The Battery Show Expo

This year, we had the opportunity to attend The Battery Show Expo, where the entire battery value chain—from cell and pack makers to chemical suppliers and equipment vendors—came together to talk about how India will build its own energy-storage ecosystem. One clear message emerged: India is rapidly moving from being a pure demand market to building serious domestic capacity across BESS assembly, cells and critical materials.

From the shop floor to the chemistry lab, everyone is gearing up for scale. BESS pack assembly lines of ~35 GWh are already installed and expected to more than double in the next 12 months, while large Chinese and global players are anticipating significant annual demand from India.

At the same time, Indian electrolyte and precursor manufacturers are stepping in to solve shelf life, logistics and supply-chain risks that come with relying on imports. This note captures our key takeaways from the Expo—covering assembly players, cell manufacturers, chemical suppliers and emerging long-duration storage technologies—and what they imply for India’s battery manufacturing opportunity over the next few years.

Key Takeaways:

A) Assembly players

- There is a significant wave of capacity addition in the BESS assembly space. As per one major player, ~35 GWh of BESS assembly capacity is already installed in India, and this is expected to more than double over the next 12 months.

- Capex per GWh for a BESS assembly line is in the range of ₹10–30 crore, depending on the level of automation, the vendor, and the cell format.

- Vendors reported strong interest this year from visitors looking to set up BESS assembly lines, with noticeably higher traction compared to last year.

- Many EV battery pack assembly lines are currently under-utilised, with low utilisation levels due to overcapacity in EV.

- For switching between chemistries or cell formats, only 15–20% of line components typically need to be changed (for example, to accommodate different cell shapes or

minor process variations).

B) Cell players

- For cell manufacturing equipment, India is still almost fully dependent on China. One large player specifically highlighted the need to reduce import duties and ease visa processing for Chinese engineers as a key enabler for setting up and ramping plants in India.

- There is generally a 24–30 month lead time from placing the equipment order to starting cell production.

- Skilled manpower is a critical bottleneck. Once the plant is installed, the ramp-up itself takes 6–8 months, and can extend further in some cases. On the utility-scale side, LFP is clearly the dominant chemistry everyone is targeting.

- Production lines are not standardised; they are custom-designed based on the specific line configuration and customer requirements.

- Multiple players across the value chain are advocating for the government to impose duties on imports and introduce an ALBM/approved list framework for cells in the coming months.

- One of the largest Chinese cell manufacturers reported much higher interest at this year’s Expo versus last year, and is expecting 100 GWh+ of annual demand from India across ESS + EV.

- 314 Ah cells are likely to be the workhorse format, though some Chinese players also showcased 500 Ah+ cells for high-capacity applications.

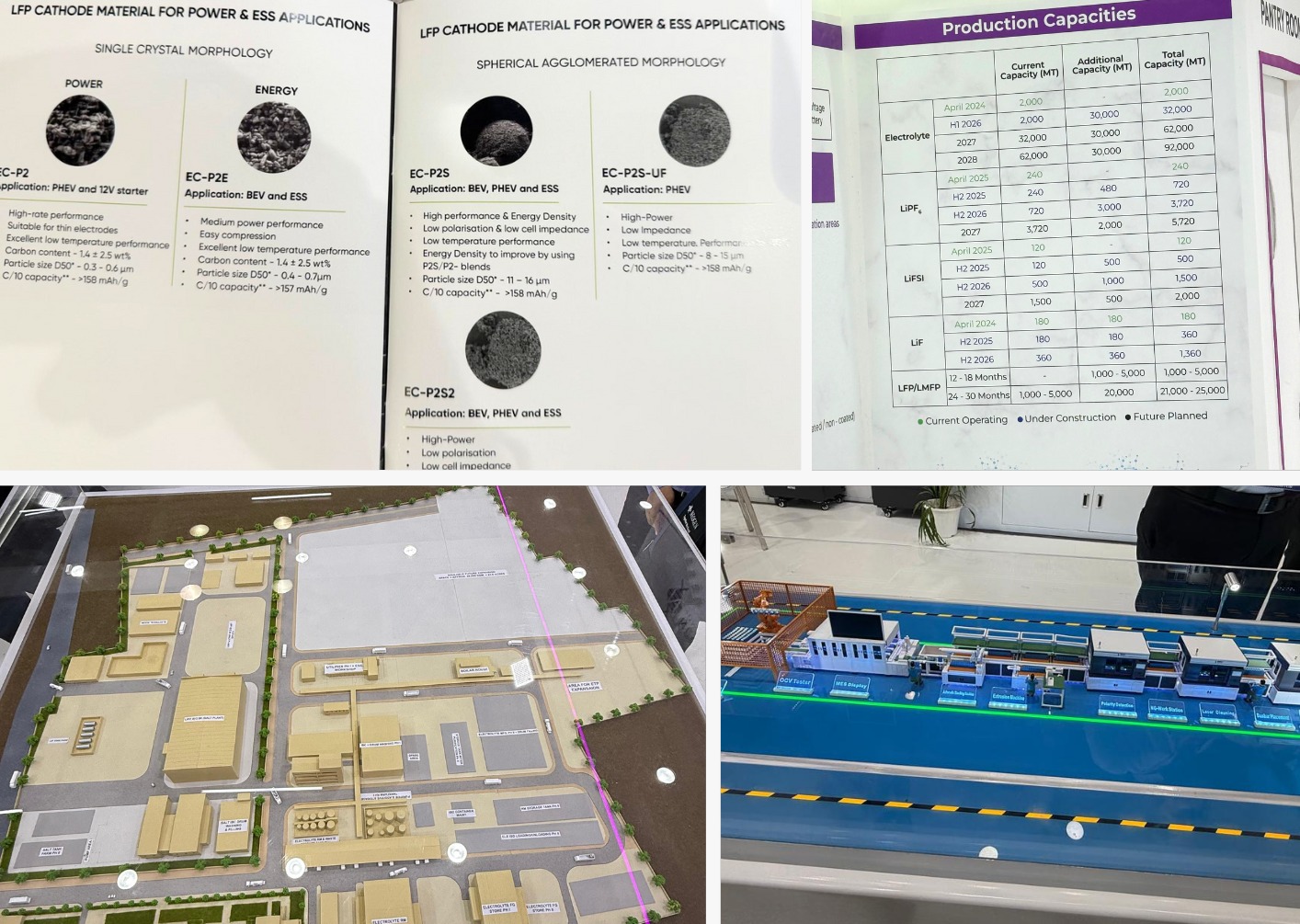

C) Chemicals

- New companies are entering the precursor space (both cathode and anode) beyond the few well-known names, indicating a broadening of the upstream supply chain.

- Like in other industries, non-Chinese cell makers are actively looking for alternative suppliers, which is creating an opportunity for Indian chemical and material players.

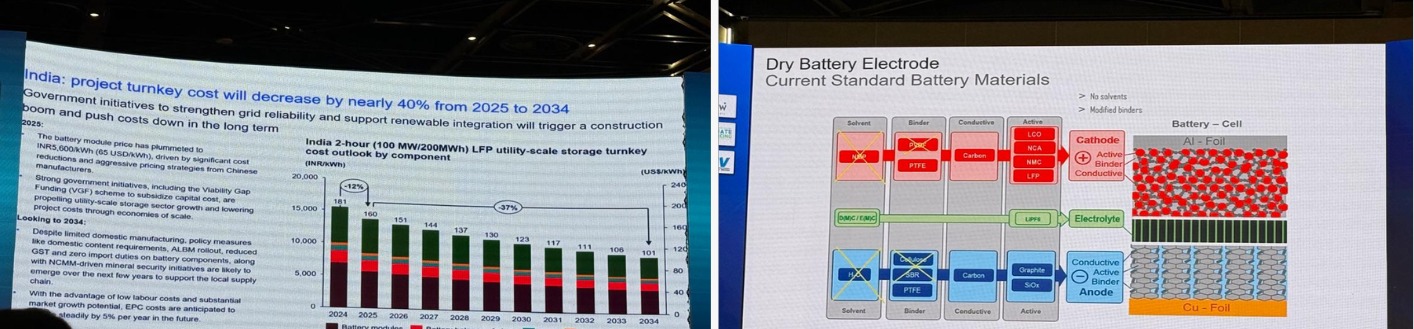

- There are a limited number of established players making electrolyte and its key constituents. The approval cycle is relatively long at 1–1.5 years. In our interaction with a leading electrolyte producer, they indicated that cell makers are increasingly firm on their timelines, improving demand visibility for them.

A key advantage for Indian electrolyte manufacturers is shelf life and logistics:

- Electrolyte typically has a shelf life of ~3 months.

- Imports from China take 1–1.5 months in transit, which can alter properties and quality.

- As new cell and pack capacities come up, there will be a strong pull for local electrolyte suppliers, even though Chinese suppliers are currently 10–15% cheaper.

Others

- Setting up clean room and dehumidification infrastructure for BESS cell manufacturing typically requires about 3 months, after an initial design phase of ~1 month. Once the design is finalised, installation and commissioning takes another ~2 months.

- There are start-ups working on long-duration storage chemistries (10+ hours to seasonal storage). They indicated that:

a) India is still at a nascent stage for long-duration storage.

b) The current market size is smaller than Europe/US, partly because India’s tropical climate has relatively lower seasonal variation.

c) Nonetheless, they expect tenders for long-duration storage to emerge over the next 1–2 years, where lithium-ion may not be viable and alternate chemistries will be

needed. - DRDO is actively focusing on sodium-ion batteries, with the explicit intent to de-risk from lithium and reduce supply-chain dependence on China.

- Also, A large IPP said there is no answer on why there is bidding happening at such a low tariff, he was doubtful of the execution as well.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR