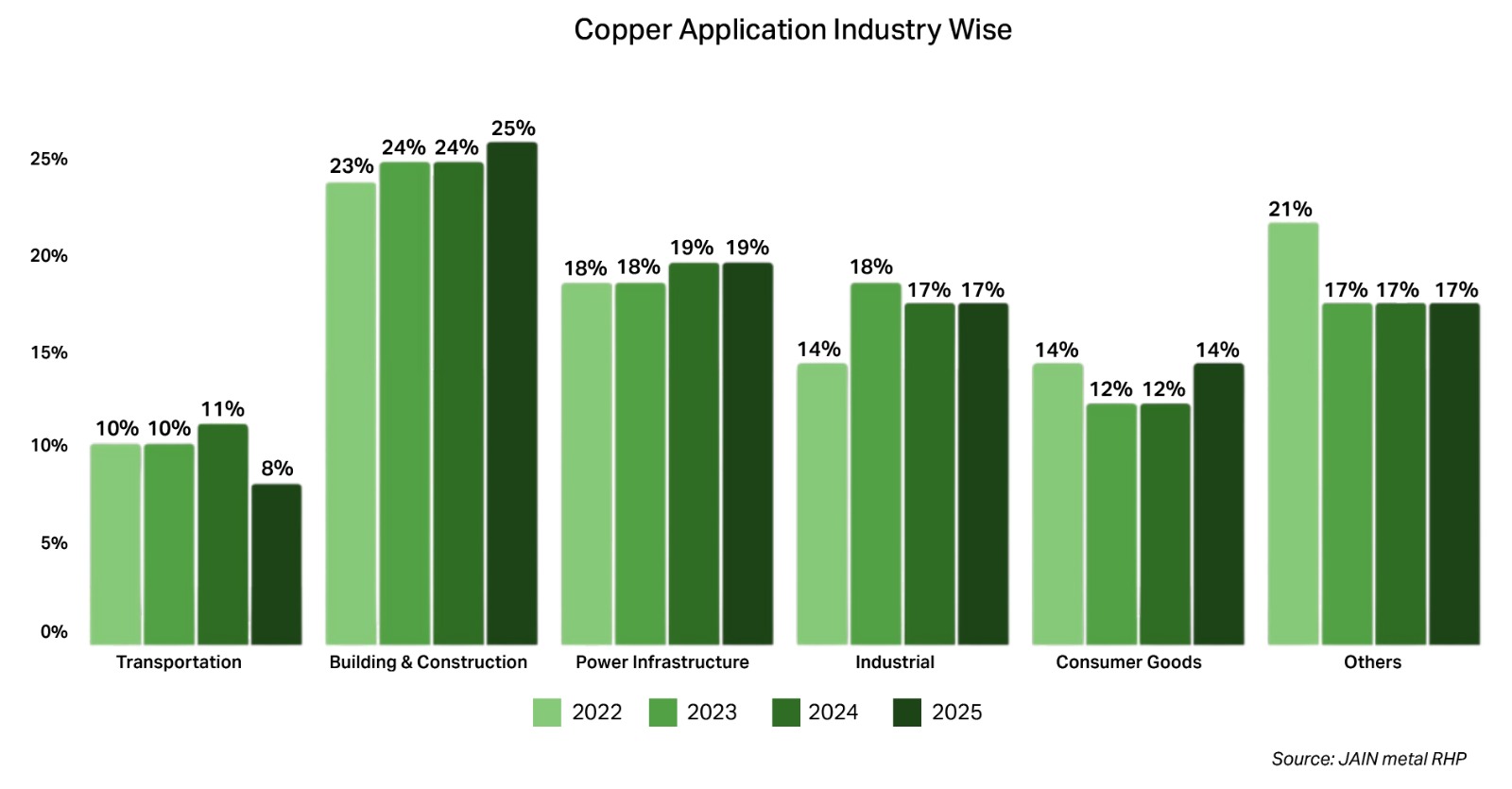

Copper is the bloodstream of modern infrastructure, conductive, corrosion‑resistant, ductile, and surprisingly hard to replace at scale. As grids expand, EV penetration rises, and computing moves into a data‑hungry AI era, copper demand keeps finding new lanes.

- Building & Construction: Building Wires, Plumbing, HVAC, Roofs, Urban transit.

- Power Infrastructure: Wiring Harnesses, Motors, Battery Systems, Charging Infrastructure, Wind/Solar balance‑of‑system, Inverters, Transformers, Transmission upgrades.

- Industry & Transport: Machinery, Rail, Industrial Equipment, Refrigeration.

- Consumer Goods: Appliances like AC, Washing machine, Water heater, Stoves and Microwave.

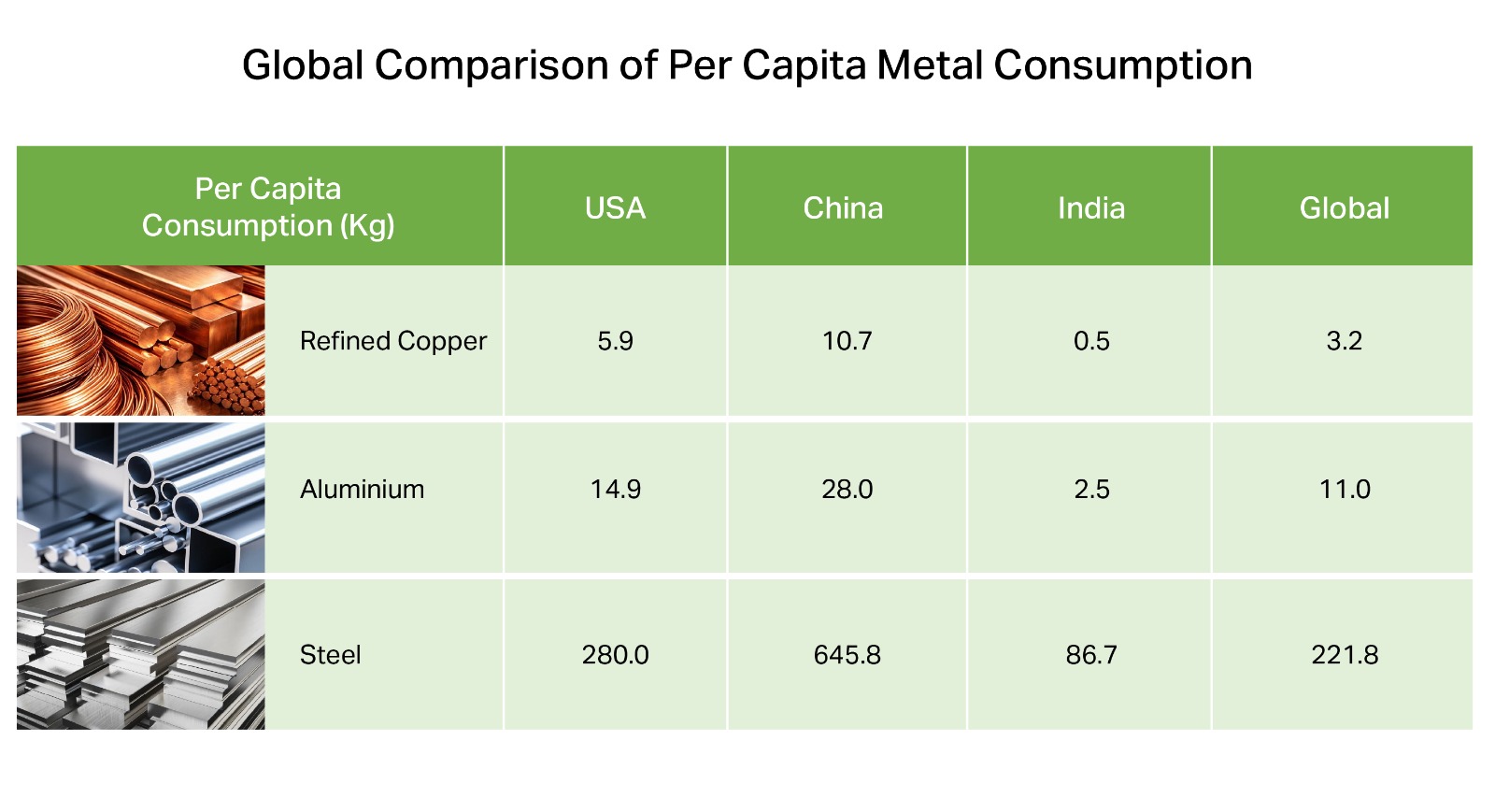

India’s Copper Catch-Up Has Only Just Begun

One simple way to see the headroom is through per-capita copper consumption. India is still at just ~0.5–0.6 kg per person, far below the global average of ~3.2 kg. History shows that copper demand tends to accelerate sharply during phases of industrial expansion. China saw this during its rapid buildout between 2000 and 2012, while the U.S. witnessed a similar surge in the post-World War II growth era.

Primary supply: Slow, Concentrated, and Harder each year

While demand is adding new use‑cases, the primary supply is constrained by geology and timelines. S&P Global estimates it can take ~16–17 years, on average, to bring a new copper mine from discovery to production. Add lower ore grades, permitting complexity, community pushback, and geopolitics supply response becomes sluggish.

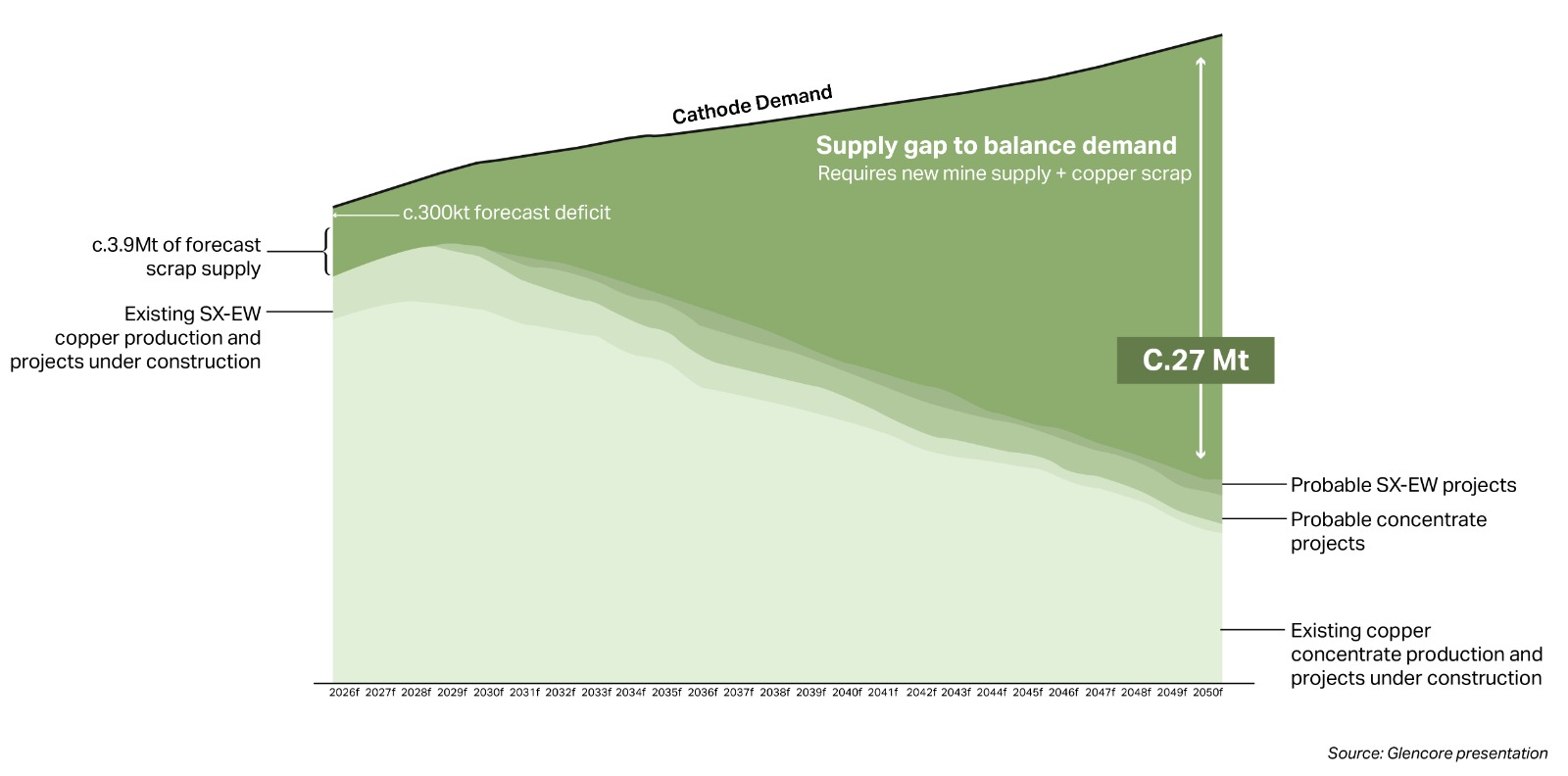

Recent disruptions, mine shutdowns, project delays, and tighter concentrate availability have been enough to swing the market balance, a reminder that the copper supply chain is far less elastic than it appears. Global production edged up from 20.4 MT to 23 MT (a modest ~2.4% CAGR) between 2019 and 2024, while demand climbed faster from 23.4 MT to 25 MT, steadily widening the gap.

And the fragility is not theoretical. Chile, the world’s largest copper producer, has seen output volatility due to declining ore grades, water constraints, and operational setbacks at major mines. In Indonesia, regulatory shifts and export restrictions (Globally 7% share in concentrate copper) linked to smelting requirements have periodically tightened concentrate availability. Meanwhile, Canada evolving regulatory and environmental approval regime has lengthened project timelines, adding friction to new capacity additions.

These disruptions underline a structural truth: new copper supply is capital-intensive, politically sensitive, and slow to respond.

India mirrors this imbalance. Demand is projected to surge from ~3.3 million MT today to 8.9–9.8 million MT by 2047, while domestic supply is expected to rise from just 1.78 MT to only 6–7 MT. Even with aggressive mining expansion, the gap remains persistent.

Recycling: Copper’s shortcut to supply and decarbonisation

Copper is one of the few materials that can be recycled repeatedly without loss of performance. That makes it a rare circular winner. Every tonne of scrap that returns reduces the need to dig, crush, and process ore.

Industry estimates show why recycling is getting strategic attention. Premium copper scrap can retain up to ~95% of the value of primary metal, recycling copper can save up to ~85% of energy and reduce CO₂ emissions by around ~65% versus the primary route.

Where the value pools sit in the secondary chain:

- Scrap sourcing: New scrap (factory offcuts) + Old scrap (end‑of‑life cables, motors, transformers, e‑waste).

- Sorting & Pre‑processing: Segregation, Shredding, Impurity removal—quality here decides realisations later.

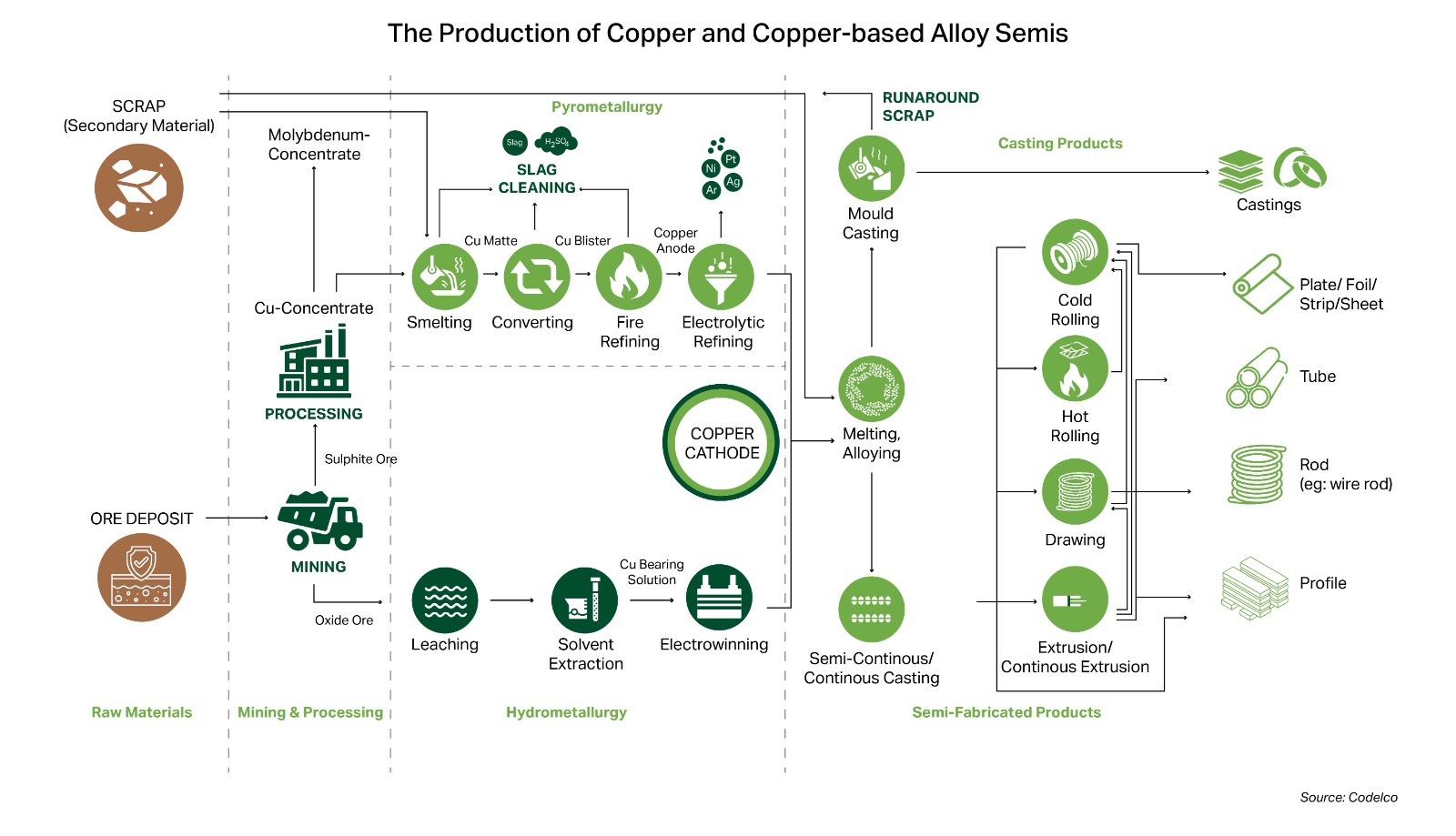

- Smelting & Refining: Fire‑refining to blister, then electrolytic refining for 99.99% cathodes where needed.

- Downstream conversion: Rods, Wires, Tubes, and increasingly busbars for EVs, Renewables, and Data centers.

A practical thumb rule: Every step you integrate forward improves control on purity, traceability, and customer stickiness, often where margins expand.

Whole Value Chain of Primary vs. Secondary copper

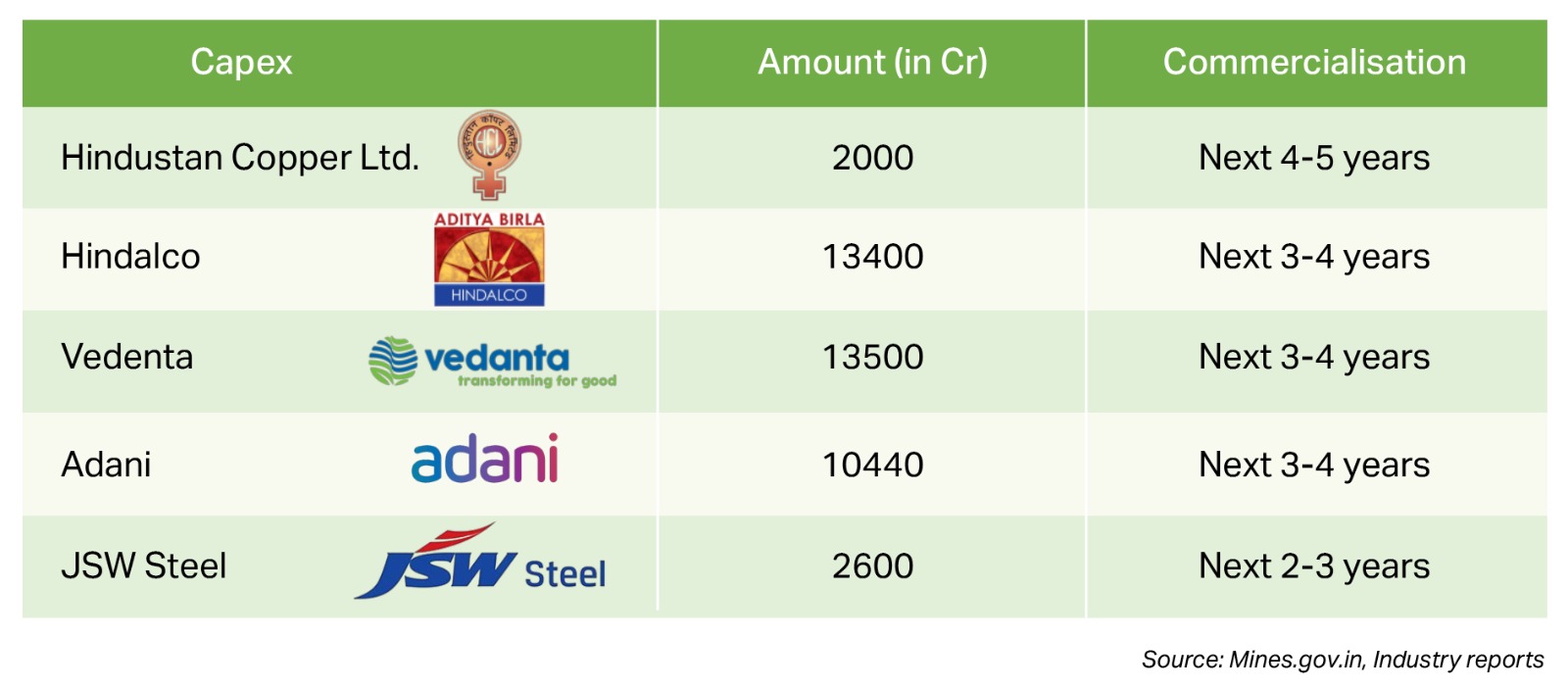

Biggest Mining Capex in Years

Seeing the big demand supply gap various India mining players are putting heavy capex. Even with mining players ramping up capex, the supply deficit is likely to persist, creating a strong runway for secondary copper.

India’s Inflection Point: Policy + Demand + Import dependence

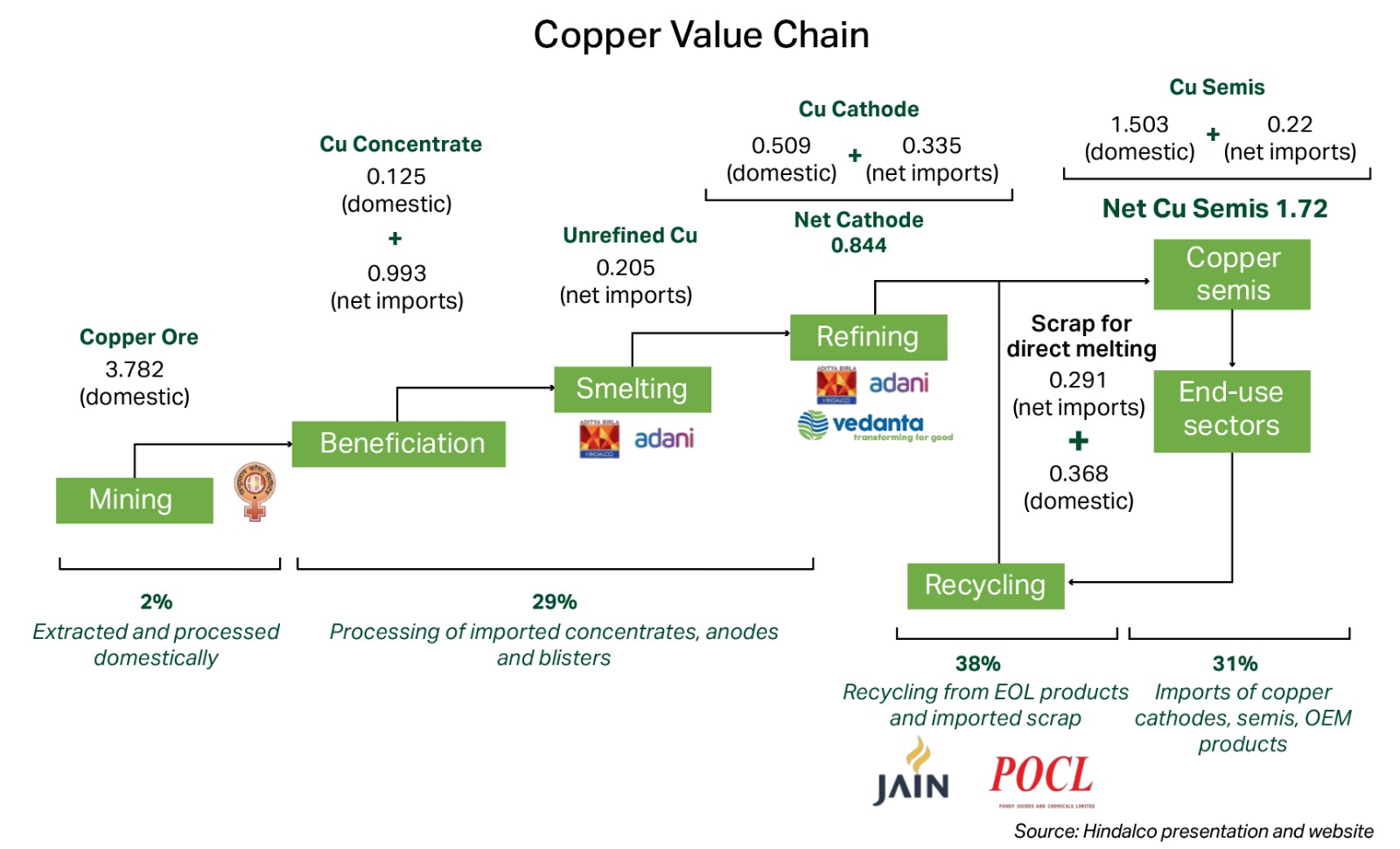

India’s copper story has a twist: Despite rising demand, the country has leaned more on imports in recent years, especially after the 2018 shutdown of Sterlite’s Tuticorin plant, an event that CSEP notes reduced cathode output sharply and worsened import dependence, currently it is 90% import.

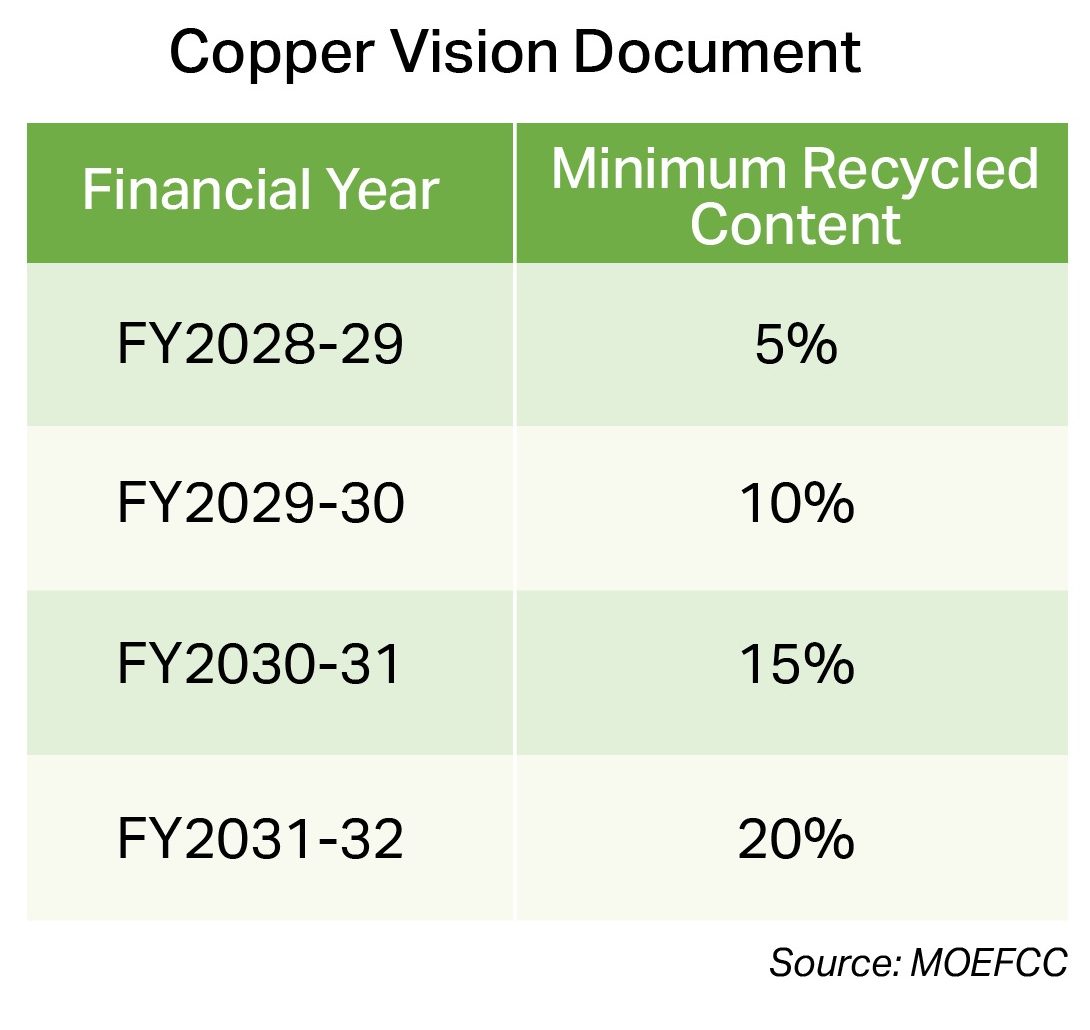

Now, regulation is nudging the system toward circularity. Under the MoEFCC’s Non‑Ferrous Metal Scrap & Recycling framework, minimum recycled content requirements for copper products are slated to step up over time, reaching 20% by FY2031‑32, with intermediate milestones starting at 5% in FY2028‑29. India’s current effective recycling contribution is already estimated at 30% of supply, driven less by policy and more by necessity.

Conclusion: The Future of Copper is Circular

If copper is the new oil of electrification, recycling is the new refinery local, faster to scale, and far cleaner. Primary supply will still matter, but it can not be the only answer when timelines are measured in decades.

The winners won’t be the ones who simply buy scrap. They’ll be the ones who formalise collection, master sorting, guarantee purity, and climb the chain from cathodes to semis (rods, wires, busbars). Because even when prices cool, the shine of recycling doesn’t, it’s tied to physics, policy, and the world’s irreversible move toward electrons.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR