From Pent-Up Demand to Sustained Momentum: The Rise of India’s Travel Industry

Remember when planning a holiday meant sitting with a notepad, counting leave days, booking trains months ahead, and saving hotel stays for once-a-year trips? Travel used to be a carefully budgeted, once-in-a-while affair.

Fast forward to today, journeys has slipped into our everyday rhythm. Airports hum with crowds even on weekdays, and pilgrimage like Kedarnath or Ayodhya are seeing record footfalls. The change is driven by many forces working together: rising disposable incomes, supportive tax cuts, new airports and better infrastructure leading to frequent vacations, workcations, weddings, or quick road trips.

What began as post-pandemic “revenge travel” has become a lasting transformation reshaping aviation, hospitality, and consumption.

Levers that are rewriting India’s travel and tourism industry:

1) Government Push: From Tax Cuts to Increasing Airports

- Tax Rates Reduction: More Disposable Income, More Travel

The government’s recent tax rate cuts have handed middle-class households an extra 50,000–1,00,000 per year in disposable income, which is a direct boost to their spending power. And unlike the past, when such savings might have gone into gold or fixed deposits, today’s consumers are increasingly channeling it into experiences. A long weekend in Goa, a family trip by air instead of train, or an upgraded hotel stay has become not just aspirational, but achievable.

This marks a decisive shift in how Indians allocate their incremental income—from necessities to lifestyle and travel, creating a lasting tailwind for the tourism economy.

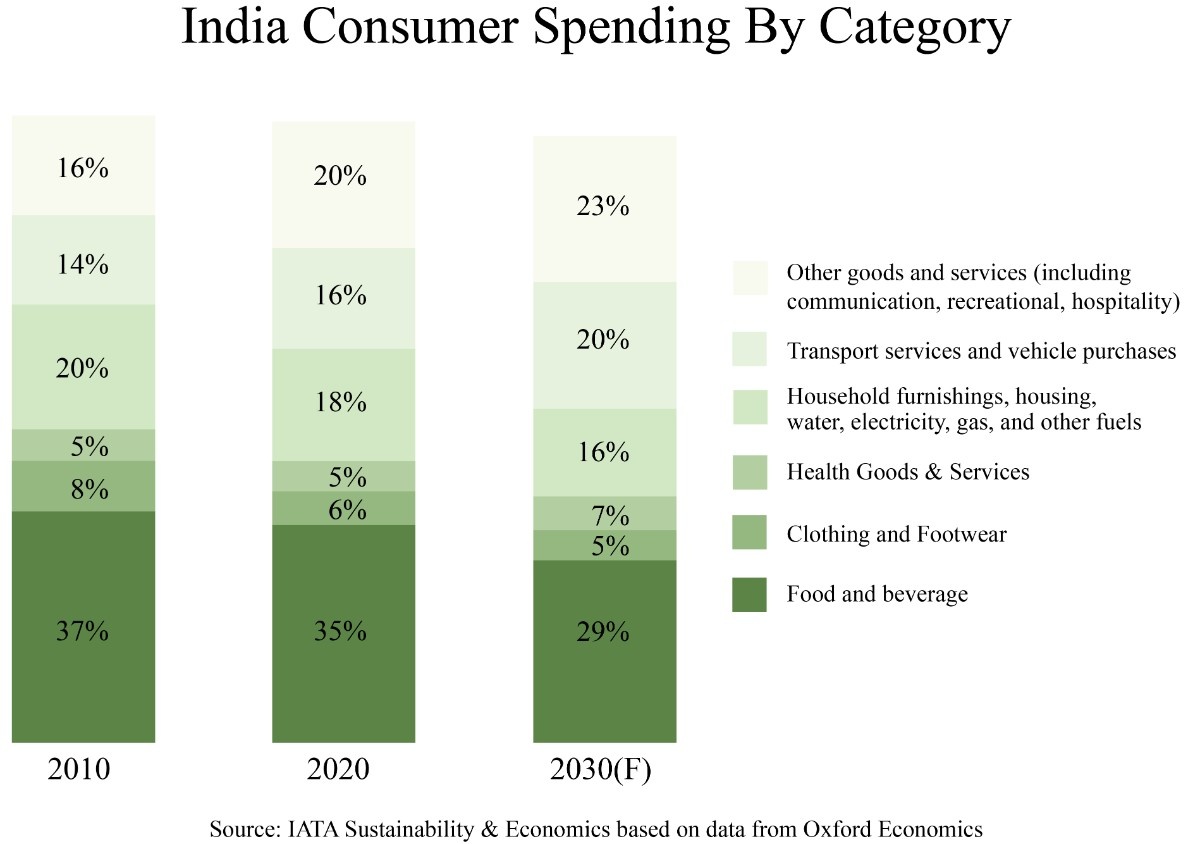

The shift is also visible in consumer spending patterns. According to Oxford Economics and IATA Sustainability & Economics data, India will witness increased expenditure in communication, recreational activities, and hospitality. This shows a structural reallocation of budgets from necessities to experiences.

These tax cuts are more than temporary relief—they are demand accelerators. Every additional rupee in the consumer’s hand nudges spending toward travel, leisure, and lifestyle experiences, powering continued growth for the industry.

Apart from tax reforms, the government is also actively boosting tourism through schemes—most notably the UDAN initiative, which has made flying affordable and accessible by linking smaller towns to metros. Complementary programs like the 2,541 crore Budget allocation, Swadesh Darshan 2.0, and PRASHAD further underline tourism as a priority.

- From 74 operational airports to 220: India’s Travel Revolution

India’s operational airports have grown from 74 in 2014 to 160+ in FY25, and the government aims to add another 50 airports in the next five years, unlocking new demand centers. The focus is not just on building new facilities but also on modernizing existing airports—improving capacity, passenger experience, and efficiency.

This ensures the system can handle India’s surge in air travel demand. Each new airport opens up fresh markets for hotels, restaurants, and transport services, especially in Tier-2 and Tier-3 cities.

2) Increasing Domestic Air Travel

India now ranks as the 3rd largest air transport market in the world, with an increase in the number of routes and flights – 37.5% of them are newly added routes that had not been operated in the past five years.

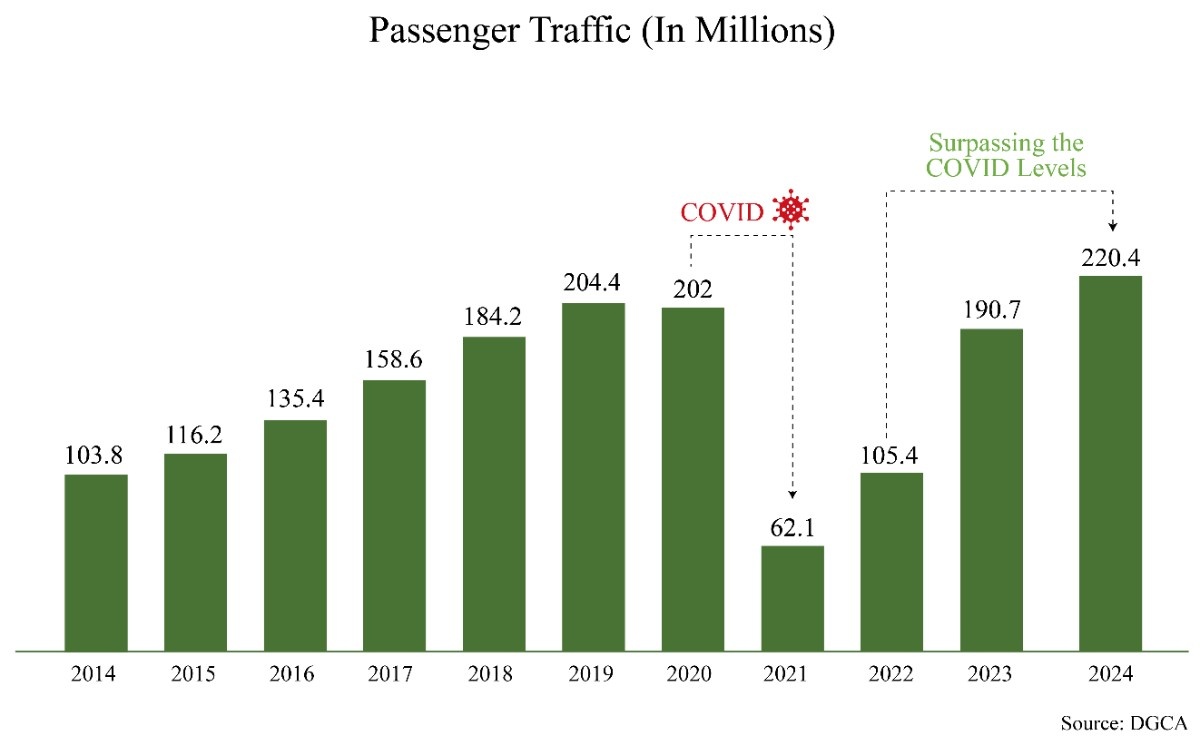

One of the strongest indicators of sustained travel momentum in India is the steady rise in domestic air passenger traffic. After peaking at 204 million passengers in 2019, the aviation sector experienced a sharp decline during the pandemic, reaching a low of just 62 million in 2021. However, the recovery has been swift and decisive. Passenger numbers rebounded to 190 million in 2023 and reached an all-time high of 220 million in 2024, surpassing pre-COVID levels.

Low-cost carriers are at the center of this transformation, converting first-time flyers into frequent travelers by making flying affordable and accessible. With capacity scaling up and regional penetration widening, air travel is steadily becoming the default choice for business, leisure, and even short-haul trips—turning India into one of the world’s fastest-growing aviation markets.

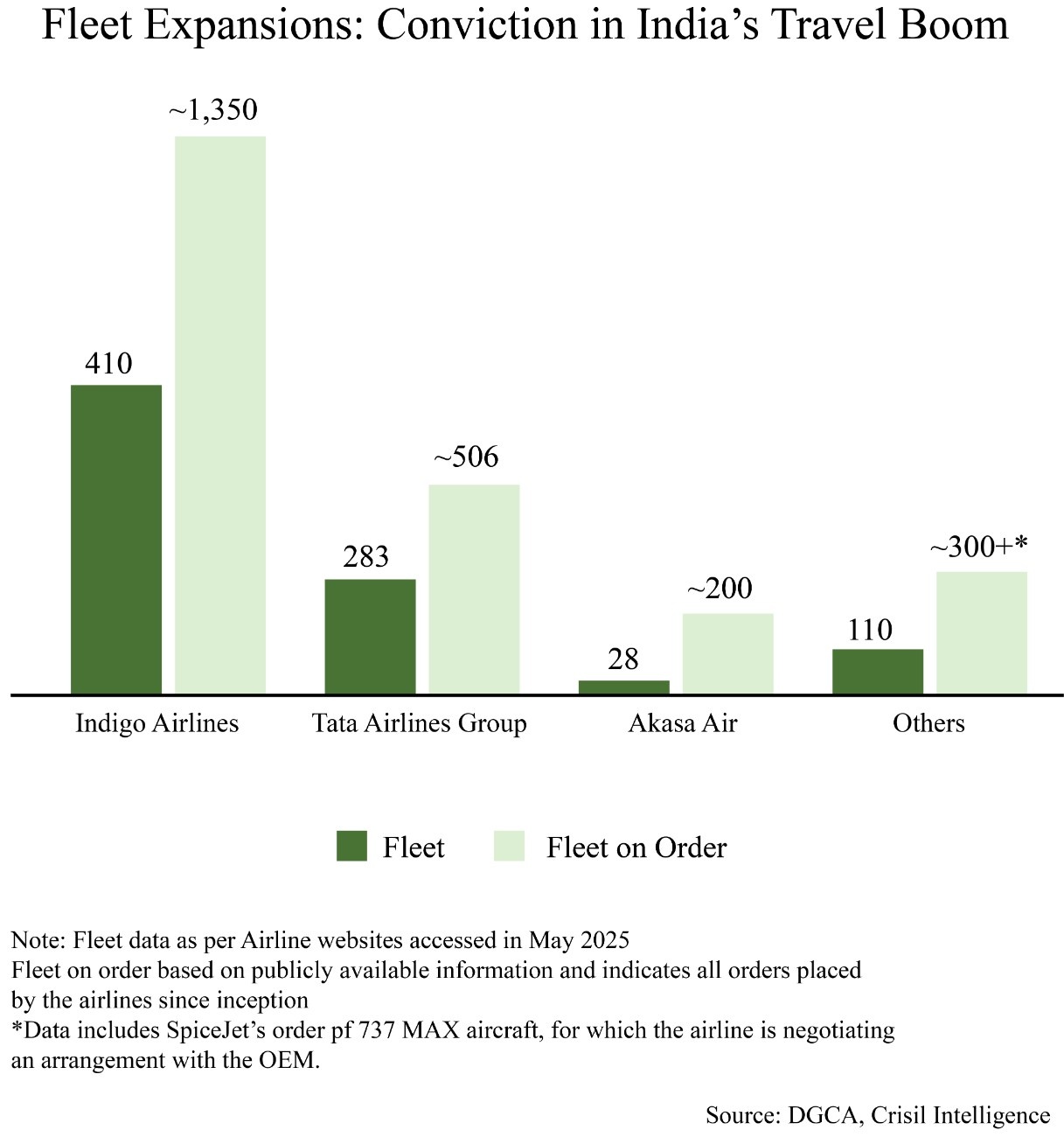

The aircraft orders placed by Indian carriers also reflects conviction that air travel demand will keep compounding over the next decade.

3) Pilgrimage Tourism is surging

Spiritual journeys have always held deep cultural and emotional significance in India. What is changing today is the scale, pace, and structure of how people undertake them.

– The 2025 Maha Kumbh Mela in Prayagraj drew over 66 crore devotees by February alone, making it one of the largest religious gatherings in history.

– In Ayodhya, more than 11 crore visitors arrived in just the first half of 2024, following the inauguration of the Ram Mandir and rapid infrastructure development.

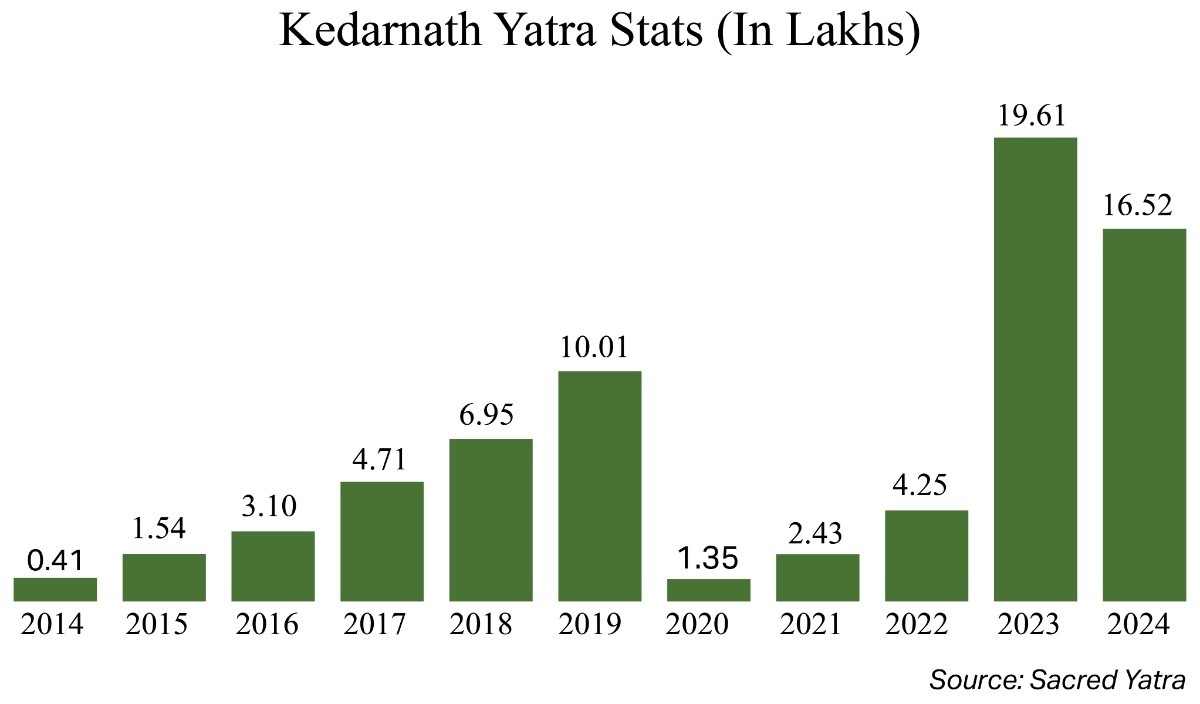

– The Char Dham Yatra continues to see record participation, with over 30.8 lakh pilgrims visiting Kedarnath and Badrinath in 2024.

– Consider Kedarnath alone—its footfall rose from just 41,000 in 2014 to over 19 lakh in 2023.

These numbers reflect not a new interest in pilgrimage, but a growing ecosystem around it—marked by digital registrations, planned itineraries, and better access. Spiritual travel is now more structured, more accessible, and more visible than ever before.

4) India’s MICE (Business Travel) is Booming

Business travel in India is picking up. Cities like Hyderabad, Delhi, and Mumbai are constantly hosting conferences, trade fairs, and leadership meets. It’s not just big corporates anymore—even startups, industry groups, and colleges are joining in. This steady flow of events is pushing demand for hotels that offer large banquet spaces and are close to convention centres. As a result, many hotel brands are adjusting their offerings to better serve this growing MICE (Meetings, Incentives, Conferences, and Exhibitions) segment.

5) Weddings are no longer just seasonal

Weddings have become a year-round business for hotels in India. With lavish functions now spread across multiple days and destinations, hotel bookings are being made months in advance—not just in peak wedding seasons, but even during off-peak months. Cities like Udaipur, Jaipur, Goa, and even hill stations have turned into go-to wedding spots. From pre-wedding shoots to mehendi and cocktail nights, hotels are offering full-service packages, creating a steady revenue stream. This shift is pushing more hotel brands to invest in larger banquet spaces, outdoor venues, and specialised wedding teams to capture a bigger slice of this booming opportunity.

The Rise of Branded Consumption: Unorganized to Organized Shift

In this entire travel and tourism boom, one of the most positive and structural changes is the shift from unbranded to branded offerings.

Hotels are steadily moving into the organized space, yet branded rooms still make up only ~35%, leaving significant headroom for growth.

Despite this expansion, India’s branded hotel room penetration remains among the lowest in the world. With just 0.3 branded rooms per 1,000 people, India significantly lags behind the global average of ~2.2 rooms per 1,000 people. This gap highlights the enormous runway for branded supply growth, especially as rising incomes and tourism demand continue to outpace room additions.

What makes this growth story compelling is the composition of new supply. A large part of the pipeline isn’t just greenfield development but also brownfield conversions, where existing unbranded, standalone hotels are brought under established chains like Taj, Vivanta, Ginger (IHCL) or Keys, Aurika, Red Fox (Lemon Tree). This structural shift ensures that as the market penetrates further, the organized share will keep climbing, making branded hospitality the dominant face of Indian travel and tourism in the coming decade.

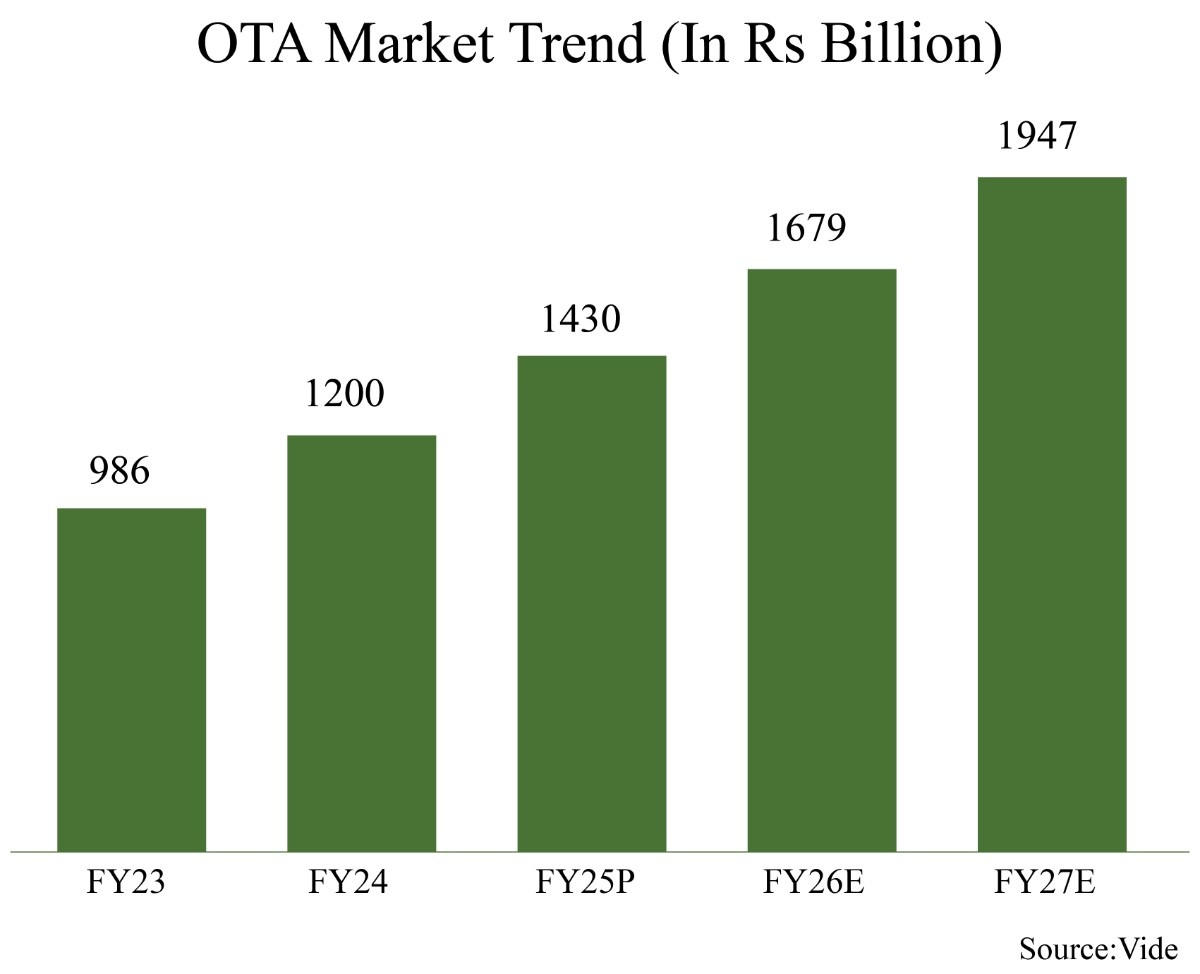

Online Travel Agencies (OTAs) have been at the forefront of the shift from unorganised to organised travel in India, replacing fragmented offline agents with consistency, convenience, and trust. Mobile-first platforms offering instant booking, dynamic pricing, and flexible cancellations have transformed how Indians plan their journeys, making travel more accessible and frequent. This has not only improved the overall user experience but also expanded penetration into Tier-2 and Tier-3 cities. Backed by this convenience, OTAs now account for nearly 68% of India’s online ticketing market, with the segment projected to nearly double from ₹986 crore in FY23 to ₹1,947 crore by FY27E.

Much like the hotel industry’s move from unbranded to branded supply, OTAs are driving the formalisation of travel consumption, ensuring reliability, transparency, and sustained growth for the sector.

The luggage industry is also experiencing a decisive shift from unorganised to organised players. In 2019, 39% of the market was organised, but by 2024 the share of organised players has already risen to 54%, and is projected to climb further to 62% by 2028. This reflects how rising incomes, greater brand awareness, and increased travel frequency are steadily formalising this segment with Tier-II and Tier-III cities emerging as new growth hubs, supported by e-commerce penetration and expanding brand reach.

Whether it’s booking a flight on an OTA, checking into a branded hotel, or carrying a trusted luggage brand, today’s Indian traveler is steadily shifting toward organized and reliable choices. This change is not only fueled by rising incomes and better infrastructure but also by reforms like GST, which have pushed more demand toward compliant, branded players. Travel is no longer just a one-off indulgence—it’s becoming a lifestyle habit, with stronger trust, higher repeat demand, and a clear runway for sustained growth.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR