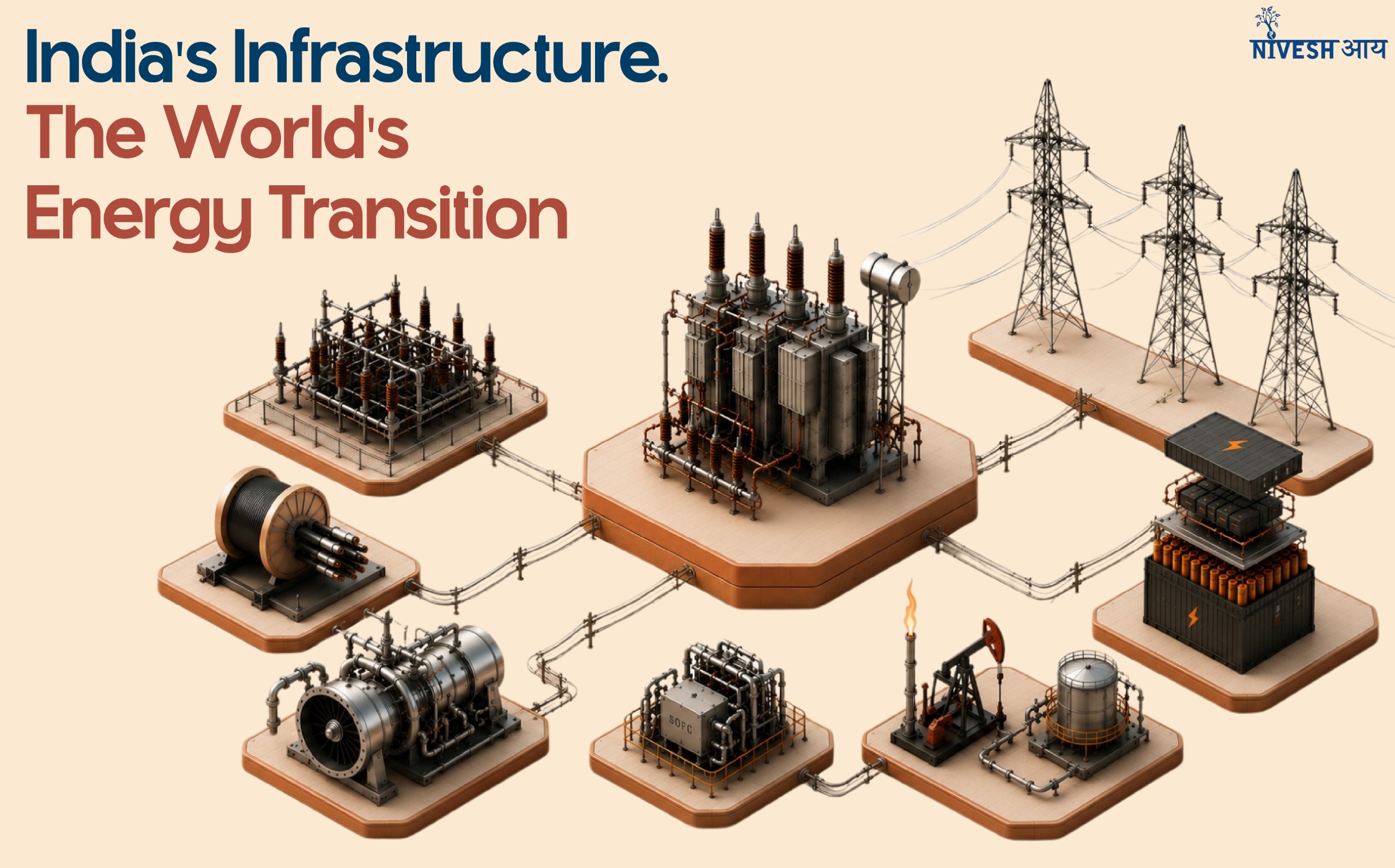

The Bottleneck Nobody Talks About in the Energy Transition

India curtailed 2.3 TWh of clean electricity in 2025, enough to power 400,000 homes for a year. Not because the solar panels stopped working. Because the wires to carry that power did not exist.

Solar can be built in 18–24 months. That speed is its biggest advantage. But it created a new problem: solar farms started finishing faster than the equipment needed to connect them could be manufactured.

The power plant is ready. The electricity cannot move.

And India is not alone. In 2025, global clean energy investment hit $2.3 trillion. The US, EU, India, and the Gulf are all running the largest energy buildouts in their histories, simultaneously, all ordering from the same handful of manufacturers. What felt like a local bottleneck turned out to be a global supply chain collision.

The Curtailment Crisis: The Most Concrete Proof

Between March and August 2025, at least 30 solar and wind projects across India faced curtailment, with financial losses estimated at ₹700 crore in just six months.

Rajasthan curtailment: nearly 4 GW; started at 8.5% in March, rose to 51.5% by August

Gujarat and Maharashtra: 10–30% curtailment during peak solar generation hours

Total solar curtailed (May–Dec 2025): 2.3 TWh – enough to power ~400,000 homes for a year

Rajasthan’s total approved transmission capacity: 14,000 MW. Commissioned and approved generation: ~22,500 MW. The state has 60% more generation than its transmission system can absorb.

The panels were generating. The electricity existed. The wires were not there.

This is green energy’s success creating its own constraint. The faster solar scaled, the more visible the gap became.

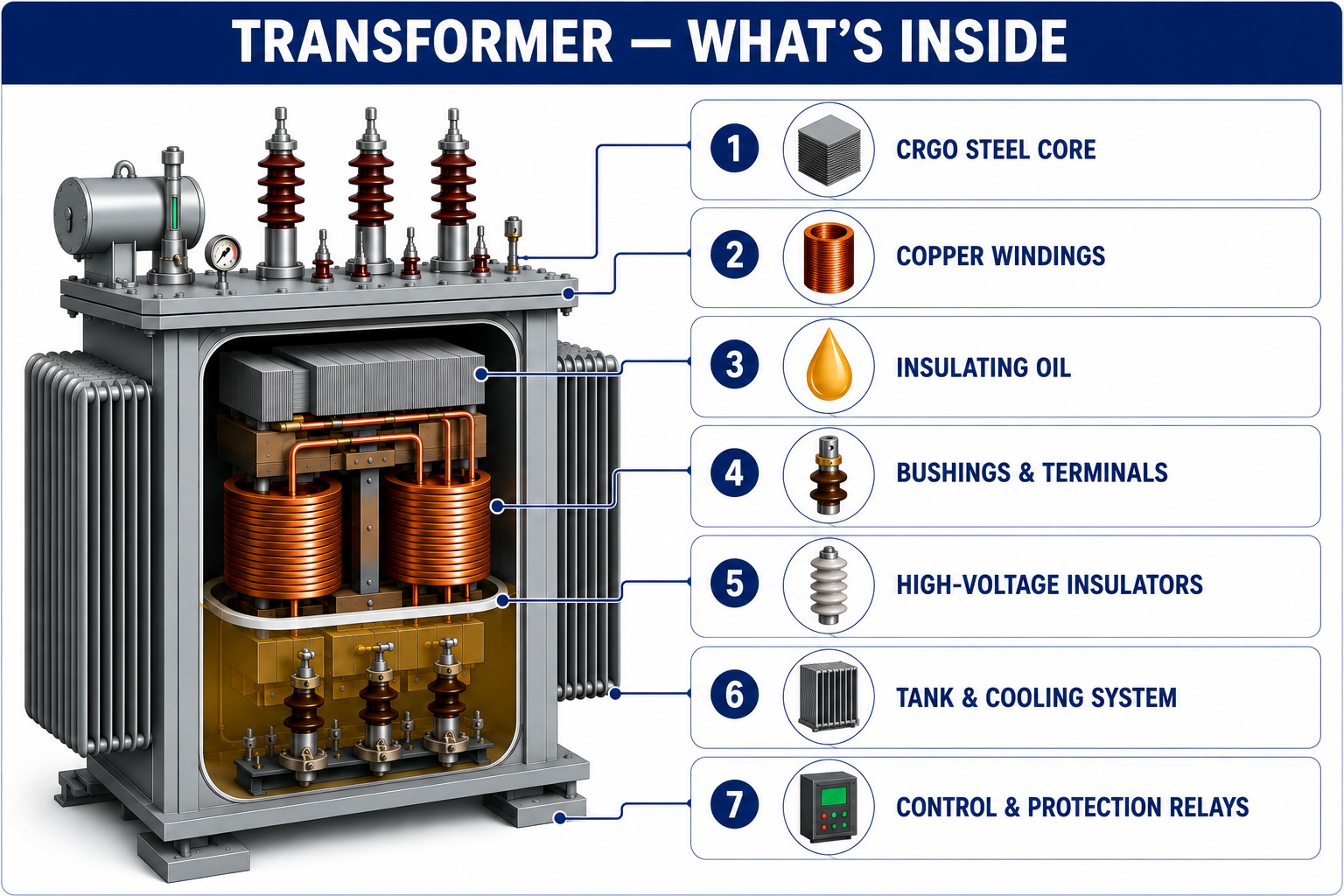

Transformers: The Pinch Point Holding Everything Back

Every solar farm, wind project, data centre, and factory needs a transformer to connect to the transmission network. It is not optional. There is no substitute. And right now, it is one of the scarcest pieces of industrial equipment on earth.

Lead time, 2019: 24–30 months

Lead time, Q2 2025: 128–144 weeks for standard units; specialist orders stretching to 4 years

Power transformer price increase since 2019: 77%. Distribution transformers: 78–95%

Generator step-up transformer demand since 2019: up 274%. Manufacturing capacity has not kept pace

Transformers need CRGO steel, made by just five mills globally. Certified manufacturers take 2–3 years to qualify. Skilled engineers take years to train. Fix one layer, the next one still blocks. The shortage is expected to persist until 2029.

India Opportunity – Insulators

Inside every transformer bushing sits a high-voltage insulator, the ceramic sleeve that prevents arc discharge at transmission voltages. Without it, the transformer cannot operate. India imports ~70% of its requirement today.

India insulator market: $451 million (2025) → $725 million by 2034

The NEP targets 270,000 circuit km of new transmission lines by 2027. As corridors push to 765 kV and 1,200 kV UHV AC, certification requirements tighten. India already has global-scale domestic players:

- Aditya Birla Insulators – largest in India, top four globally, produces up to 1,200 kV, 56,400 TPA capacity

- Modern Insulators Ltd – Siemens Germany collaboration, exports to 50+ countries, up to 800 kV+

- Hindustan Urban Infrastructure Ltd (HUIL) – order book ₹125 crore as of June 2024, exports to 33+ countries

Domestic plays on a component India currently imports heavily – demand scales directly with the NEP transmission buildout.

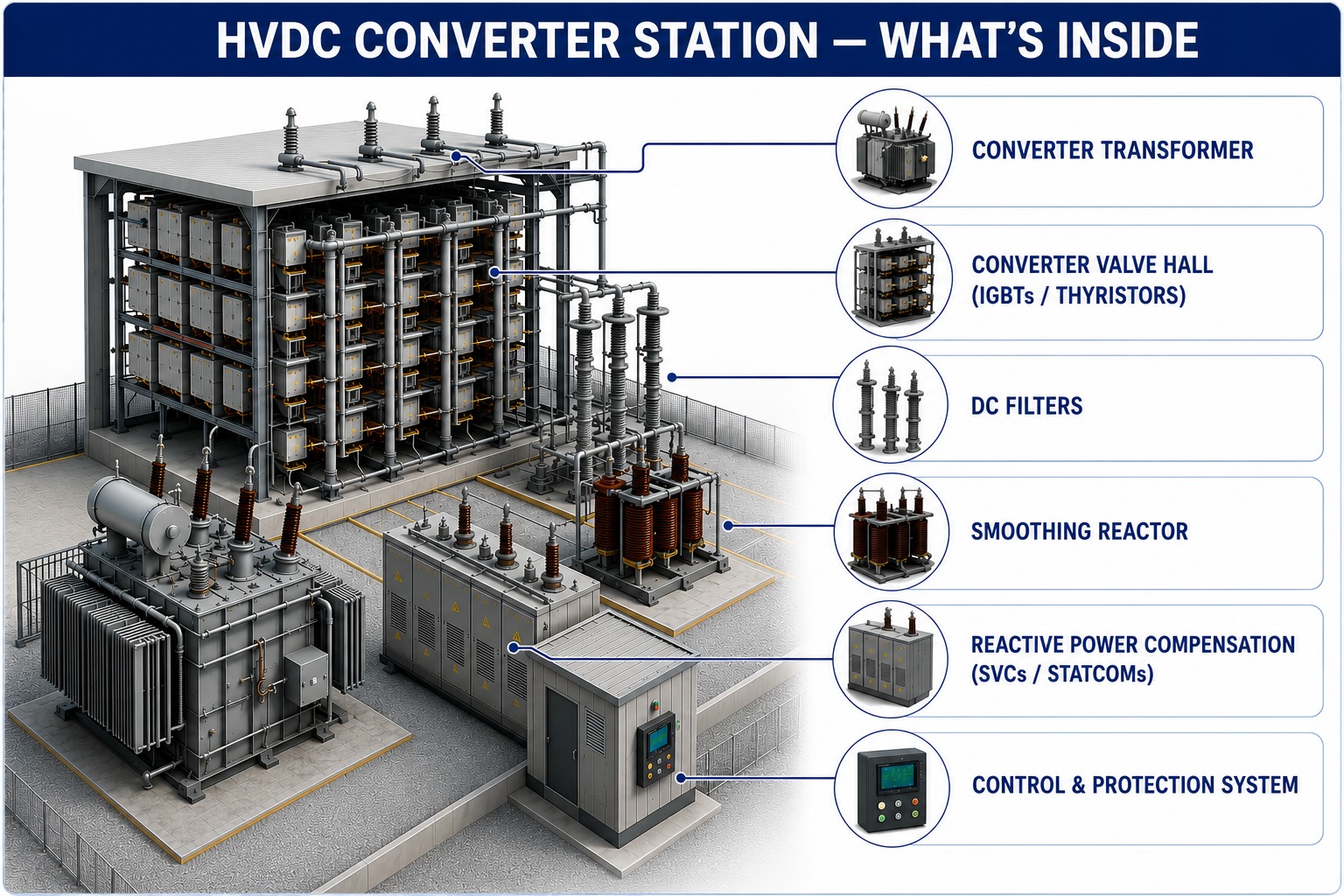

HVDC: The Infrastructure India Cannot Build Solar Without

Connecting a solar farm to its nearest substation solves only part of the problem. India’s geography creates a second, larger challenge.

The best solar resource sits in Rajasthan and Gujarat. The largest demand centres, UP, Bihar, West Bengal – are 1,000 to 2,000+ km away. Standard AC transmission loses 5–8% of electricity per 1,000 km. HVDC loses just 2–3%. At these distances and volumes, HVDC is not a technical preference. It is the only economical solution.

India HVDC market: $3.86B (2025) → $5.84B by 2030 at 8.65% CAGR

Largest HVDC order in India’s history: ₹20,773 crore Ladakh-Kaithal project, Cabinet-approved

Hitachi Energy India order backlog (Q2FY26, Sept 2025): ₹29,412 crore, a company record

India Opportunity – HVDC Conductors & Cables

The converter station is only half the system. Every corridor also needs specialty high-voltage DC conductors and oil-filled cables running its entire length, engineered specifically for HVDC, non-substitutable, and procured fresh for every project.

- Apar Industries – already an approved supplier for HVDC-grade conductors and oil-filled cables. Certification takes years to earn and cannot be replicated quickly. Cables are procured before the converter station is even installed, Apar sits at the front of that order sequence.

- BHEL-Hitachi (Khavda–Nagpur corridor) – ₹25,000 crore total project; BHEL-Hitachi share ₹4,000–6,000 crore. First of 2–3 HVDC awards Nuvama Research expects every year. Each project converts procurement into domestic engineering capability.

- GE Vernova T&D India – investing ₹1.4B to expand its HVDC thyristor and VSC valve facility in Chennai. Any new entrant at converter station level needs ₹2,000+ crore and 5–7 years.

JP Morgan estimates $14–15B in HVDC opportunity for Indian players over the next 5–6 years. The cable layer is where a domestic player is already qualified, already earning, and scaling with every corridor India builds.

Battery Storage: Closing the Timing Gap

Transformers connect solar farms to the network. HVDC moves power across long distances. But a fundamental timing problem remains: solar generates most heavily at noon. Demand peaks in the evening.

Without storage, that mismatch either forces curtailment, the ₹700 crore problem already playing out, or keeps fossil backup running permanently. BESS stores midday surplus and dispatches it when demand rises, reducing both curtailment and the peak load the transmission system must carry.

BESS is what converts intermittent green electricity into a 24/7 supply contract. Without it, every solar panel India installs is generating electricity that cannot be fully used.

India BESS market: $2.05B (2026) → $8.59B by 2031 at 33% CAGR

BESS growth in 2026: under 200 MWh (2025) → ~5 GWh (2026) – a near-tenfold expansion in one year

BESS tenders issued in 2025 alone: 69 new tenders totalling 102 GWh – nearly double all previous years combined

CEA BESS target by 2031–32: 236.2 GWh battery + 175.2 GWh pumped hydro = 411 GWh total

India Opportunity – Battery Cell Manufacturing

The constraint inside BESS is the cell – currently ~6 Chinese manufacturers dominate global supply. India’s ACC PLI target is 50 GWh; only 1.4 GWh is commissioned – 2.8% achievement. Two players are building outside the PLI framework, on commercially viable timelines:

- Amara Raja – 16 GWh cell facility in Telangana, ₹9,500 crore invested, technology from Gotion High-Tech. Targeting domestic production by 2027–28.

- Exide Industries – partnering with SVOLT for cell technology. Same 2027–28 timeline, without PLI penalty clauses that would have forced impossible milestones.

Cell import dependency until 2027–28 is the constraint. These are the two domestic plays building into it.

How Green Energy Created the Gas Turbine Shortage

The connection between green energy and gas turbine shortages is not obvious. Here is how it happened.

As solar and wind scaled globally, grids needed dispatchable backup- power that turns on in minutes when the sun is not generating. Gas turbines are that backup. Simultaneously, AI data centres that cannot wait 5–7 years for a network connection started generating their own power on-site. Gas turbines are the on-site solution.

The green energy buildout that is replacing gas in power generation is simultaneously driving record demand for gas turbines as backup and as data centre power. Green energy did not reduce gas turbine demand. It restructured it and compressed the timeline from years to months.

Gas turbine lead times, 2020: 12–18 months

Gas turbine lead times, 2025: 3–4 years – GE Vernova, Siemens Energy, Mitsubishi Power all at multi-decade high backlogs

US power connection queue, 2025: 2,600 GW+ waiting – more than the entire installed US generation base

Hyperscalers stopped waiting. Microsoft, Google, and Amazon became direct buyers of gas turbines, adding a third demand signal to a supply chain already strained by grid modernisation and industrial backup needs.

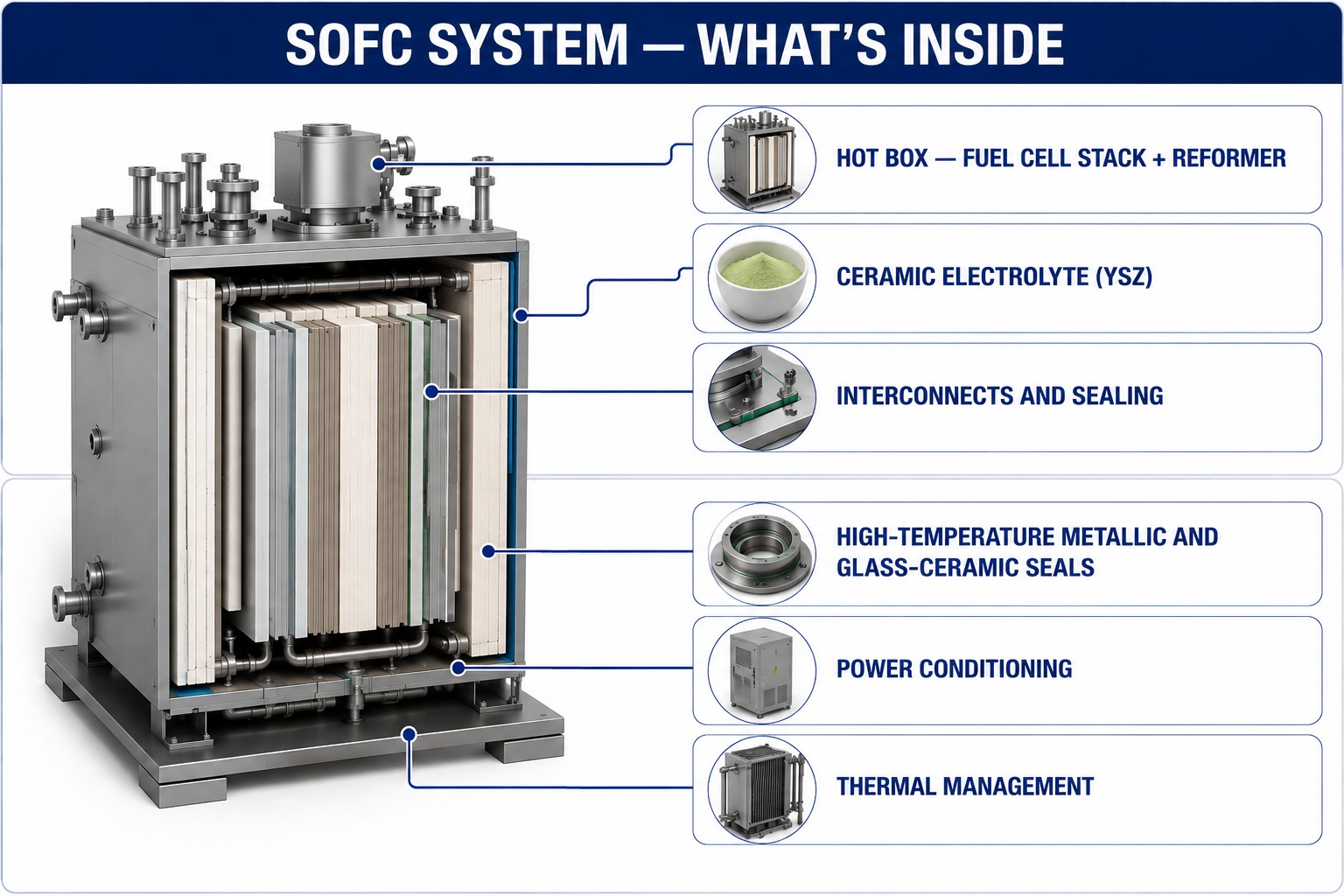

SOFC – The Technology Hyperscalers Are Betting on Beyond Gas Turbines

Gas turbines are powerful but inflexible, they need dedicated space, acoustic mitigation, and specialist maintenance crews. For an AI campus adding capacity server hall by server hall, that is operationally wasteful.

Solid Oxide Fuel Cells solve this differently. No combustion. No rotating parts. Efficiency of 60%+ versus 35–40% for a simple-cycle gas turbine. Units are containerised, stackable, modular, a campus can add 1 MW of SOFC power at a time, exactly as demand grows.

The constraint is the hot box, the core electrochemical unit. And this is where India has a position.

India Opportunity – SOFC Hot Box

The hot box is the highest-value, highest-scarcity node in the entire SOFC system – the single-crystal blade equivalent for this technology. MTAR Technologies manufactures it to the tolerances required by SOFC OEMs deploying systems at Google, Microsoft, and AT&T data centres across the US.

This is not thematic positioning. The orders are active. The OEM qualification cycle takes years; MTAR already holds it. Fewer than 5 manufacturers globally can produce this at commercial scale.

The ceramic electrolyte (YSZ), interconnects, and power conditioning layers all involve specialist materials — but the hot box is where the supply constraint is most acute and the India position most defensible.

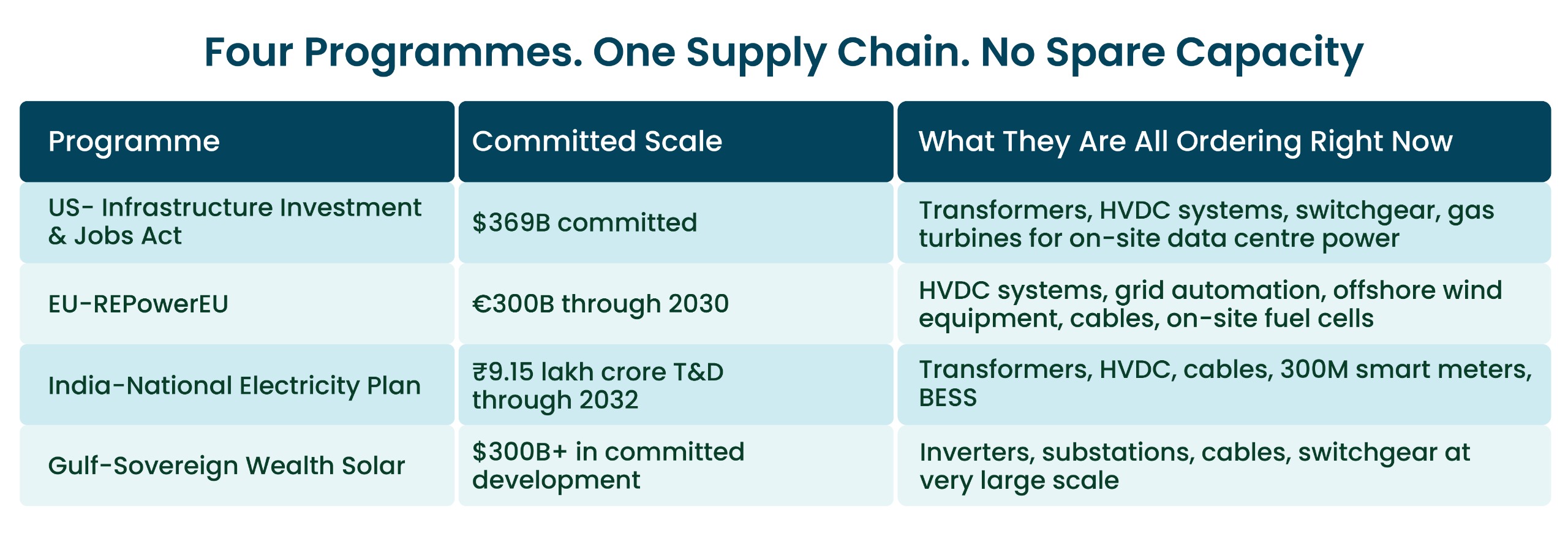

Four Programmes. One Supply Chain. No Spare Capacity.

Every major economy is placing orders with the same transformer factories, the same HVDC suppliers, the same cable producers, and the same gas turbine makers – simultaneously.

None of these programmes can be scaled quickly. All require years of qualification, specialist materials, and workers that take years to train. The demand arrived simultaneously. The supply did not.

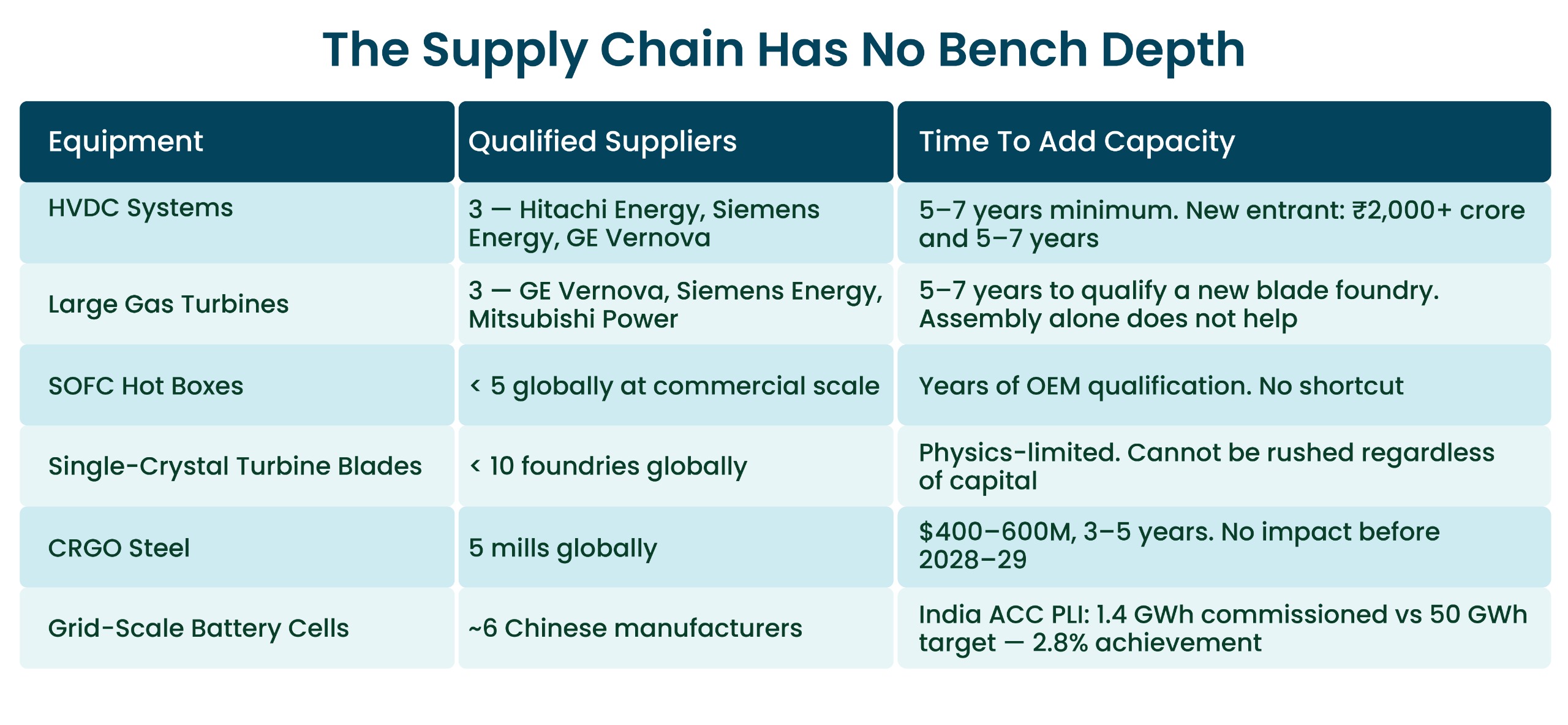

The Supply Chain Has No Bench Depth

Every previous infrastructure boom stressed supply chains that had recovery mechanisms. If one supplier was full, a second was available. The green energy supply chain does not work this way.

When the top tier is full, there is no second tier. That single fact is what makes this crunch structurally different from everything that came before – and why it lasts longer than most forecasts suggest.

India Opportunity – Building Inside the Supply Chain

India is simultaneously the largest new buyer in this constrained market and earning certified positions inside the very supply chain it is ordering from, qualifying at the highest-value, hardest-to-enter nodes:

- ₹9.15 lakh crore T&D capex committed through 2032 – every rupee needs transformers, CRGO steel, HVDC systems, and cables the world is already racing to procure

- Inter-regional transmission scaling 120 GW → 143 GW (2027) → 168 GW (2032) – all under active procurement

- Green Energy Corridor Phase-II – 10,750 ckm new lines + 27,500 MVA new substation capacity

- Power Grid Corp pipeline – ₹1.08 lakh crore (FY26–28); ₹3.06 lakh crore through FY32

Gas turbine blades, SOFC hot boxes, HVDC components, battery cells – not commodities. They are the bottlenecks. And Indian manufacturers are earning certified positions inside them, one qualification at a time.

Key Insight

Solar scaled faster than the infrastructure built to carry it. India is generating electricity it cannot use – ₹700 crore lost in six months to missing wires. The fix needs transformers (shortage until 2029), HVDC (three global manufacturers, all at capacity), gas turbines (lead times now 3–4 years), and BESS (cell import dependency until 2027–28).

Green energy created four simultaneous demand signals on a supply chain built for one. There is no bench depth anywhere in it – when the top tier is full, everyone waits. India’s position is unusual: it is simultaneously the largest new buyer in this constrained global market and earning certified manufacturing positions inside the very supply chain it is ordering from.

These markets together represent over $13B in India today, growing at 8–33% annually, backed by committed government capex. Green energy built the demand. The infrastructure that carries it is where the investment case lives.

→ The supply chain crunch is reshaping who can manufacture competitively. When lower-cost electricity arrives at industrial scale, it reshapes something even bigger – where manufacturing happens at all, and who wins in it.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR