India's Watch Market Has Three Different Clocks

The sequel to Titan’s origin story isn’t streaming anywhere. It’s sitting in five years of export data

Bombay, 1978. The Indian watch market runs almost entirely on smuggled Swiss pieces, a state-run watchmaker no one trusts, and a Tata Group executive named Xerxes Desai who’s just been handed a near-impossible brief.

Build a watch India can be proud of, from a country nobody believes can build one. That’s the opening act of Amazon MX Player’s Made in India: A Titan Story, and it’s worth the six episodes.

But every origin story runs out of episodes. This one’s sequel never aired on TV.

It’s been playing out quietly instead – in Swiss customs filings, company reports, and shipment data from the last five years.

And it’s a stranger story than the one on screen. Not one industry, but three – each moving at its own pace.

That’s the story this piece actually tells. Not through one growth number – through three.

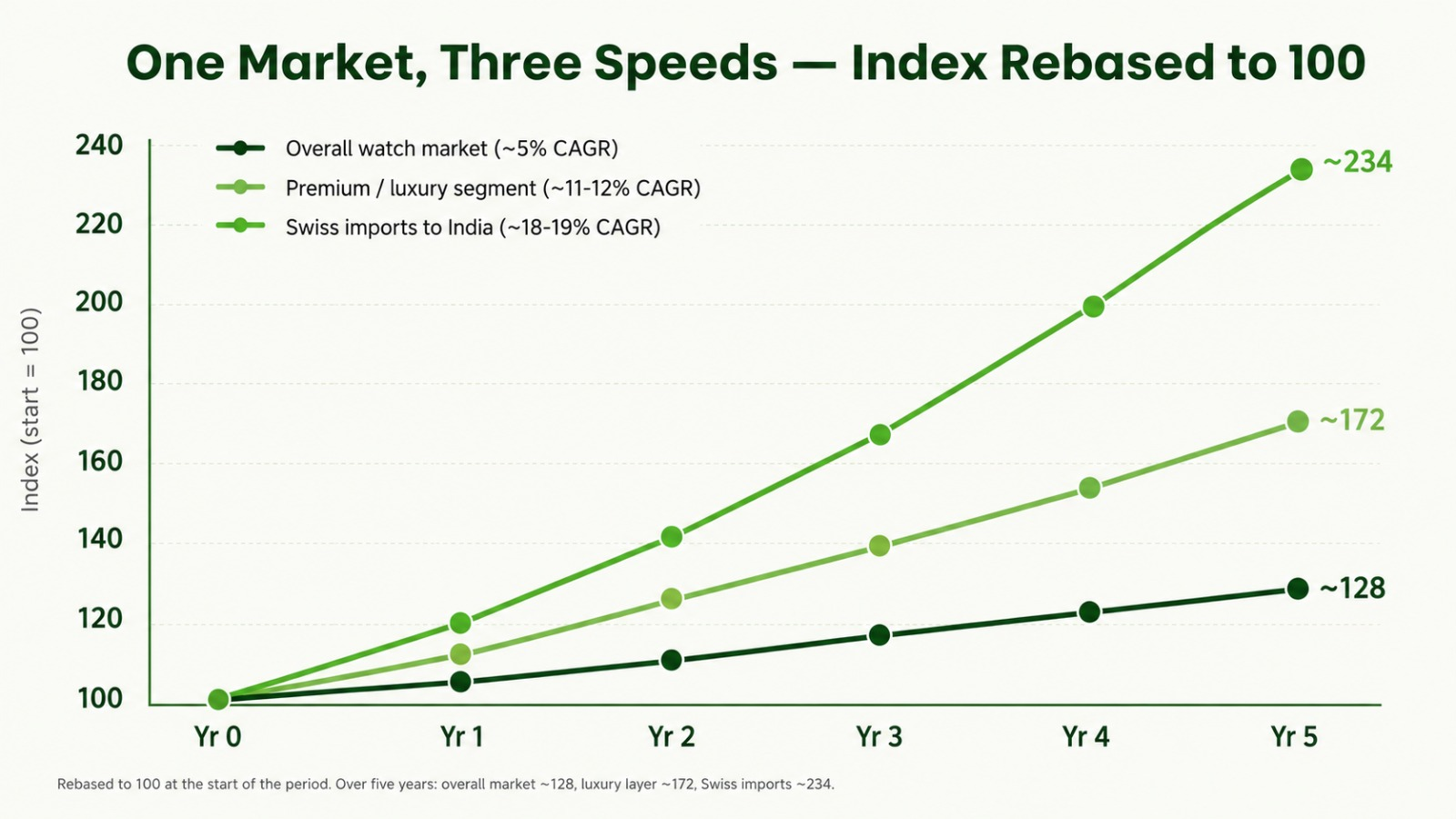

01 One Market, Three Speeds

Ask five analysts how fast India’s watch market is growing and you’ll get answers anywhere between 5% and 19%.

Nobody’s lying – they’re each looking at a different layer of the same market, and each layer moves at a genuinely different speed:

- Overall market (~5% CAGR): USD 5.24 bn (2020) → an estimated USD 6.71 bn (2025) → a projected USD 8.58 bn (2030E). Unhurried, and dragged down by a huge base of inexpensive watches and budget smartwatches.

- Premium & luxury segment (~11-12% CAGR): roughly USD 1.7 bn in 2025 – more than double the overall market’s pace.

- Swiss imports to India (~18-19% CAGR): the fastest layer of all over the last five years – a small number, growing quickly off a low base.

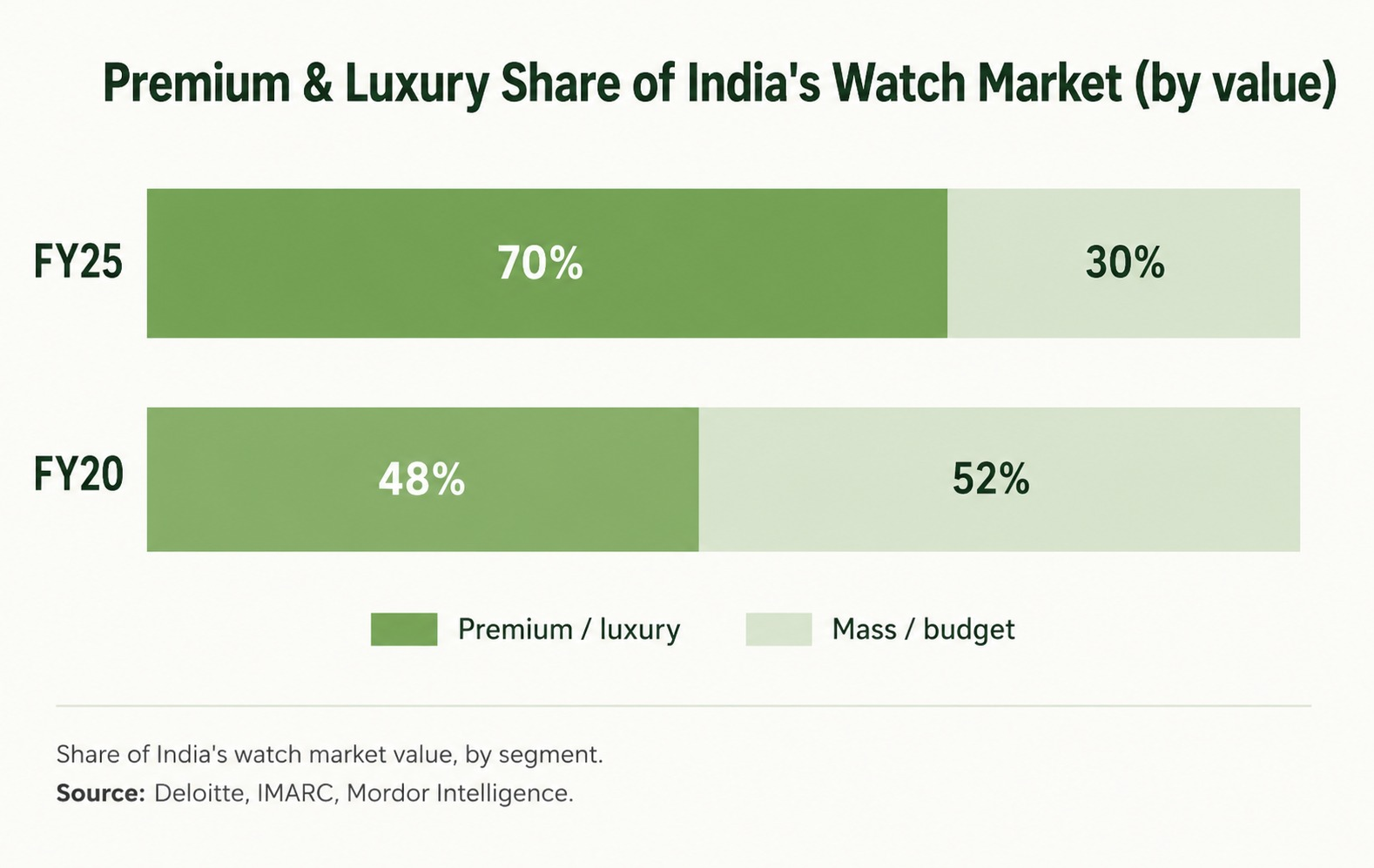

Growth rates alone can be misleading. The clearer proof is in how the market’s own composition has shifted.

Five years ago, premium and luxury watches made up less than half of what Indians spent on watches. They don’t anymore.

A single “market growth rate” hides more than it reveals here – it averages three markets that barely resemble each other in speed.

This is also, quietly, why two earlier drafts of this same research disagreed with each other – one citing ~10.2% (a wristwatch-specific series), the other ~5% (a broader market series). Neither was wrong. They were just standing on different floors of the same building.

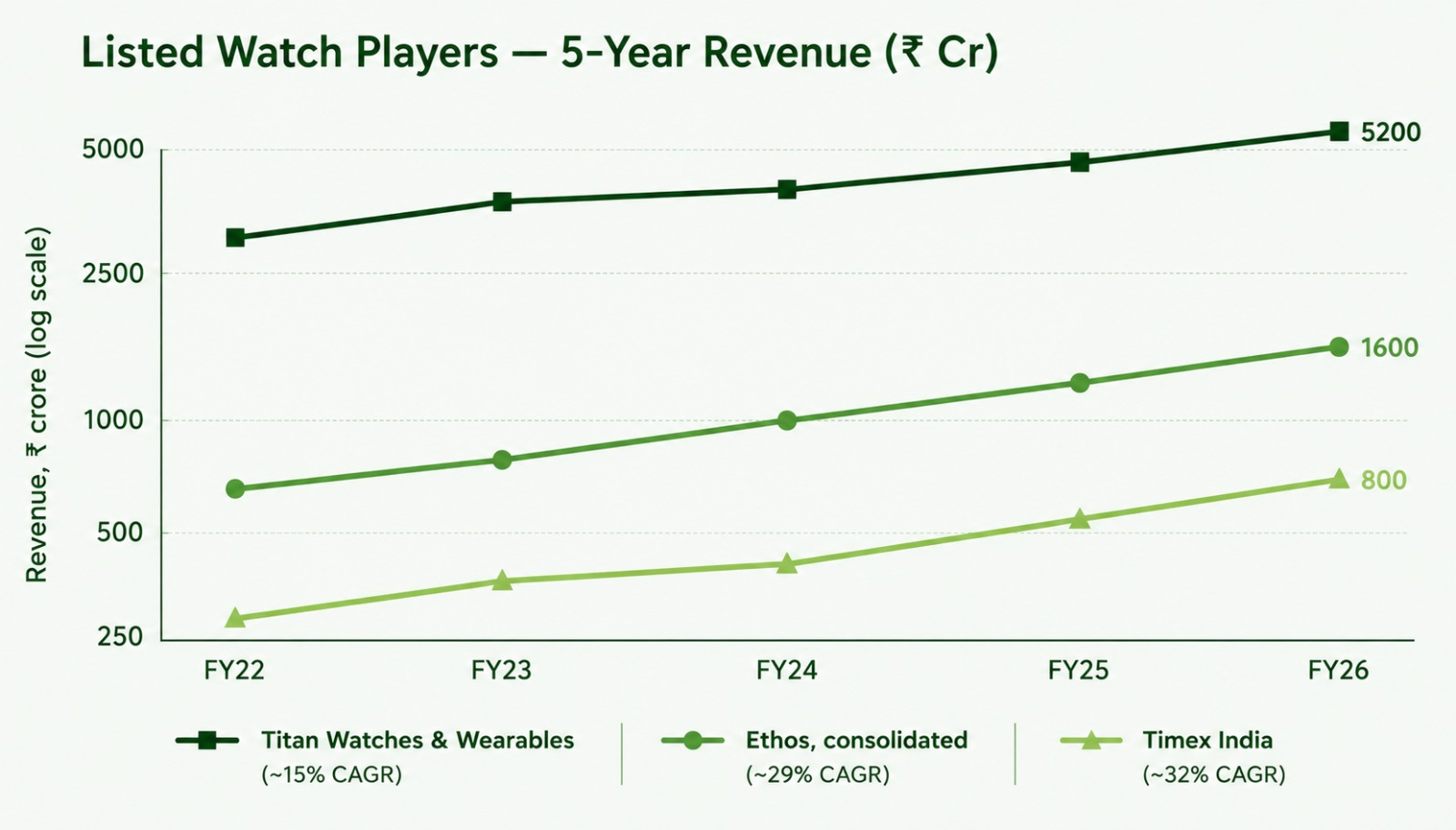

02) Three Companies, Betting on the Same Layer

If the premium layer is where the real growth is hiding, three listed companies are the closest thing to a scoreboard for who’s actually capturing it.

Timex – the quiet turnaround

- Timex is the one nobody was watching a few years ago.

- PAT of ₹3.2 Cr (FY22) → PBT of ₹38.1 Cr (FY26).

- ~32% revenue CAGR – the fastest of the three.

Ethos – betting on luxury and the second-hand market

- Ethos compounds at ~29% on two engines: luxury retail, and certified pre-owned (CPO) watches.

- CPO business grew 32% in FY25, at an average ticket size of ~₹2.04 lakh per watch.

Titan – the giant, recalibrating in real time

- Titan‘s Watches & Wearables division lifted EBIT margin from 5% to 16.2% between FY25 and FY26.

- Missed its own ₹10,000 Cr FY26 target, landing at ₹5,267 Cr instead – the smartwatch bet underdelivered.

- The growth that did show up came from analog premiumisation, not wearables – a thread this piece picks back up in Section 05.

Ethos and Timex outgrow the headline market because they capture organised, premium share within it – not because the market itself accelerated.

That’s the view from inside India. The clearest outside confirmation comes from Switzerland’s own trade data.

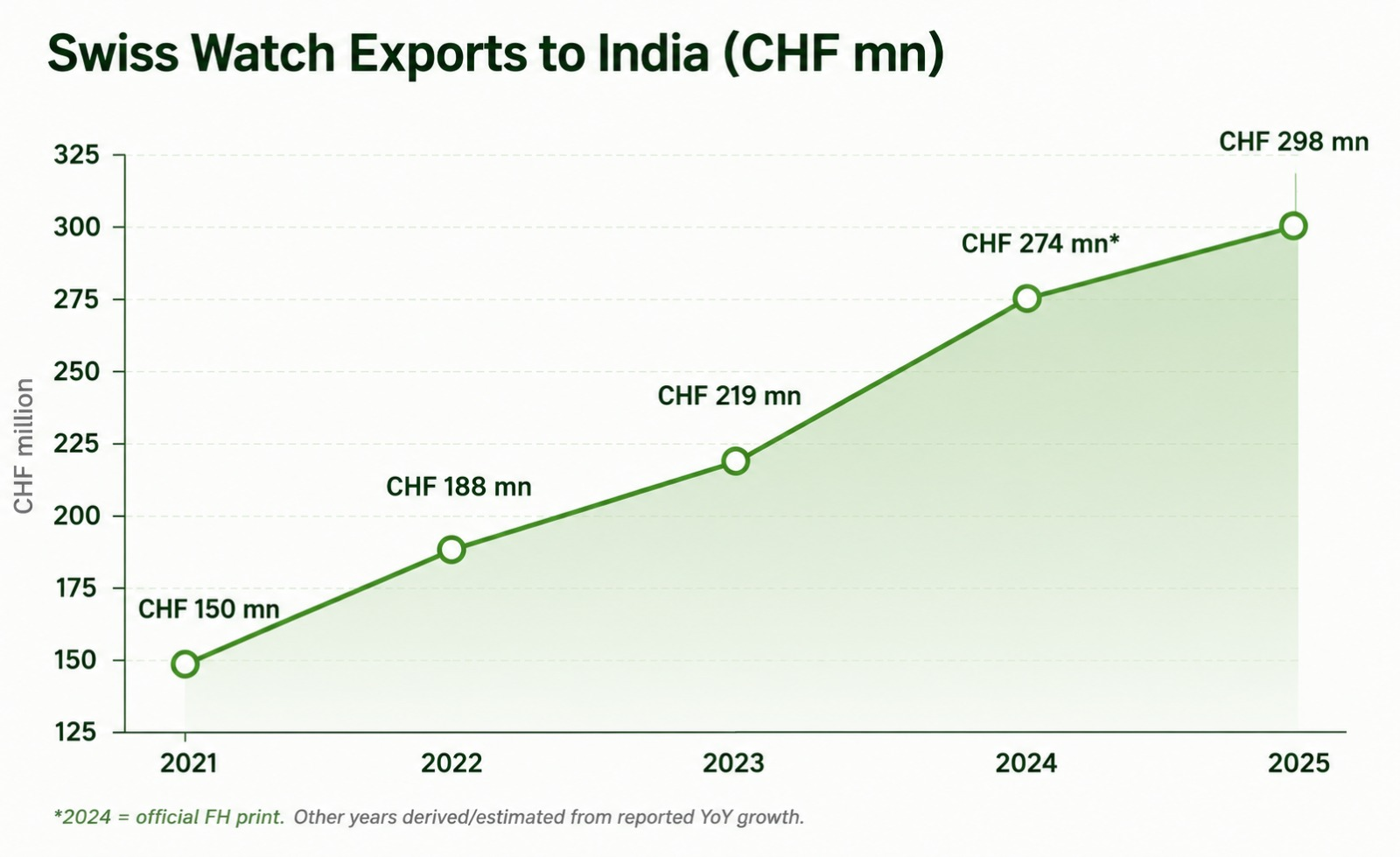

03) What Switzerland’s Own Ledger Says

Switzerland keeps meticulous books on where its watches go, which makes Swiss export data the easiest of the three layers to fact-check.

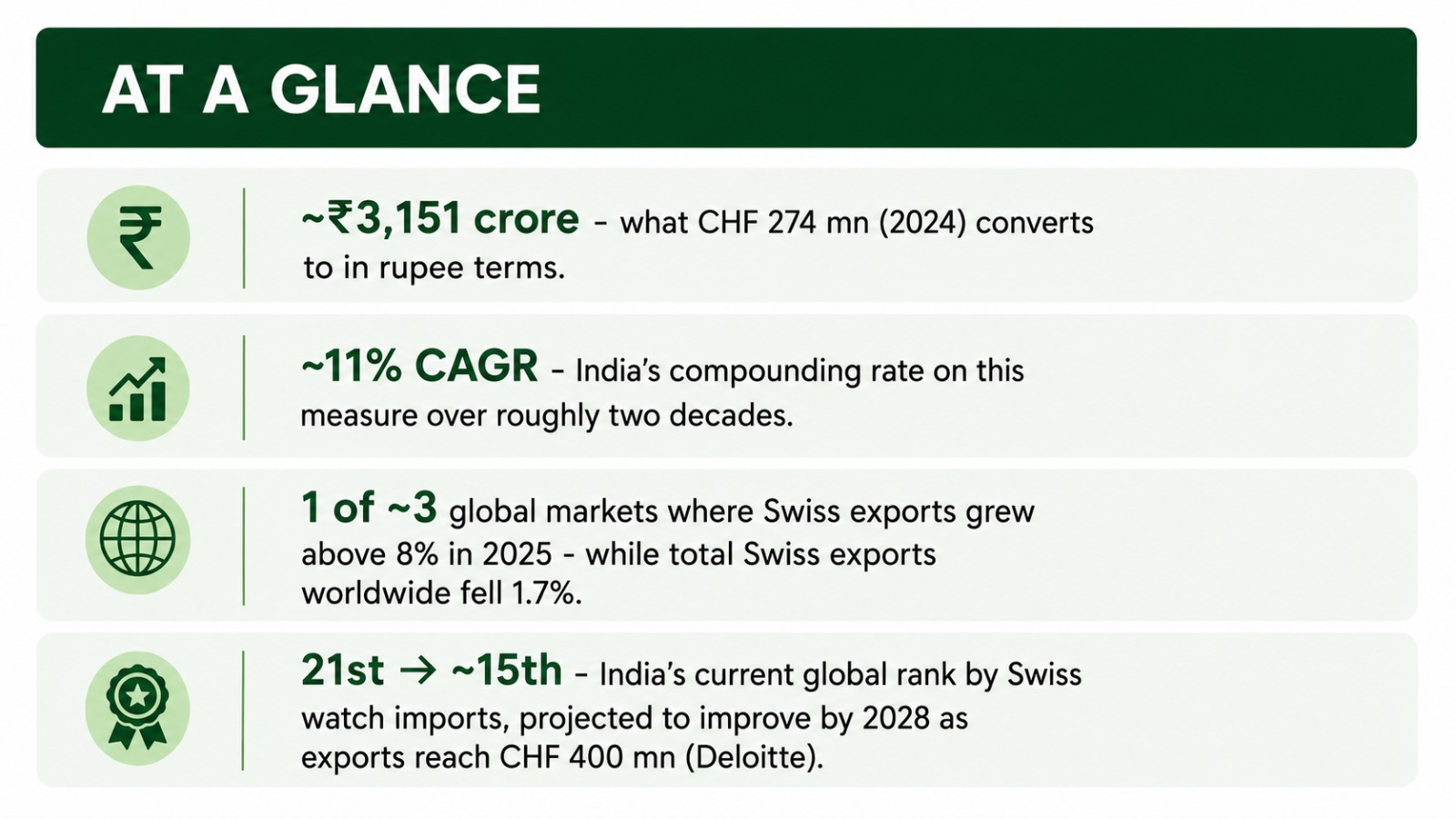

The Federation of the Swiss Watch Industry confirmed CHF 274 million of exports to India in 2024.

- 2024: CHF 274 mn – the one officially confirmed figure in this series.

- 2025: ~CHF 298 mn – an estimate based on a reported +8.9% YoY growth rate.

India is still a minor character on the world stage – 21st, by this measure. But it’s one of a small handful of markets still growing while the rest of the world’s Swiss watch trade shrank. Being early to a trend and being unimportant to it are two very different things, and the data says India is the former.

04) The World Noticed Before the Data Caught Up

Long before quarterly results confirmed any of this, the infrastructure had already started moving. A sample of what’s on record:

- Jaeger-LeCoultre, IWC, Cartier, Bvlgari, Rolex and Panerai now hold flagship boutiques inside Mumbai’s Jio World Plaza; Jacob & Co opened its Mumbai flagship in partnership with Ethos.

- Bain & Co estimates India’s broader luxury market could reach ~USD 200 billion by 2030.

- Deloitte’s 2025 study: 79% of watch industry executives named India the most promising market worldwide – ahead of the US, for the first time.

- Deloitte’s 2023 study had already forecast India entering the top-10 Swiss export markets within a decade; 94% of Indians surveyed said they wear a watch.

- Karine Szegedi of Deloitte points to India and Mexico as sources of young, dynamic customers open to innovation.

- Europa Star (Jan 2026) reports Rolex, Omega, Cartier, TAG Heuer and Breitling continuing to expand in India, Rado capitalising on its early lead, and Favre Leuba (under KDDL) returning.

Perhaps the best line on all this came from a veteran retailer, quoted via Europa Star, who put the required temperament simply:

“India is not a market for short-term thinkers.”

Fittingly, that’s also the whole moral of Xerxes Desai’s watch.

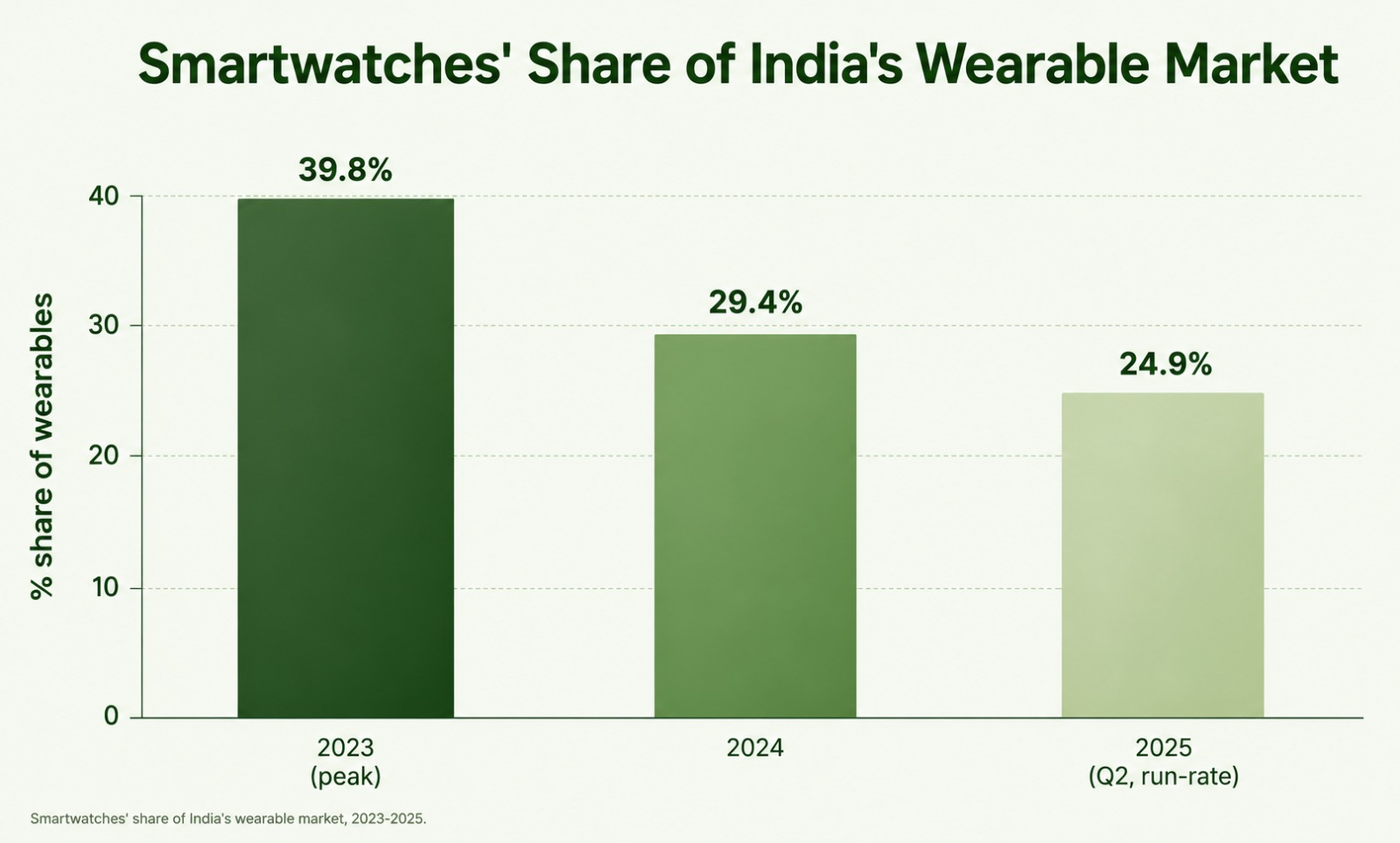

05) The Twist Inside “Smart”

Every good story needs a reversal, and this one arrived in the segment everyone thought was the future: smartwatches.

- 2024: India’s total wearable market fell for the first time ever – down 11.3% to 119 million units.

- 2024: smartwatch shipments alone fell 34.4% to ~35 million units, followed by a sixth straight quarterly decline by mid-2025.

- Over three years: average smartwatch selling prices fell more than 60% amid aggressive price wars.

- 2024: yet the premium tier (>₹20,000) surged +147% – even inside “smart,” money moved upmarket.

Titan’s own numbers make the trade-off almost too neat: analog watches grew 15% in FY26 at a 16.2% EBIT margin, while its wearables business fell roughly 50%.

Budget-digital fatigue and an analog-plus-premium comeback turned out to be the same story, told twice.

The Episode Still Airing

The MX Player version of this story wraps up with Titan finally shipping a watch India could be proud of.

The data’s version doesn’t have a finale – it’s still airing, three episodes a year, at three very different speeds:

- The overall market keeps compounding at a modest ~5% – a large, slow base that isn’t rewriting itself soon.

- The premium layer is where the real plot is, now past two-thirds of the market’s value.

- Swiss imports, the fastest thread of all, are still describing a market that ranks just 21st in the world – early in the season, not late.

None of this is a stock recommendation, and five years of data is not a script for the next five.

It’s simply a reminder that the number worth remembering depends on which layer of the market you’re asking about – and that conflating them is how two honest analysts end up quoting two very different growth rates for the same industry.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR