India’s CDMO Rise: From Pill Factory to Strategic Partner

Every few decades, a shift in operating models reshapes an entire industry. In global pharmaceuticals, that shift is happening now, and India’s CDMO sector sits squarely at its centre.

The numbers show momentum. The global demand signals urgency. And the strategy points to integration. Development and manufacturing are no longer siloed functions. They are converging into unified service platforms, led increasingly by agile partners across India.

What was once a cost-driven market is now expanding into a value-led ecosystem. Infrastructure has matured. Compliance frameworks have scaled. Talent pipelines are growing in both depth and specialisation.

For investors, the signals are not speculative. They are visible across RFP volumes, contract sizes, and expansion plans. The story is not about disruption. It is about quiet consolidation of capabilities and a region aligning its strength with the future of drug development. If you need some figures for context, the domestic pharmaceutical industry is already worth close to $50 billion and projected to more than double in the next decade. That kind of growth may increase India’s GDP share by nearly 100 basis points. How about that!

Why CDMOs Are Reshaping Pharma’s Backbone?

At the heart of this story is a new development. India is becoming a trusted name in Contract Development and Manufacturing. CDMO is not a new concept. But the pace of adoption, the global demand, and the scale of investment now being seen are new. But let’s not get ahead of ourselves. Let’s start at the beginning.

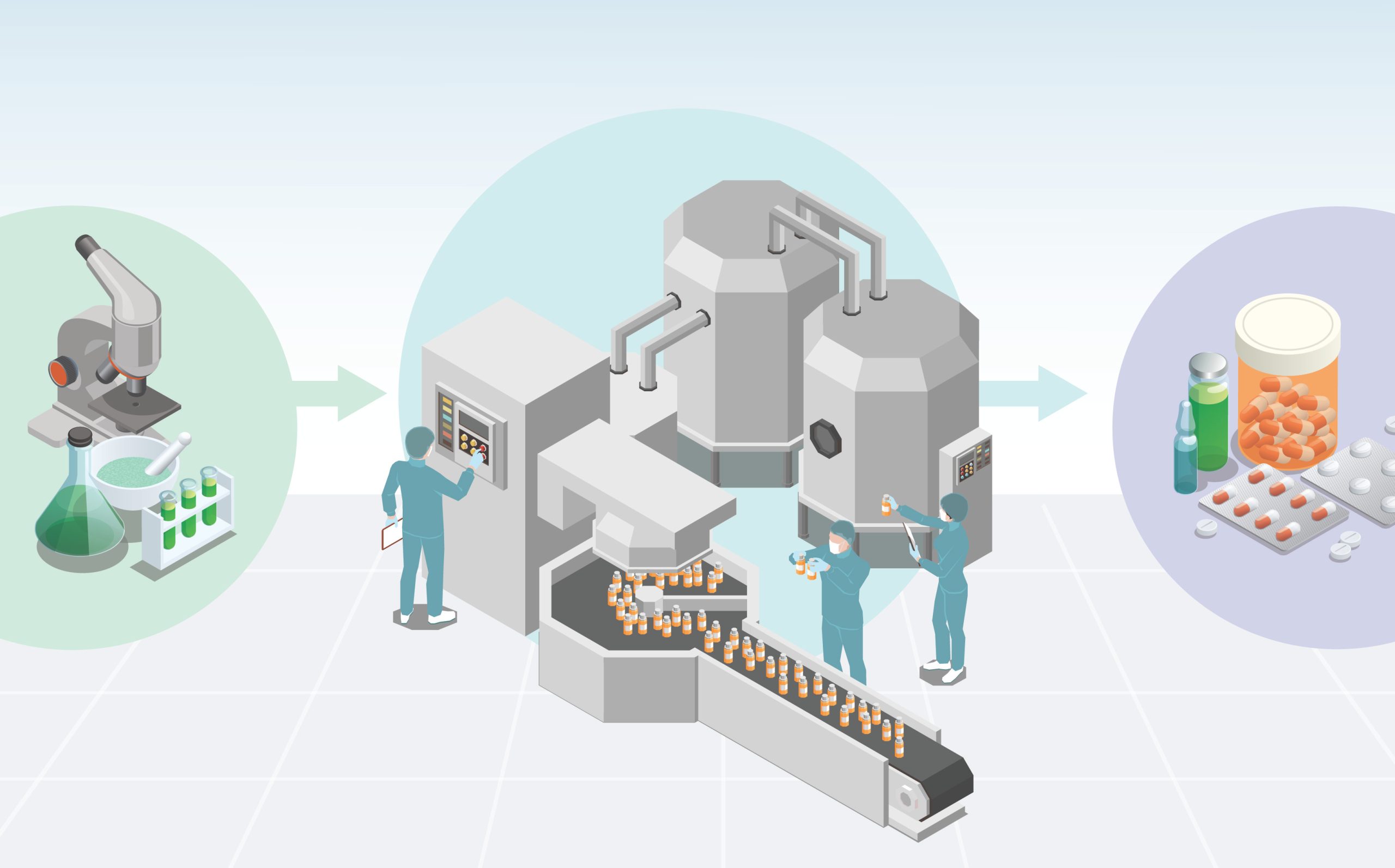

What Does a CDMO Really Do?

Think of a CDMO as the behind-the-scenes engine that helps pharmaceutical innovations move from lab to life. A Contract Development and Manufacturing Organisation doesn’t just assist with manufacturing. It connects every stage of the value chain, starting from early molecule development and continuing through to market-ready production.

Unlike traditional outsourcing partners, CDMOs are built for integration. They combine scientific depth with regulatory rigour, ensuring that ideas can scale without losing speed or compliance.

From Silos to Synergy: How Pharma Outsourcing Models Are Evolving

Imagine trying to assemble a complex machine with three different teams, each speaking a different language and working in different time zones. That’s how pharmaceutical outsourcing once looked: fragmented, delayed, and full of friction.

Today, that picture is changing. The industry is steadily moving toward integrated models where development and manufacturing flow together, not apart. But where does India come in?

The Market Outlook: Bigger, Faster, Stronger

India’s CDMO sector is expanding at a pace few anticipated. From a market size of $22.5 billion in 2024, it’s projected to touch $44.6 billion by 2029. That’s a compound annual growth rate of nearly 15 per cent, significantly ahead of the global pharma average.

According to Boston Consulting Group, India is on track to capture up to 5 per cent of the global CDMO market by 2030. It may sound modest, but for a sector that’s rapidly moving into higher-value territory, it’s a leap that matters.

What’s Powering India’s CDMO Momentum?

India's CDMO sector is not just growing—it's building significant momentum from multiple directions. With regulatory reforms, shifting global pharma dynamics, and emerging trends, the timing has never been better. Here’s what’s driving this exciting rise:

1. The Outsourcing Boom

Pharmaceutical companies worldwide are turning to outsourcing more than ever before. Faced with rising costs and tightening regulatory demands, doing everything in-house is no longer practical. In 2024 alone, Indian CDMOs saw a 50% spike in project requests—an unmistakable sign that the global market is putting its trust in India.

2. The Patent Cliff Is Opening New Doors

As blockbuster drug patents expire, the race to produce generics and biosimilars is on. India, already a master of the generic game, is uniquely positioned to lead the charge. With established regulatory processes and cost-efficient manufacturing, Indian CDMOs are ready to meet the surge in demand for off-patent drugs.

3. Biologics and Specialty Drugs Are the New Frontier

Pharma is shifting towards biologics, specialty injectables, and advanced therapies—products that require precision, sophistication, and specialized environments. Indian CDMOs are stepping up by investing in cutting-edge technologies like bioreactor systems, cleanrooms, and expert teams to meet this growing demand and move further up the value chain.

4. Regulatory Confidence Is Soaring

India's regulatory ecosystem has evolved impressively, and most top-tier CDMOs are now fully compliant with global GMP standards. This newfound regulatory confidence is enabling Indian CDMOs to gain credibility and make their mark in highly regulated markets like the US and Europe, giving them a competitive edge.

5. India’s Cost Advantage Is Still a Game-Changer

Even in a world facing inflationary pressures, India’s CDMOs continue to offer a significant cost advantage—about 15-20% lower than other outsourcing destinations. This cost efficiency is a huge draw for pharma companies working under tight margins, making India a go-to hub for pharmaceutical outsourcing.

6. Talent Depth with Room to Grow

India’s talent pool in chemistry and process engineering is one of its strongest assets, enabling CDMOs to tackle complex formulations and scale-up operations. However, when it comes to biologics, there’s still work to be done. India’s talent pool needs to grow by six to seven times to meet the booming global demand for biologic products. But with the right investments in education and infrastructure, this growth is well within reach.

Investing in India’s CDMO Shift: A Decade of Opportunity and Discipline

A quiet shift is underway in India's pharmaceutical backbone. What was once a story of low-cost manufacturing is now steadily becoming one of innovation, integration, and strategic value creation. This evolution doesn’t just change how drugs are made; it changes who benefits from making them.

As global pharma looks for partners that offer both scale and specialisation, India’s CDMO sector is stepping into a more central role. What makes the timing especially relevant is the convergence of three powerful currents: global demand for complex therapeutics, strong domestic policy support, and a maturing regulatory framework that meets international expectations.

For investors, this is not just another manufacturing trend. It’s a deeper, more structural movement toward integrated pharmaceutical services, one that aligns closely with intellectual property and long-term value creation.

India is witnessing a shift towards more integrated pharmaceutical service models, where CDMOs provide a range of services across the entire drug development lifecycle, from research and development to manufacturing. This shift is supported by policy initiatives such as the Production Linked Incentive (PLI) schemes, which aim to boost domestic manufacturing and innovation. Additionally, there is a global trend towards increased outsourcing of research, development, and manufacturing, which aligns with India’s growing role in this sector.

India’s regulatory track record has also improved, with many CDMOs meeting global GMP standards, enhancing the country’s credibility in international markets. Moreover, the cost structures across various service verticals in India remain competitive, making it a viable option for global pharmaceutical outsourcing. These factors contribute to India’s growing significance in the CDMO space, offering potential for continued development within the sector.

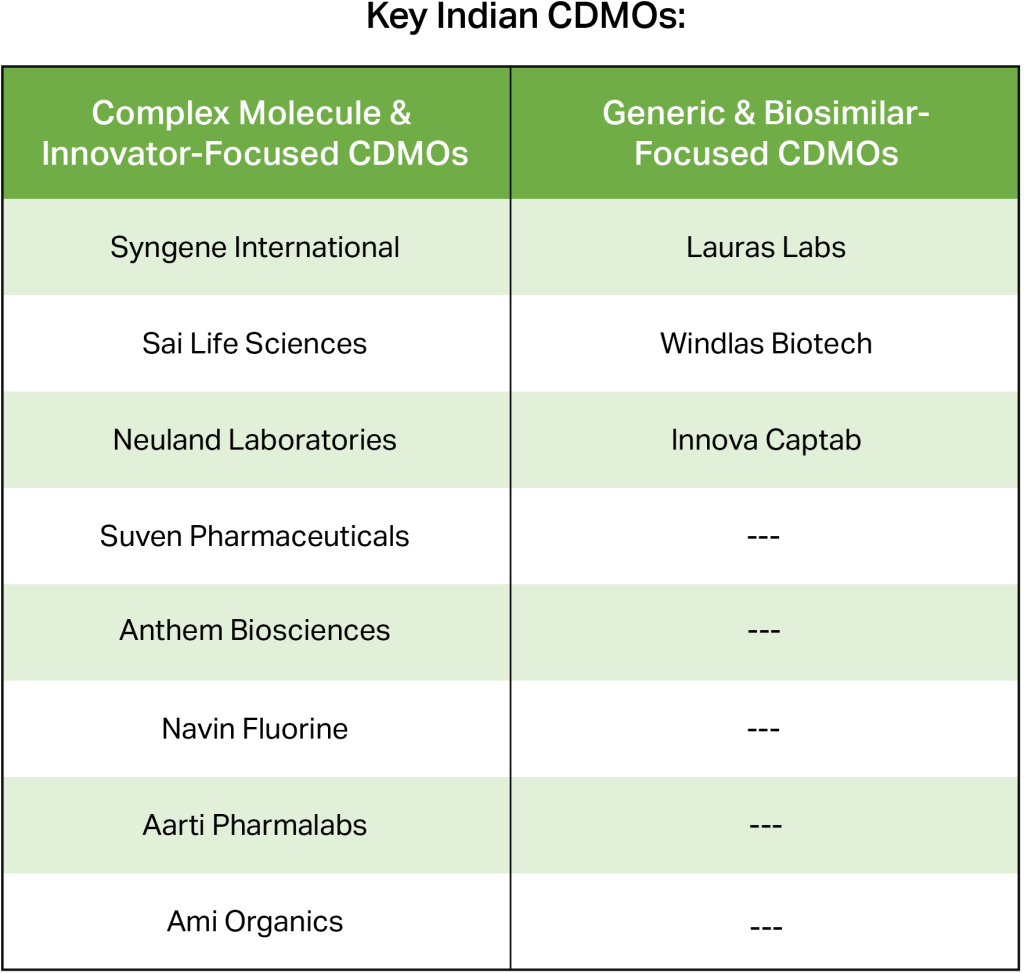

Mapping the CDMO Landscape: Where Each Player Fits In

The CDMO space isn’t monolithic. It spans a wide spectrum, with players positioned according to the kind of drugs they support, how complex those drugs are, and the regulatory or production demands involved. Two broad categories emerge:

1) Complex Molecule & Innovator Drug CDMOs: These players support novel drugs (NCEs, biologics) from early development to commercial scale. They offer advanced capabilities like custom synthesis, biologics production, clinical trial supplies, and regulatory filings—acting as strategic partners throughout the drug lifecycle. Their integrated services reduce inefficiencies and accelerate time-to-market.

2) Generic & Biosimilar CDMOs: Focused on cost-efficient, high-volume production of off-patent drugs and biosimilars. Their strengths lie in streamlined manufacturing, multi-region regulatory compliance, and quick market entry, enabling global scale at optimized costs.

Risks That Need To Be Considered

India’s rise in the CDMO space is real, but the road forward is complex. One of the sector’s most pressing challenges is talent. While India has strong chemistry and engineering depth, biologics demand a new level of specialisation, and scaling that expertise will take time.

Global clients are also expecting more. Compliance requirements are growing sharper across jurisdictions, and companies that can’t match this pace may struggle to compete. At the same time, other emerging pharma hubs are moving fast, supported by aggressive local policies and focused capital deployment. And because this sector is tightly linked to global R&D and regulatory cycles, any disruption in global innovation flows can echo back into India’s CDMO ecosystem.

What Investors Should Watch Next

India’s CDMO sector is entering a new phase. The growth is no longer about volume alone. It is about capability, quality, and co-ownership.

Innovation is not limited to molecules. It is seen in how contracts are structured. Some CDMOs are exploring licensing models. Others are investing in digital twins for process optimisation.

Investors should look for CDMOs with strong compliance records, high client retention, and clear expansion plans. The most promising companies will be the ones that combine scientific depth with operational agility.

NIVESHAAY INVESTMENT ADVISORS

508, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7859870559

research.smallcase@niveshaay.com (Equity Baskets)

NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED

610, SNS Platina, Near Someshwara Enclave, Vesu, Surat, Gujarat-395007

(+91) 7836915478

contactaif@niveshaay.com (AIF)

SEBI Registration No. : INH000017338, IN/AIF3/24-25/1571, IN/AIF2/24-25/1607, INP000009506 | BASL Membership ID: 6276

Disclaimer:

Investment in Securities Market are subject to market risks. Read all related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory

NIVESHAAY INVESTMENT ADVISORS © . All Rights Reserved., NIVESHAAY INVESTMENT MANAGEMENT PRIVATE LIMITED © . All Rights Reserved.Smart ODR